This note was originally published at 8am on January 28, 2014 for Hedgeye subscribers.

“Wall St. was a street of vanished hopes, or curiously silent apprehension, and a sort of paralyzed hypnosis.”

-New York Times

Imagine that was the header for @NYT on the eve of America’s central economic planner in chief’s State of The Union. Newsflash: it’s not. That was the front page of the New York Times on the day after the 1929 US stock market crash.

John Coates cites the aforementioned headline in chapter 1 (The Biology of a Market Bubble) of The Hour Between Dog and Wolf and goes on to remind us that “research on body-brain feedback, even within physiology and neuroscience, is relatively new.” (pg 28).

So how are you feeling this morning? While you know that hope is not a risk management process, apprehension and paralysis are all part of the game. While it’s hard to sell`em on green and buy`em on red, fading your emotional state is often the precise action to take.

Back to the Global Macro Grind…

I don’t know about you, but in the heat of the decision making moment I fade how I feel about markets a lot. Through 15 years of trial and error, I’ve learned to increasingly rely on multi-factor, multi-duration, risk management signals amidst the research noise.

Since I don’t have a dog (or wolf) in the fight in marketing a perma bullish or bearish position, I use the TRADE versus the TREND in order to tone down my testosterone. Yep, I’m a dude – keeping that under control matters!

To review our process lingo:

- TRADE is 3 weeks or less in duration

- TREND is 3 months or more in duration

The reason why I use “more” or “less” is because time in my model (days) varies inversely with volatility. In other words, if front-month volatility ramps +50% in a week, the number of days in my TRADE model falls, fast – and, if implied volatility (looking out on the curve) doesn’t confirm that immediate-term information surprise, I keep an above average amount of duration (time) in the TREND model.

That may or may not make sense to you. So to put it more simply:

- When both front-month and implied volatility are signaling lower-highs and lower-lows, a monkey can buy stocks

- When both front-month and implied volatility move from bearish to bullish TRADE and TREND, monkeys get killed

Momentum monkeys, I mean.

I know, I know. Every time I call someone a monkey, I trigger an emotional response. But, please, don’t be offended. I am a monkey too – I’m just one that tends to learn from the cage door being slammed on my fingers.

Volatility, of course, is the #1 risk factor that every major fund manager who has fallen from grace has messed up. Even the world’s best messed this up in bonds last June. Many more have already messed this up in Japanese and Emerging Market Equities YTD.

This is basically why I completely disagree with the concept of being an active “long-term investor” who doesn’t use an implied volatility risk management overlay. While it would be nice to wake up to sun and bananas at the zoo every day, reality is that every once in a while a storm rips the cages open and the tigers, who have been putting up with monkey-bull chirping for a year, are hungry.

Back to the actual levels, to keep this simple, let’s just focus on the inverse relationship between the SP500 and VIX:

- TRADE – SPX 1837 momentum support broke as 13.81 VIX resistance became immediate-term support

- TREND – SPX 1779 support was tested intraday yesterday (and held), but VIX 14.91 TREND is firmly intact

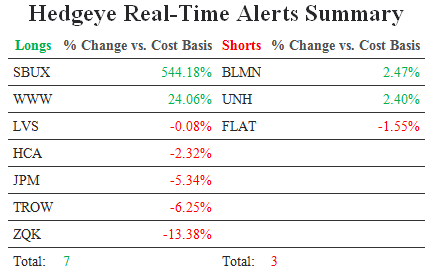

And here Mucker the monkey was covering oversold shorts (and buying one long, LVS) into the close as 1779 SPX held (which would be called a high-probability gamble - dealer shows a 6 in #BlackJack)… and the minute I saw Apple (AAPL) guide down, I thought it was going to be a gamble I’d pay for today (and deserve it).

But, the US Equity Futures are up 8-10 handles and I’ll play lucky on the open today instead. I won’t, however, confuse that with the next leg up in this market ripping to fresh all-time highs. Provided that 1837 SPX TRADE resistance and 14.91 VIX TREND support remain intact, I’ll be a seller again this morning on green (like we were in #RealTimeAlerts on the open yesterday).

I know that playing the game across durations isn’t for everyone. But this is what I do. And I like it. I can assure you that the longest of “long-term” investments you can ever make is starting your own company with all of your own money. And for me at least, that investment requires absorbing 24/7 risk management, apprehension, and pain – if you want the long-term to last longer, that is.

Our immediate-term Global Macro Risk Ranges are now (12 Big Macro Ranges are in our Daily Trading Range product):

SPX 1758-1822

VIX 14.91-20.41

USD 80.18-80.79

Pound 1.64-1.66 (bullish)

NatGas 4.58-5.15

Gold 1240-1272

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer