With U.S. #GrowthSlowing sequentially, sentiment is reversing some. Some.

But is consensus bearish enough right now? Nope.

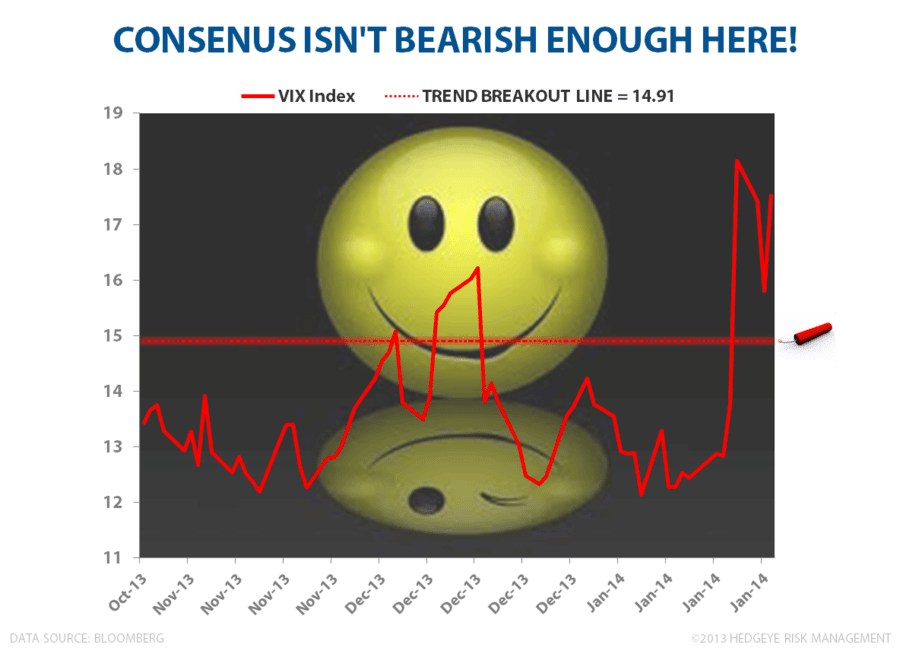

This morning’s II Bull/Bear Survey is still +3780 basis points wide to the Bull Side (53.1% Bulls, 15.3% Bears). Meanwhile, the VIX has broken out over 14.91.

Bottom line: People aren't bearish enough, particularly if growth continues to slow.

Editor's Note: This is an excerpt from Hedgeye CEO Keith McCullough's pre-market morning research. For more information on how Hedgeye can help you prosper and learn click here.