This note was originally published at 8am on December 05, 2013 for Hedgeye subscribers.

“There is no one left, none but all of us.”

-S.S. McClure

So I was in my homeland (Canada) yesterday meeting with some free-market capitalists and couldn’t help but think of what it felt like when I came to this country in the early 1990s - liberating.

Other than the Chris Farley looking mayor dude who did crack, Toronto, Ontario seemed void of what dominates our market lives in today’s USA. There’s no “taper-talk.” There are no professional politicians and TV pundits gorging on the uninformed.

As I boarded the plane back to beautiful Newark, New Jersey, I sighed. Then I cracked open a new book, and felt better again. In the preface to Doris Kearns Goodwin’s The Bully Pulpit –Theodore Roosevelt, William Howard Taft, and The Golden Age of Journalism, she reminds us of what objective research and reporting used to be. I smiled again. This is our opportunity.

Back to the Global Macro Grind …

“As S.S. McClure well understood, the vitality of democracy depends on popular knowledge of complex questions” (The Bully Pulpit, pg XIV); not using complexity, policy, and demagoguery, as a political Trojan horse to obfuscate the truth.

Albeit I’m just a man with my team in a room, that’s my solemn commitment to you – providing you an objective research view of the truth. To be clear, this is not a position in life I always longed for – it’s simply the position I find myself in.

Even though he went to Harvard, for a long-time I’ve respected Teddy Roosevelt via a paper one of my freshman guidance counselors (who I was older than at the time!) put on my desk when I first got to Yale – The Strenuous Life. If you ever feel like you’ve lost your moral compass, re-read that – and read it again. It does the soul good.

Moving along…

Buying-the-damn-bubble #BTDB may not be chicken soup for your soul, but it has certainly paid the bills in 2013. From a behavioral market practitioner’s perspective, I have developed an affinity for doing precisely the opposite of how I think this ultimately ends. Weird, but it works.

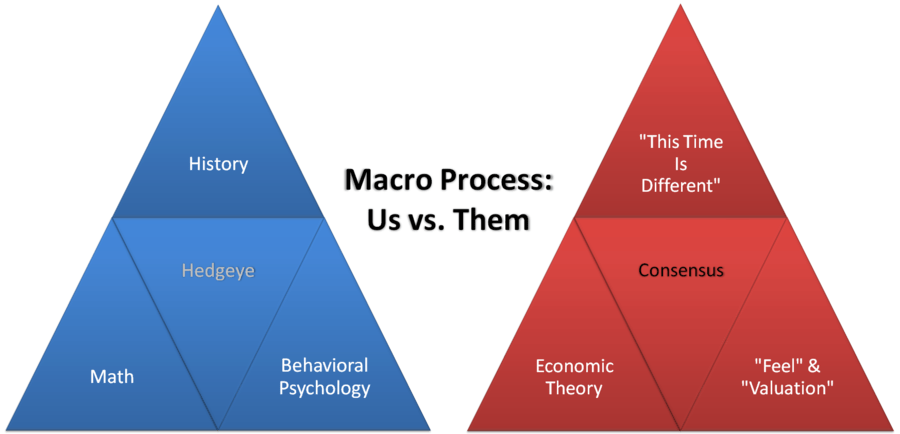

To review, the multi-disciplinary triad of our Global Macro Research Process, there are 3 big parts:

- History

- Math

- Behavioral Psych

History provides us context (economic/market patterns, mean reversion risk, etc.); math (fractal dimensions and risk ranges) signals timing; and behavioral, well, that’s a learning process.

How else would you define what it is that you do? Other than Embracing Uncertainty and constantly re-evaluating your position relative to the information surprise (price, volume, volatility) of the day, is there an alternative to mental flexibility? There isn’t for me. I’m not smarter than the market. And it took me a good long while to accept that.

In terms of our current strategy, quite simply put in our Q413 Macro Theme of #GetActive, it’s to do just that. Unaccountable and un-elected @FederalReserve policy making means we need to engage in unconventional market strategies.

In practice, in our Hedgeye Asset Allocation Model, what does that mean?

- At the US stock market highs we moved to 58% Cash (last Friday)

- After a 4-day US stock market correction we moved back to 42% Cash

Don’t lose the message of mental flexibility in the absolute numbers. If you want to be in 90% cash or 10% cash makes no difference to the point I am trying to make. It’s how you move on the margin that counts. I call it Fading Beta.

Looking at it from a different perspective (different Hedgeye product - #RealTimeAlerts):

- Last Friday (on green) we moved to 5 LONGS, 5 SHORTS

- Into yesterday’s close (on red) we moved to 11 LONGS, and 3 SHORTS

Again, the point here is about the process. My process is far from perfect. But at least I can explain, evaluate, and evolve it. Doing that in an open network of client feedback has made me a more responsible and accountable investor.

So why can’t we do that running America? Wasn’t the whole marketing pitch “Yes We Can”? Or, somewhere along the way towards truth, did we put political reputations and excuse making ahead of your country’s learning process?

How do you ever learn if you’re constantly on a quest to prove that you’re never wrong? If there’s one question I’d ask one of the most conflicted and compromised outcrops of Big US Government Intervention (the power of the Fed), that would be it.

And that’s all I have to say about that. It’s time to grind and get on with my day. It’s time for you to get on with yours. Thanks again for taking the time to read what I have to say. Teddy wrote it much more eloquently, but you’ll get the point:

“… our country calls not for the life of ease but for the life of strenuous endeavor. The twentieth century looms before us big with the fate of many nations. If we stand idly by, if we seek merely swollen, slothful ease and ignoble peace, if we shrink from the hard contests where men must win at hazard of their lives and at the risk of all they hold dear, then the bolder and stronger peoples will pass us by, and will win for themselves the domination of the world. Let us therefore boldly face the life of strife, resolute to do our duty well and manfully; resolute to uphold righteousness by deed and by word; resolute to be both honest and brave, to serve high ideals, yet to use practical methods. Above all, let us shrink from no strife, moral or physical, within or without the nation, provided we are certain that the strife is justified, for it is only through strife, through hard and dangerous endeavor, that we shall ultimately win the goal of true national greatness.”

Our immediate-term Global Macro Risk Ranges (see our Daily Trading Range product for all 12):

UST 10yr Yield 2.76-2.85%

SPX 1788-1811

DAX 9128-9411

USD 80.45-80.91

Pound 1.62-1.64

Gold 1217-1259

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer