A while back I referred to Japan as a man treading water with a bowling ball in his hands. Since that time the situation has remained unchanged.

With production and exports at record lows and rising unemployment, the stimulus measures that the Aso administration is attempting to use to expand domestic demand look to us as insufficient to move the dial significantly.

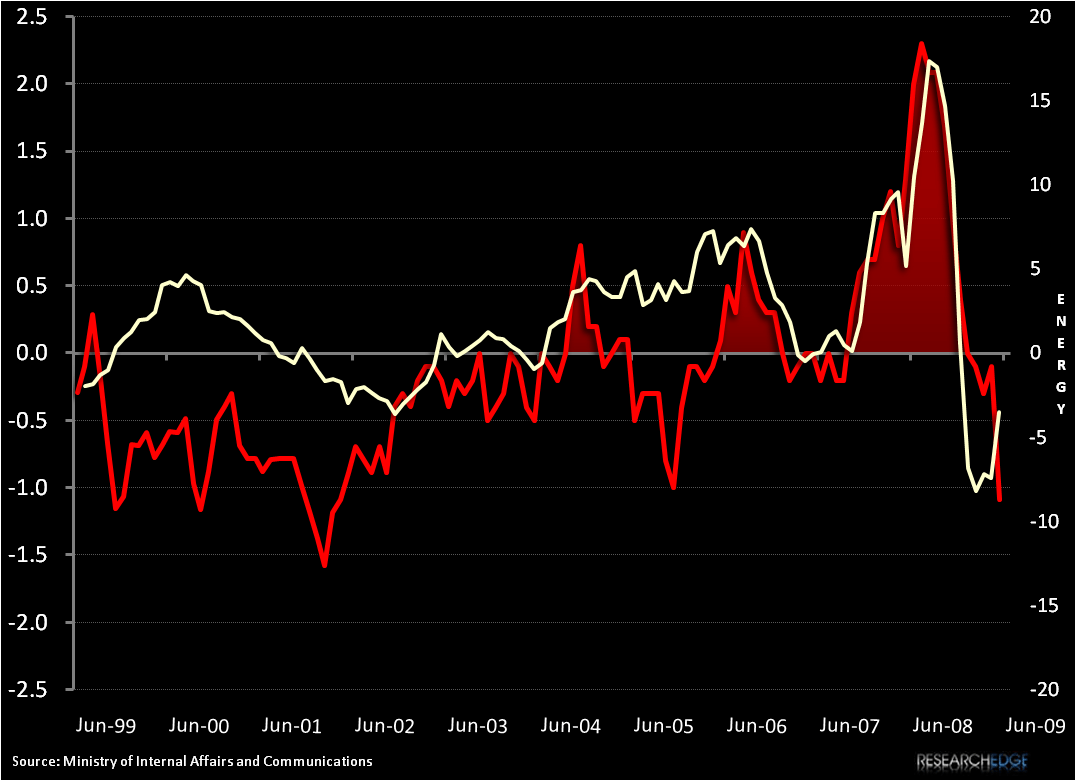

Today's CPI figures showed a 1.08% Y/Y decline, with Tokyo specific slightly higher at -0.78% and prices excluding Food and Energy registering at -0.5% . With the threat of deflation weighing heavily on the minds of central bankers who have memories of the "lost decade" still fresh in their minds the only way forward will be to continue to pump money into the system -essentially throwing things at the wall until something sticks.

Another prolonged period of stagnation would be catastrophic for Japan as the pronounced demographic shift that is looming gets underway. Remember that as Japanese debt levels have been climbing towards 200% of GDP, the glass-half-full crowd has reminded everyone that all of that debt is held by domestic investors. As the aging Japanese population starts to drain savings and the tax base shrinks, there will be fewer consumers who will be keeping their money parked at banks that pay zero on deposits so that those banks can turn around and buy government bonds that pay barely more.

We remain negative on future prospects for the Japanese economy, but think that the equity markets there could still get a big boost from a weak yen.

Andrew Barber

Director