Last week was another difficult week for consumer stocks, with the XLP down -1.74% versus the SPX down -0.43%. The Hedgeye U.S. Consumption Model is flashing predominantly red, as only 3 of the 12 metrics are flashing green. Please see the table below for more detail. Although personal spending turned green last week, it comes with a caveat – it is being driven primarily by re-leveraging, as the personal savings rate fell to the lowest level since 2008 (3.9%).

The Macro team’s 1Q14 theme of #InflationAccelerating continued to play out last week and manifested itself in the form of slower growth. There were plenty of red flags for growth in December and things appear to have slowed further in January.

As Keith highlighted in today’s Early Look:

- CRB Commodities Index (19 Commodities) = +0.3% last wk to +1.1% YTD (vs SP500 -3.6%)

- CRB Commodities Foodstuff Index = +1.1% last wk to +3.3% YTD

- Corn +1.0% last week to +2.8% YTD

- Cocoa +4.3% last week to +7.5% YTD

- Coffee +9.4% last week to +13.1% YTD

- Cheese +2.2% last week to +18.0% YTD

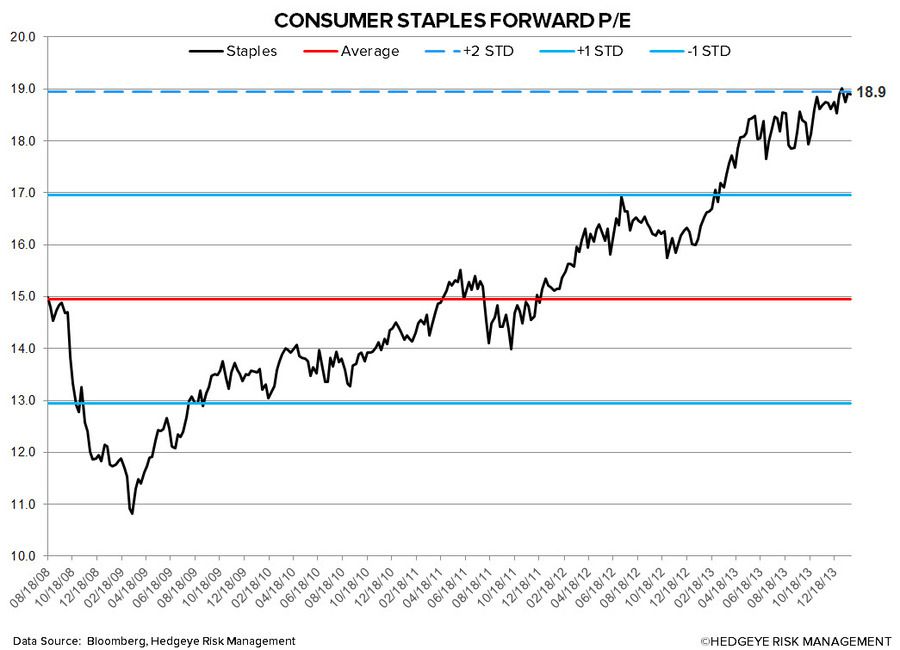

In the charts below we look at the largest companies by market cap in the Consumer Staples space from both a quantitative perspective and fundamental aspect where we can offer one. As you will see over time, sometimes our fundamental view does not align with the quantitative setup (though not often).

Top 5 Week-over-Week Divergent Performances:

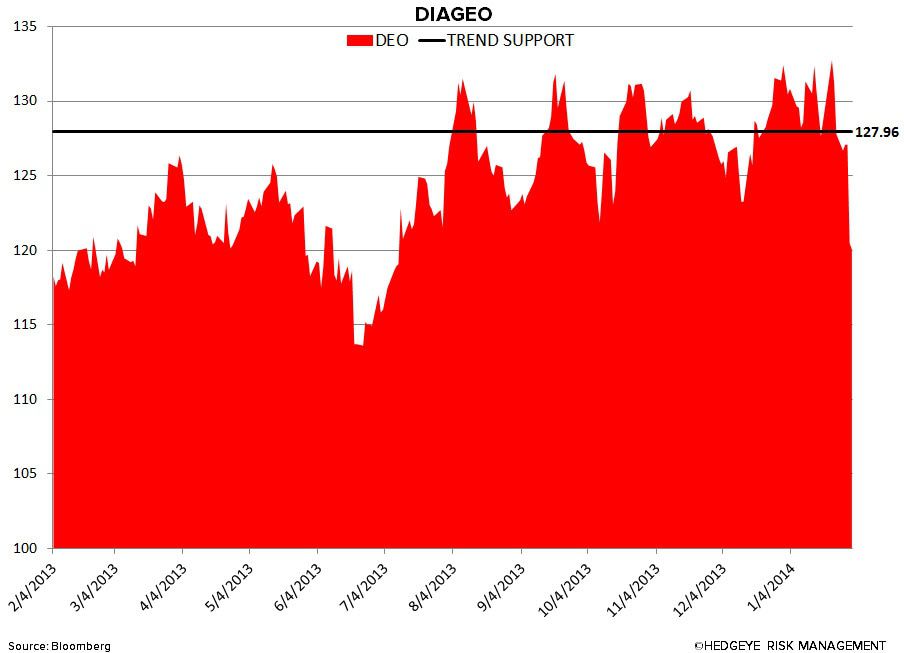

Negative Divergence: ENR -7.4%; DEO -6.1%; MKC -7.0%; MO -5.6%; DF -4.3%

Positive Divergence: NUS +10.7%; TSN +7.6%; HLF +7.2%; HSH +5.2%; IFF +2.0%

The “Newsy” News Flow:

Herbalife (HLF) announced this morning that it will boost its share buyback by 50% to $1.5 billion and offer $1 billion in convertible senior notes.

- We still like the stock on the long side from a trading perspective – the company clearly has the cash to protect the stock, key activist investors remain poised on the other side of Ackman’s short bet, no government agency appears ready to open Pandora’s box on the multi-level-marketing industry, and any claims that Ackman may have against HLF’s China business as a pyramid scheme (expected to be presented this month) may be at best immaterial: 1) they will be hard to investigate given the lack of transparency in China, and 2) HLF can afford to cut its exposure to China, which is only ~11% of sales.

Altria (MO) announced this morning it’s in agreement to acquire the e-vapor business of Green Smoke for $110M in cash.

- This is a key signal that Big Tobacco is looking to play catch-up for e-cig market share. LO was first out of the box with its acquisition of Blu in April 2012, then bought UK-based e-cig manufacturer SKYCIG in October 2013 to expand internationally. Both MO and RAI were late to the e-cig “party”, rolling out their own e-cig brands (MarkTen and Vuse, respectively) only in late 2013 in test markets, with plans for national distribution by mid-year. A wild card on the future direction of the industry remains the FDA. We’d expect it continues to drag its feet, balancing the need to protect the consumer while promoting harm reduction of traditional tobacco. We’re bullish on e-cigs and see moves to consolidate as conviction from Big Tobacco that the category is here to stay.

POST announced this morning it has agreed to buy the PowerBar and Musashi sports brands from Nestle for $550 million.

- We’re bullish on CEO William Stiritz’s push to transform the portfolio to meet consumer trends of health (fitness) and wellness. This adds to such brands as Premier Nutrition supplements and Hearthside Food Solutions’ organic cereals and snacks that were acquired since Post was spun off from Ralcorp in 2012. Note: Stiritz also holds a 7.4% stake in HLF, and has said he’s willing to take part in a leveraged buyout of the company.

Earnings Calls This Week (in EST):

Tuesday (2/4): ADM 9am; CHD 10am; HAIN 4pm

Wednesday (2/5): EL 9:30am; CCE 10am

Thursday (2/6): K 9.30am; PM 1pm

Howard Penney

Household Products

Matt Hedrick

Food, Beverage, Tobacco, and Alcohol

(o)

ALCOHOL

BUD – doesn’t look much healthier than DEO or MO now either; has moved from bullish to bearish TREND in the last month; TREND resistance = 101.28

DEO – looks just like MO – no more TREND mo mo as TREND reverses from bullish to bearish w/ $127.96 TREND resistance

BEVERAGE

KO – you’d think the consumer and emerging market world was ending looking at some of these charts; big time bearish breakdown confirmed here this week; TREND resistance = 40.19

PEP – doesn’t look as horrendous as KO, so it just looks horrible instead; bearish TREND confirmed this wk = 83.18 resistance

FOOD

GIS – nothing new here; stock still looks awful; Bearish Formation @Hedgeye w/ TREND resistance = 50.07

MDLZ – no Peltz takeout premium = no more bullish TREND; what was support is now TREND resistance up at 33.67

HOUSEHOLD PRODUCTS

KMB – the only name on this list that signaled bullish for real last week had some real alpha this wk; love that – bullish TREND confirmed with immediate-term TRADE support above that at 106.08

PG – another Bearish Formation with TREND resistance confirmed this wk up at 80.36

TOBACCO

MO – just lost whatever was left of its mo mo; TREND reversal from bullish to bearish this wk (TREND resistance = 36.92)

PM – dog breath stock continues to implode as our Bearish Formation signal remains firmly intact; TREND resistance = 85.46; classic series of lower-highs and lower-lows