Below are Hedgeye analysts' latest updates on our high-conviction stock ideas as well as CEO Keith McCullough's refreshed levels for each stock. In addition, this week we have selected three institutional research notes we believe offer a valuable look into the state of the markets.

Trade :: Trend :: Tail Process - These are three durations over which we analyze investment ideas and themes. Hedgeye has created a process as a way of characterizing our investment ideas and their risk profiles, to fit the investing strategies and preferences of our subscribers.

- "Trade" is a duration of 3 weeks or less

- "Trend" is a duration of 3 months or more

- "Tail" is a duration of 3 years or less

IDEAS UPDATES

The latest comments from our Sector Heads on their high-conviction stock ideas.

CCL – We recently completed our early Wave cruise pricing survey. The survey was bullish for Carnival on the margin with outperformance of the Carnival brand in the Caribbean. Europe pricing was mixed while Alaska was the glaring trouble spot. Overall, we believe Wave is trending above CCL’s management expectations. With easy Triumph comparisons coming in mid-February, early strength in pricing bodes well for Carnival.

DRI – Good news for Darden shareholders this week. The heat increased on management with activist investor Starboard Value LP urging DRI to delay the spinoff of Red Lobster to find an alternative option to increase shareholder value. Restaurant Analyst Howard Penney couldn’t agree more with the Starboard letter saying it appears that the activists are close to agreeing on what we believe the new Darden should look like.

DRI has the potential to become the true leader in the casual dining industry, but it needs an unbalanced (unbiased) force to make the changes necessary and unlock shareholder value. The Starboard letter represents one more step in the right direction.

FDX – Shares of FedEx were weak as the broader market experienced increasing pressure this week. There was little company specific news flow, other than some minor B to C customs issues in Russia and positive comments from DHL on European activity. Market participants are likely focused on the deluge of earnings over coming weeks.

FXB – We received more positive economic data out of the UK this week, in line with our Q4 2013 and Q1 2014 macro themes of #EuroBulls and #GrowthDivergences, respectively, that forecast a bullish outlook for the British Pound.

- The Unemployment Rate ticked down to 7.1% in NOV vs 7.4% in OCT and expectations of 7.3%.

- BOE Minutes released showed a 9-0 decision to keep the benchmark rate unchanged and the asset purchase target unchanged.

UK high frequency data continues to offer evidence of emergent strength in the economy, and in many cases the data is outperforming that of its western European peers, which we expect should provide further strength to the equity market and currency. The decline in the unemployment rate represents the largest decline in almost 5 years! Additionally we’re seeing CPI also moderated, down 10bps to 2.0% in DEC Y/Y in the last reading – we expect this cut to boost business and consumer confidence and increase purchasing power and consumption.

We remain bullish on the British Pound versus the US Dollar (etf FXB), a position supported over the intermediate term TREND by prudent management of interest rate policy from Mark Carney at the BOE (oriented towards hiking rather than cutting as conditions improve). This was confirmed once again by the Minutes released today, which continues to stoke the Pound. The Bank said there was no need to raise rates even if the unemployment rate hits 7% in the near future.

The British Pound is holding its Bullish Formation, which we expect will continue to be supported by prudent monetary policy from the BOE and strengthening economic fundamentals.

HCA – Healthcare Sector Head Tom Tobin has no update this week.

JPM – Financials Sector Head Josh Steiner added JPMorgan Chase & Co. to Investing Ideas this week. Click here for the full report issued Friday evening.

RH – Weather continues to be a point of contention for investors with the retail sector this quarter. We addressed this point briefly last week and maintain our stance that Restoration Hardware, unlike many other retailers, won’t feel the effects of the recent cold spells in the Midwest and Northeast as badly as some of the other names in the consumer discretionary space for the following reasons.

1) E-commerce – RH’s direct business accounts for 47% of company revenues. Consumers may use Brick and Mortar stores as a showroom before purchasing online, but weather induced traffic declines may displace sales by a day or two but will not eliminate them all together. Unlike traditional retailers – RH purchases are event driven, and there is very little correlation between traffic and sales unlike what you might see at Target or Bed Bath & Beyond.

2) 90% of all RH orders ship to consumers home – The current wait time for an RH order is 6 – 9 weeks. That means that essentially all meaningful (and by meaningful - we mean revenue driving categories like furniture) sales are booked for the quarter. Delivery may have been slowed due to adverse driving conditions – but those effects are marginal.

3) Real estate distribution – 61% of RH stores are in the South/West regions of the United States, while 39% are in the Midwest, Northeast, and Canada. RH’s limited store base and geographic distribution sets it apart from other retailers who rely more heavily on the hard hit areas of the Midwest and Northeast. On the Ethan Allen Q214 conference call the company noted that weather was a factor in a quarter, but that stores in the South and West were the highest comping stores in the fleet. We expect the same to hold true for RH.

In conclusion, it would be irresponsible to ignore the fact that weather could be a drag on this quarter’s results. But, we believe that those effects are grossly overestimated by the rest of the street.

TROW – We relay that our ongoing call of a retail investor allocation into equities and out of fixed income started as of mid-year 2013 and is continuing. As crystallised in the recent BlackRock fourth quarter earnings report, BLK's category asset flows showed the strongest growth in retail equities with weaker comparative trends in fixed income. We think that the retail story relayed by BlackRock is a trend that can continue into 2014 as mutual fund flow driven by retail investors is a performance chasing exercise with still better return prospects in equities over fixed income.

With this theme in mind, we continue to recommend T Rowe Price (TROW) on the long side with allocations of 82% of its assets-under-management in equities and 80% of the firm's AUM in retail.

WWW – Keds accounts for a negligible percentage of Wolverine Worldwide's annual revenue, but it is one of the company’s best known brands. Sales for Keds topped out at $450mm, but at the time of WWW’s acquisition of the PLG brands, annual sales totaled only $80mm. PLG focused its attention on its Payless business and the Sperry brand while Keds was largely ignored. Brand equity at Keds is strong, but the execution behind that powerful brand name left much to be desired. The same was true for Converse, who prior to its acquisition by Nike in 2003, was a $200m brand. In FY13 revenue totaled nearly $1,500mm.

After the acquisition, Wolverine looked to right the ship and rolled out 4 new initiatives in 2013: 1) an endorsement contract with Taylor Swift, 2) a design partnership with Kate Spade, 3) a partnership and distribution agreement with ANF’s Hollister, and 4) Keds branded retail space in high traffic malls. The Taylor Swift partnership is entering the 2nd year of a 3 year contract, and we learned at the ICR conference that Kate Spade and Keds would be teaming up once again this year. As a result of these efforts, Keds sales grew at a ‘solid double digit rate’ this year, and we continue to believe that Keds will generate in excess of $400mm in revenue in 4 years. Granted, much of that will growth will come through international expansion, but the early read throughs in the US are promising.

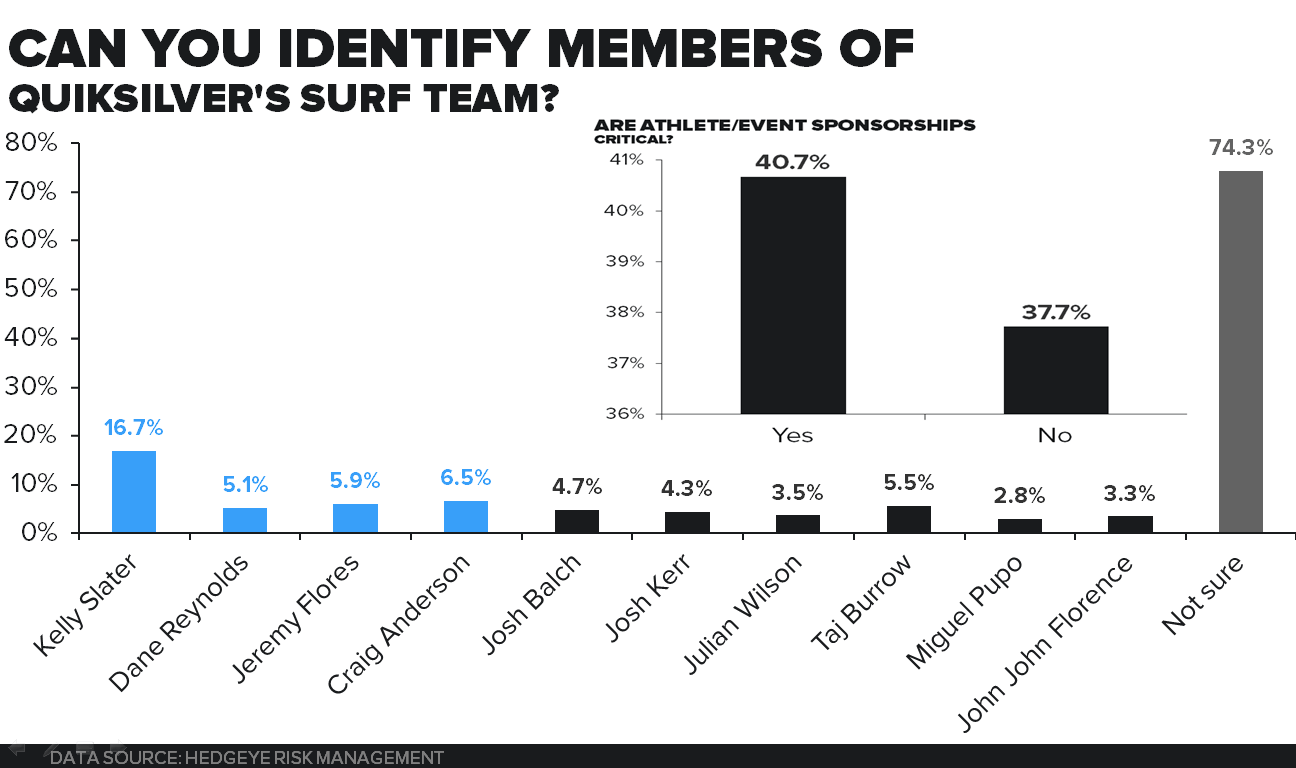

ZQK – When Quiksilver’s new CEO, Andy Mooney, was hired he laid out a detailed profit improvement plan that focused on cost reduction, brand consolidation, and revenue growth. One of the most polarizing cost reduction plans concerned the company’s marketing strategy – more specifically its history of shelling out generous amounts of cash to sponsor action sports athletes and events. Investors feared that this shift in strategy would tarnish the brands reputation as an authentic action sports brand and disconnect it from its roots.

We decided to ask consumers to get their opinion on ZQK’s brands so that we could gauge things like brand loyalty, authenticity, and purchase intent. Our results were jam packed with insight, and one of the most telling things we found was that athlete and event sponsorships really don’t matter despite what the consumer might say.

40.7% of the consumers we surveyed said that athlete and event sponsorships were critical to the Quiksilver brand image. We decided to dig a little deeper to judge if that was truly the case, and found that nearly 75% of the respondents were unsure of who Quik’s actually team members were (Quiksilver team members are displayed in blue). On top of that only 17% knew that Kelly Slater – the Michael Jordan of surfing – surfed for Quiksilver. The results speak for themselves on this one.

* * * * * * *

Click on the titles below to unlock the institutional research notes.

McDonalds's (MCD): Reiterating Short In 2014

Veteran Hedgeye Restaurants analyst Howard Penney still doesn't like what's going on at McDonald's. He has been bearish on MCD for quite some time now and continues to believe the company has issues in its underlying, core business. While we believe management has realized they have problems, we have little faith that they have found the proper solutions.

Argentina's options have not changed: default or burn the peso. Neither outcome is good for sentiment surrounding beleaguered Emerging Market assets. Analyst Darius Dale writes that "he feels bad writing so negatively about Argentina’s managerial woes. Typically when our firm publishes bearish research on companies, usually the worst thing that could happen is a bunch of overpaid corporate executives lose their jobs as a result of persistently poor operational performance. For countries, however, the ramifications of persistent mismanagement are considerably more far-reaching."

ICI Fund Flow Survey: Equity Flow Rebounds

Financials analyst Jonathan Casteleyn writes that Equity flows perked up strongly after a negative week to start 2014 with the biggest inflow in 10 weeks. This strong weekly inflow coupled with the slight outflow from last week has now moved the 2014 weekly average to a $3.9 billion average inflow for equities to start 2014, a follow through on 2013's positive trends where $3.0 billion per week on average flowed into stock funds.