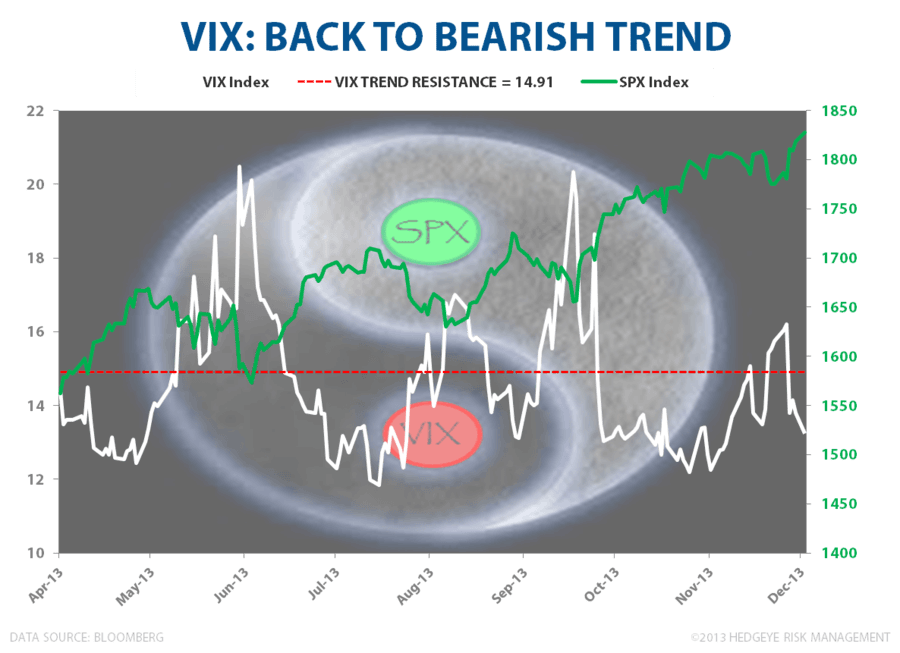

Volatility (VIX) was down -12.5% last week. It's back into crash mode for 2013 (down -23.5% year-to-date) alongside Gold.

Both of them hate the whole #RatesRising on growth surprising to the upside thing.

More importantly, the VIX is under our 14.91 Hedgeye TREND line again. That of course is bearish for the VIX.

Editor's note: This is an excerpt from Hedgeye's Monday morning research. For more information on how you can join the revolution click here.