In what must have been a time consuming exercise in data management (even by our standards), a study titled Worrying about the stock market: Evidence from hospital admissions by Joseph Engelberg and Christopher A. Parsons combed through 30 years daily hospital admissions and stock market data. The authors make a remarkable conclusion on page 27:

"Over roughly three decades, we provide evidence that daily fluctuations in stock prices has an almost immediate impact on the physical health of investors."

If stock market declines can put you in the hospital, maybe feeling bad (low confidence) really makes you feel bad!

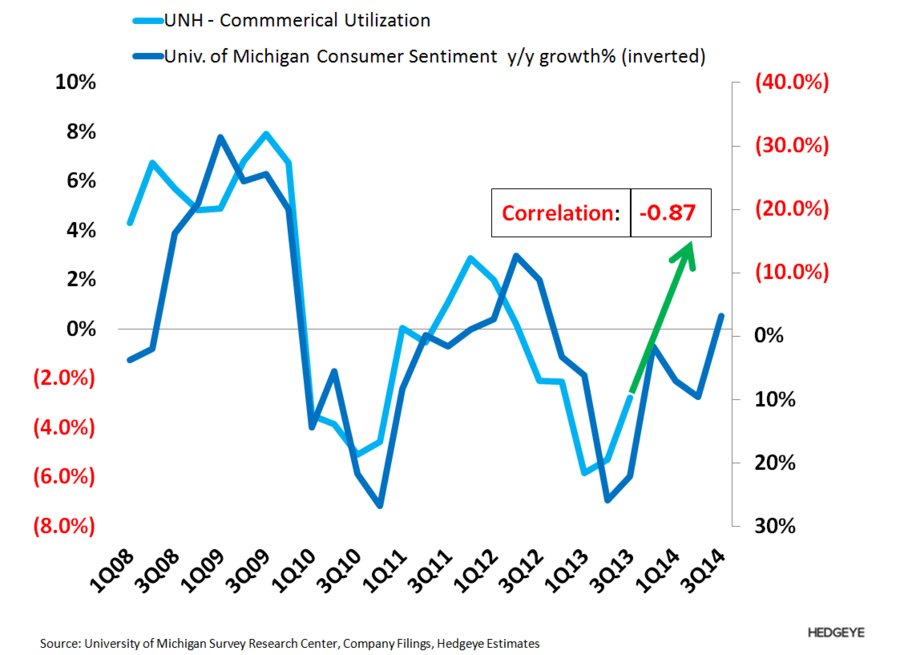

Charts and data can sometimes show you something that just doesn't "feel" quite right. In this case, we are talking about the inverse relationship between medical spending and Consumer Confidence. It's not new to us, but it's been easy to ignore, despite consistently showing up in multiple analysis across multiple durations and multiple company and economic factors.

So, does a happy consumer go to the mall, while an unhappy one goes to the doctor? It may be more true than we previously thought.

Check out the chart below.

It reveals just how tight the relationship is. Specifically, that changes in Consumer Confidence lead Medical Utilization by 2 to 3 quarters. The trajectory forecasts accelerating medical utilization for 2014.