MEDNAX is coming up against some difficult comparisons in their Q413 report. In fact, births face the toughest compare in the last six years when they report numbers and guide Q114.

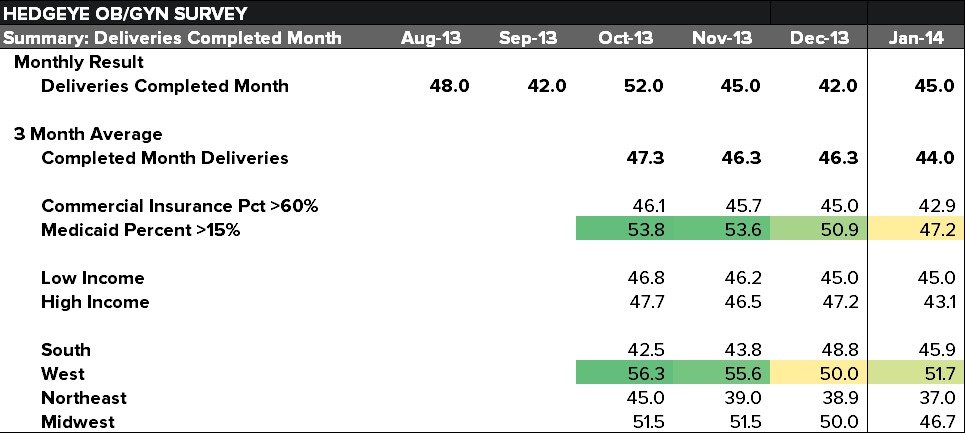

Our recent physician survey is telling us births are likely down in the US in Q413. A second quarter in a row of negative year over year organic growth, and likely worse sequentially than Q3, is not a risk we want to take.

Meanwhile, sellside sentiment is falling, which is negative for MD shares. The sellside actually does a good job on MD, unlike most other stocks.

Bottom line: Most of our catalysts to the upside seem played out. We'd rather sidestep the quarter and take another crack at the name from a lower price and lower expectations.