DISMAL DECEMBER

This weekend Black Box gave us a look at December sales trends, which are, on the margin, negative for the industry. Same-restaurant sales and same-restaurant traffic trends were both negative during the month and down sequentially from November. Before we delve further into the details of the release, we thought it would be useful to highlight which casual dining chains had same-restaurant sales estimates adjusted since December 2nd.

Zero of the casual dining companies that we track had 4Q13 same-restaurant sales estimates revised up over the course of December.

The following companies had 4Q13 same-restaurant sales estimates remain flat over the course of December: BOBE, BWLD, CAKE, CBRL, CEC, DIN, IRG, KONA, RUTH, RRGB, TXRH

The following companies had 4Q13 same-restaurant sales estimate revised down over the course of December: BBRG, BJRI, BLMN, CHUY, DFRG, EAT

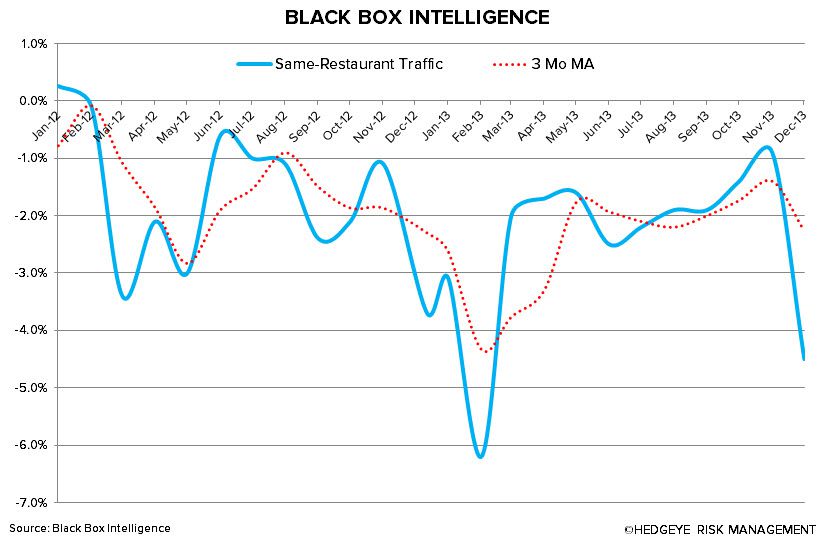

Moving back to the release, Black Box reported that December 2013 same-restaurant sales decreased -2.0%, a 280 bps sequential decline from November. Same-restaurant traffic trends were down -4.5%, a 360 bps decline sequential decline from November. These same-restaurant sales and traffic estimates come against results of -1.1% and -3.7%, respectively, in December 2012. 3-month same-restaurant sales and same-restaurant traffic declined 70 bps and 90 bps, respectively, on a sequential basis.

December was hurt by winter storms and a shortened shopping season due to a late Thanksgiving. Furthermore, Thanksgiving was included in December figures which hurts the majority of casual dining same-store sales, as they typically see lower weekly sales due to the holiday. California was the best performing region during the month, with same restaurant sales up +0.7% and same-restaurant traffic down -3.4%. NY/NJ was the worst performing region, with both same-restaurant sales and same-restaurant traffic down -5.5% and -8.1%, respectively.

In aggregate, December numbers imply that same-restaurant sales and same-restaurant traffic were down -0.1% and -2.3%, respectively, in 4Q13. This suggests that casual dining chains continue to lose share to fast casual and fine dining chains, both of which had positive same-store sales in the quarter.

On an annual basis, same-restaurant sales and same-restaurant traffic were down -0.1% and -2.1%, respectively, in 2013.

One bullish data point, however, is the 2 point sequential acceleration in the Restaurant Willingness to Spend Index (which resembles consumer willingness to spend). At 95, this marks a 3-year high in the index suggesting consumers are willing to eat out. Unfortunately, these consumers appear to be frequenting chains outside of the casual dining industry.

Clearly, December was a let-down month for the industry after a solid October and November and, judging by the weather thus far, we suspect January will be another difficult month.

IS THE STREET TOO BULLISH?

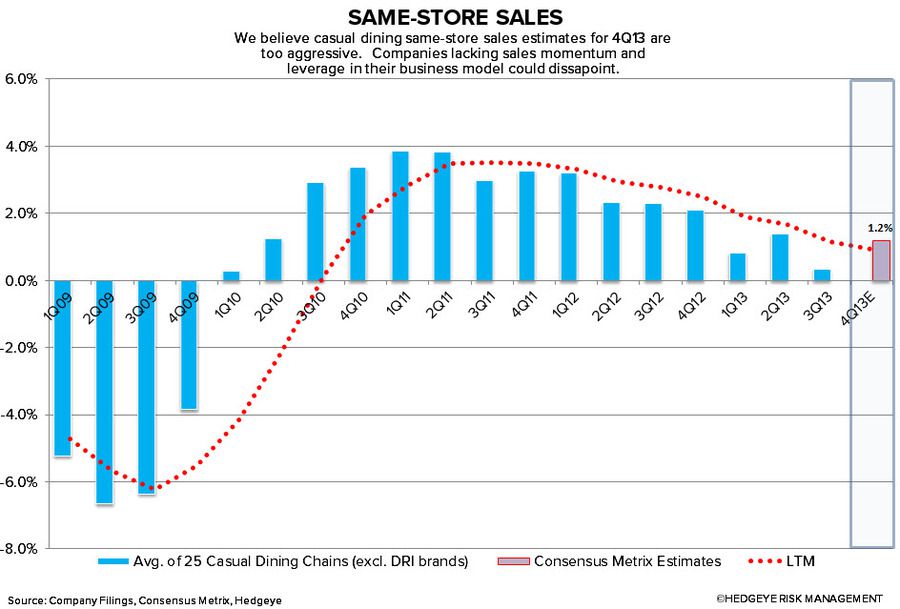

What is remarkable is that despite Knapp estimates indicating same-restaurant sales will be down -0.7% in 4Q and Black Box estimates indicating same-restaurant sales will be down -0.1% in 4Q, our index (composed of Consensus Metrix estimates for the 25 casual dining chains we track) indicates the street is expecting +1.2% same-restaurant sales growth in the quarter. This is further evidenced by the fact that only 6 out of the 17 casual dining companies we track had their same-restaurant sales estimates revised down over the dreadful month of December. In our opinion, the street appears to be disconnected from reality.

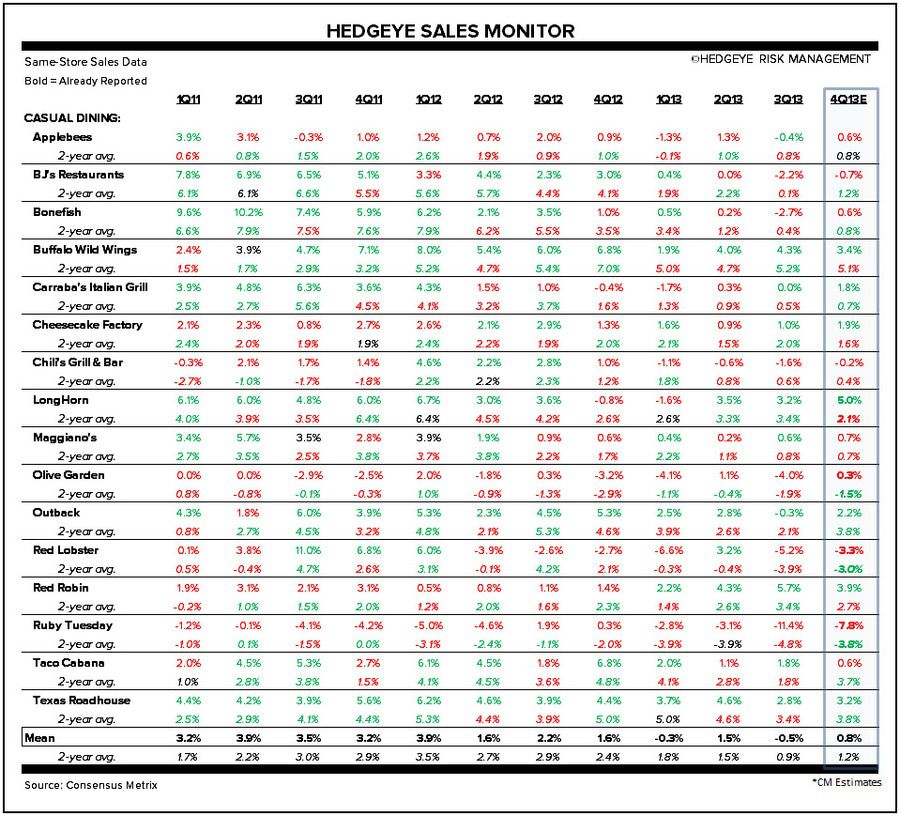

Below, is our Hedgeye Sales Monitor for the casual dining sector. Same-store sales are color coded green (if above) or red (if below) the sub-sector's mean. 2-year averages are color coded green (if accelerating) or red (if decelerating) on a sequential basis.

Howard Penney

Managing Director