Yesterday Russian President Vladimir Putin announced an agreement to loan the Ukraine $15 Billion and reduce the cost of natural gas exports by one-third. Will this quell the weeks of protests against Ukrainian President Viktor Yanukovych’s government?

While publically there was no talk of the Ukraine joining Putin’s custom union (for trade) – which already includes Kazakhstan and Belarus and is a contentious issue for the “Western” protesters – make no mistake that with this agreement Russia has reconfirmed its dominance over the Ukraine, and with it won a key geopolitical victory. For the Ukraine, it spells years, if not decades, before real reform (political and economic) may be realized.

Our Position: despite heavy foot power (protests) against President Yanukovych over the last four weeks, we do not expect dissent to topple government leadership that is orientated to the East (Russia). This view is built on several factors, including the unwillingness of the EU to fully commit to bringing the Ukraine into the EU, or conversely meet the sway of Putin to fold the Ukraine under its geographic empire. What Russia can provide in funds (both directly and through gas subsidies) we don’t foresee the EU attempting to match, and this balance of payments should reinforce existing strong levels of political corruption (beyond just the President), supported by a sizable proportion of the populous that identifies with the East. Further, unlike during the Orange Revolution, there is no clear organized opposition (merely disparate dissenters), all of which suggests to us that while protests may continue, there’s low probability that Yanukovych’s rule is toppled (especially following the deal with Russia) and a high probability that the Ukraine maintains its alliance with the Kremlin for the foreseeable future.

Below we note historical background, critical developments, and analysis aided by sources in the region to contextualize the protests:

- Protests Beyond Just A Trade Agreement. While Yanukovych’s decision last month (21 NOV) to reject a trade deal with the EU (that had been in the works for a number of years) sparked the largest protest since the Orange Revolution in 2004, the dissent is rooted in opposition to years of crony capitalism, centered around a small group of oligarchs and government heads profiting from the state at the hands of the population.

- The Orange Revolution Failed. The 2004 Orange Revolution ushered in great hope for the ideals of the West: democracy and reform in the spirit of the EU institution, but the Revolution failed. Yulia Tymoshenko, with her camera-friendly crown of blond locks, and Viktor Yushchenko, with his discolored and uneven face after being poisoned by the opposition in 2004, were strong faces and voices of the Orange Revolution. The protests led to the defeat of Yanukovych in a forced second run-off election that ushered in Yushchenko as President and Tymoshenko as his Prime Minister in early 2005. While their leadership brought great “hope” that the country could have its Berlin Wall or Solidarity moment, their stars faded quickly (along with hope of real reform) under the weight of a corrupt state.

- Tables Turned. By 2010, Yanukovych won back the Presidency. By this time, Tymoshenko was surrounded by controversy and suspicion over gas contracts that she arranged with Russia in 2009: allegedly she agreed to inflated gas prices (which hurt the nation and led to shutdowns) in return for political favors and personal profit. Even Yushchenko testified against her in 2011 and Yanukovych sentenced her to a 7 year term in 2011 – a position the EU decries as “unjust” without substantiating with refuting evidence. Yanukovych’s rule since his reelection has been marked by the further consolidation of power and wealth, going so far as to take out certain leading businessmen (and oligarchs), redistributing assets and leadership positions to an inner circle of family members and a close cadre of “extended” family.

- Economic Plight. The economy has unraveled under Yanukovych. GDP has gone from its last high of +5% at the end of 2011 to -1.3% as of Q3 2013. Pressing is an underfunded government (deficit around -8.5% of GDP) with plunging foreign reserves. The country is estimated to have $17 Billion of debt payments due in the next two years, hence the importance of a bridge loan from Russia/EU. The government’s mismanagement of the economy has also included a lack of infrastructure spending and investment, equating to the erosion of living standards, while chasing away foreign investment on fears of sovereign default.

- No Opposition Leadership over Divided Kiev. Recent demonstrations illustrate that unlike the Orange Revolution, there’s no united leadership in the opposition parties. The contenders are made up of: Arseny Yatseniuk (leads the party formerly headed by Tymoshenko), Vitaly Klitschko (a boxing champion that heads the Udar “punch” party), and Oleh Tyagnibok (a right-wing nationalist). All of them claim to have not seen the protests coming.

- Ukraine and Kiev Remain Divided. A country with a population of 46 million, the western half of the country aligns itself politically with the West (Europe) and has the highest concentration of native Ukrainian speakers, whereas the eastern half aligns itself with the East (Russia) and primarily speaks Russian as a first language. Kiev, the capital and largest city, is located centrally to the north, and is itself a very divided city both politically and linguistically. The recent demonstrations suggest that protesters have numbered anywhere between 100K to 600K, but the city remains divided. Reports suggest the protests have a grass roots organization “feel” that lack strong polarizing leadership and have been mostly met by non violence from the government/police, with no recorded deaths. While the protests have been taking place, as recently as December 3rd, Yanukovych’s government survived a no-confidence vote.

- Russian Interests. Russia is looking out for its national security interests first and foremost and using its stranglehold on natural gas as a bargaining chip. If Ukraine is under the influence of the EU, Russia is vulnerable to the south. Ukraine also represents an important natural gas transit country for flows to Europe, and a Ukraine under Russian influence helps to solidify Putin’s desires for a trading union. Given that Putin has done nothing to diversify his own economy in the last 12 years, he’s left with few options to exert his political clout beyond straight arming former Soviet satellite countries into his sphere of influence.

- EU Interests. For the EU, the Ukraine is of less importance from a security perspective, unless it is looking to invade Russia (unlikely). Like Turkey, the Ukraine is geographically at the fringe of Europe. Given the experiences of the Eurozone ‘crisis’ and tail of slow growth alongside political indecision (there are now 28 separate parliaments and 18 Eurozone countries), we do not envisage the EU yearning to add a historically highly corrupt government to its roster.

- Russia Terms. To plug the country’s balance of payments deficit (for an estimated 18-24 months) Ukraine will issue $15 billion of Eurobonds which Russia will purchase from its National Wellbeing Fund containing $88.1 billion – the first tranche of $3 billion is expected as soon as year-end. In addition, the discount given to the Ukraine on natural gas, from current prices of around $400 per thousand cubic meters (tcm) to $268.50 tcm, is worth another $3 billion in subsidy. While Yanukovych did not sign off on entering Putin’s custom union (which Kazakhstan and Belarus have joined and which reeks of attempts to get the old Soviet gang back together), expect that this deal didn’t come without terms. Besides the national security piece that Russia receives, our guess is Putin will run the Ukraine’s PR campaign – he will decide if and when the Ukraine should enter his custom’s union.

Conclusion - Tipping East. The Ukraine remains a state uncomfortable with addressing its own sovereignty, preferring to be aligned. In our analysis, the Kremlin remains Yanukovych’s preferable partner over the EU given 1) Putin’s ability to quickly write a check (to cover the government’s liabilities), 2) his reelection aspirations for 2015 and ability to “win” cheaper, uninterrupted heat for the nation, 3) the cultural affinity to the East, including a significant percentage of the population that identifies with Russian rule and to some extent nostalgically yearns for a return to the Soviet days, 4) the likely harsher terms the EU and international organization could offer in exchange for loan packages, and 5) the lukewarm reception of the EU to fold the Ukraine into the EU.

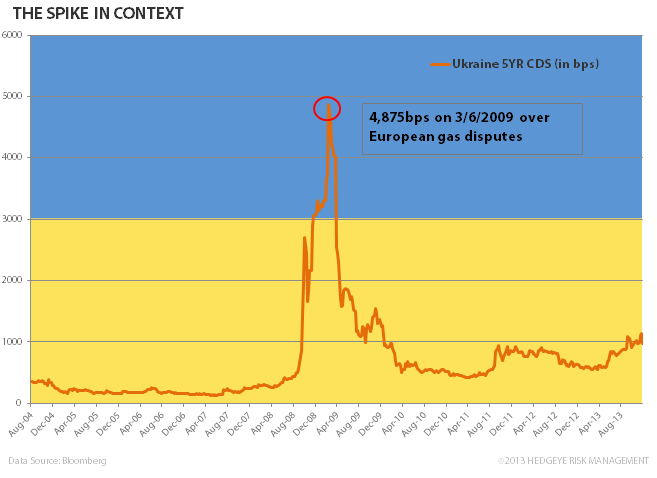

If we look to the market for its risk assessment, as expected following yesterday’s deal Ukrainian CDS and sovereign credit yields dropped in a hurry. What’s interesting, however, comes from the second chart below that shows Ukraine’s 5YR Sovereign CDS pulled back on a historical basis (to its maximum based on Bloomberg data). Here it’s clear that while risk was being priced up into the event (1st chart), the absolute level is a moon shot from all-time highs in March 2009, a period when Western European nations had to negotiate with Russia over gas shut-down to their countries that was being pumped through the Ukraine. What this signals to us is that the EU community will only get its hands dirty in the interests of Ukraine when it stands to clearly and personally receive benefit. The “failures” of these protests for change and the muted response from the EU suggest to us that the Ukraine is far from what could be tipping point levels. Russia will remain its puppet master.

Matthew Hedrick

Associate