Europe is ringing in the New Year with some impressive data!

As a continuation of our top Q4 2013 Global Macro Theme, #EuroBulls, which outlined a bullish outlook on the GBP/USD and bullish positioning on UK and German equities, below we show updates to some of the charts we’re tracking that are supportive of our investment position around this theme.

In the Real Time Alerts Portfolio we’re currently long German equities via the etf EWG and long the GBP/USD (FXB). To get exposure to the UK equity market, we’ve traded the etf EWU in the past.

Eurozone

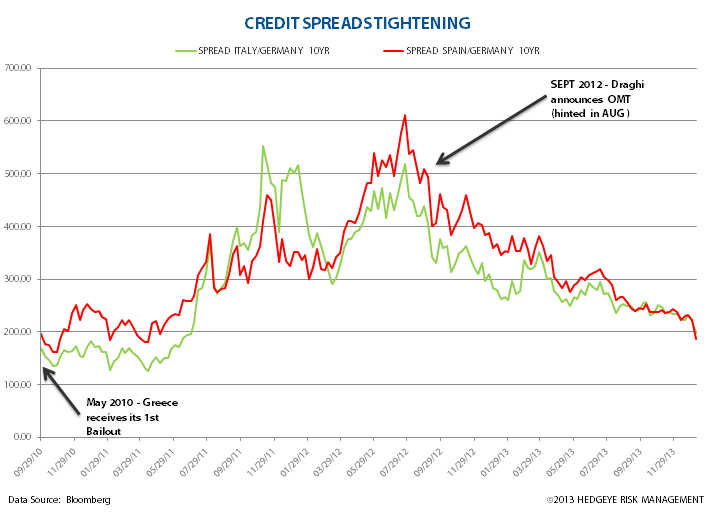

Steady as She Goes: broadly we continue to see a reduction in the risk profile across sovereigns and banks. Telling is that the Spanish 10YR bond is trading at 3.76% as its Italian counterpart is at 3.86%, and that both have reached spreads with the German Bund of under 200bps – back to where levels stood when Greece required its first bailout back in May 2010!

Meanwhile, the ECB continues to be highly accommodative with the main interest rates at 25bps. The ECB meets as soon as tomorrow to discuss any changes to monetary policy. Despite the media’s ‘deflationista’ frenzy around the inflation level (currently at 0.8% Y/Y in December and down 10bps since last month), we think President Draghi has well outlined the Bank’s forecast for an extended period of low inflation (below its 2% target). We think the next move from the ECB could be policy measures aimed at stoking real growth to SMEs through loan mechanisms, however not via another rate cut this quarter. We believe this position, as well as its continued posture of “ready and willing to act” (to ensure the survival of the Eurozone at any cost and keep financial conditions accommodative) will continue to support the common currency and strengthen investor confidence in the equity market.

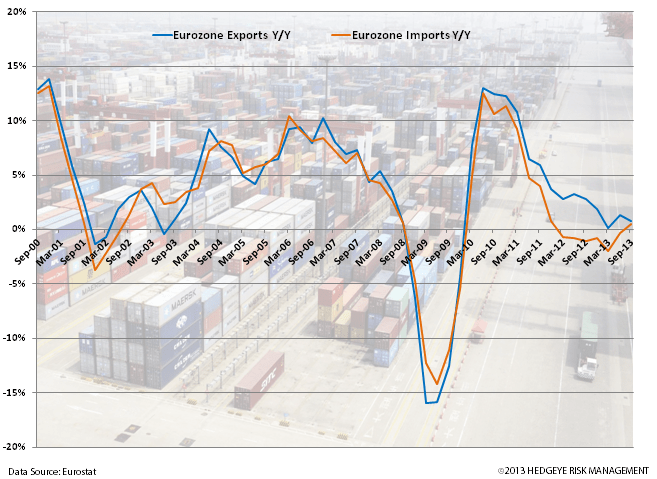

Additionally, despite the Eurozone unemployment rate at a high and sticky 12.1%, we expect lower levels of inflation to help spur exports, consumer spending and broader confidence. Eurozone aggregate Services and Manufacturing PMIs have shown slow and steady progress, as have retail sales and car orders, which we expect to continue in Q1.

UK

- Strong UK: we remain bullish on the British Pound/US Dollar and the UK equity market. Our positioning is supported over the intermediate term TREND by prudent management of interest rate policy from Mark Carney at the BOE (oriented towards hiking rather than cutting as conditions improve) and the Bank maintaining its existing asset purchase program (QE). We expect the FTSE (up +14.4% last year) to be pushed higher on continued evidence of emergent strength in the economy. In many cases, the UK’s high frequency data is outperforming that of its western European peers, including PMIs. We believe that a moderation in CPI should spur consumer spending and that a strong Pound should bolster spending power.

- UK Office of Budget Responsibility in its Autumn Statement revised higher its 2014 GDP outlook, to +2.4% vs prior +1.8% and 2014 CPI at +2.3% Y/Y vs prior +2.4%.

- We outline our levels on the GBP/USD below, and believe a strengthening UK economy coupled with the comparative hawkishness of the BOE (vs. Yellen et al.) will further perpetuate #StrongPound over the intermediate term.

Germany

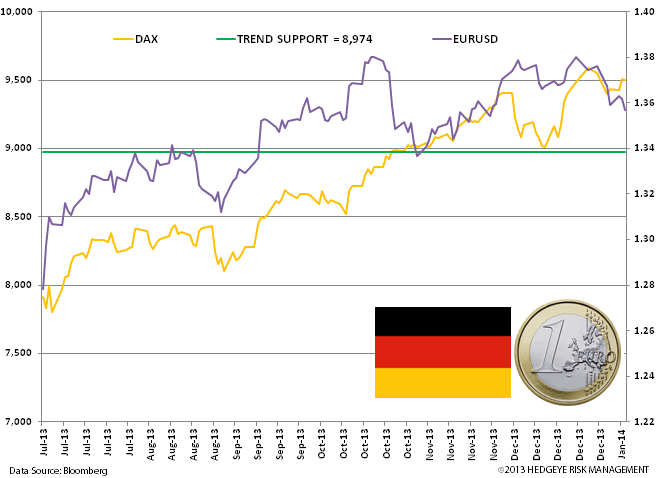

- Strong Germany: we continue to like the DAX (up +25.5% last year), which we’re currently long of via the etf EWG. Fundamentals remain grounded with a low unemployment rate (6.9% vs 12.1% in the Eurozone), CPI at 1.2% Y/Y in DEC (vs 1.6% in NOV) that is aiding exports, alongside strong PMIs and consumer and business confidence, and an inflection in factory orders to the upside.

- Merkel consolidated her coalition late into 2013 – we expect Germany to remain the fiscal hawk vis-à-vis sovereign and bank policy.

- The upward revision in the Bundesbank’s 2014 GDP forecast last month, to +1.7% vs prior +1.5%, is in line with our bullish outlook.

Matthew Hedrick

Associate