TODAY’S S&P 500 SET-UP – December 13, 2013

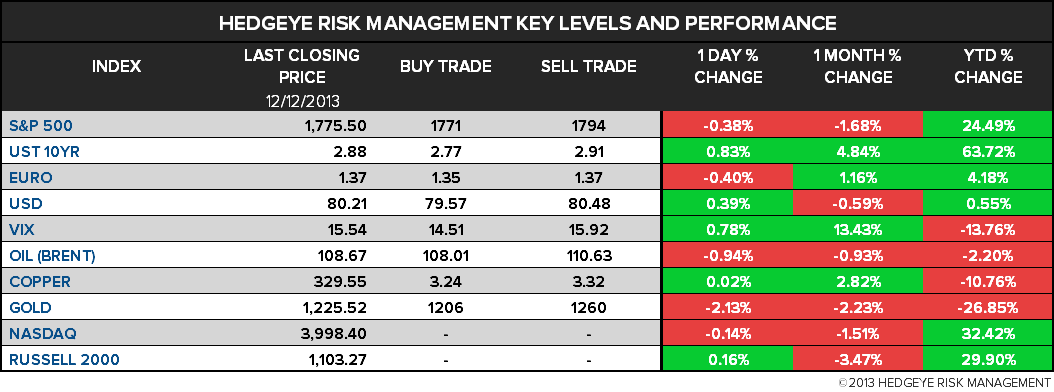

As we look at today's setup for the S&P 500, the range is 23 points or 0.25% downside to 1771 and 1.04% upside to 1794.

SECTOR PERFORMANCE

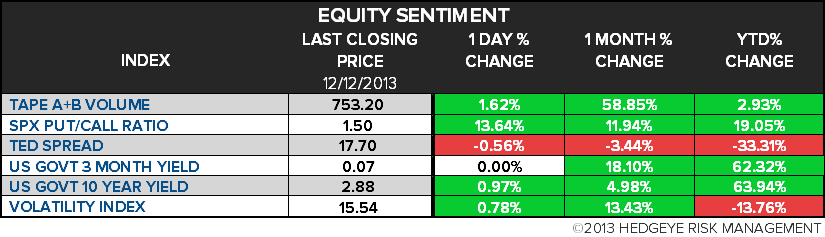

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 2.55 from 2.56

- VIX closed at 15.54 1 day percent change of 0.78%

MACRO DATA POINTS (Bloomberg Estimates):

- 8:30am: PPI m/m, Nov., est. 0.0% (prior -0.2%)

- 8:30am: PPI Ex-Food/Energy m/m, Nov., est. 0.1% (pr 0.2%)

- 1pm: Baker Hughes rig count

GOVERNMENT:

- 8am: Medicare Payment Advisory Commission holds mtg, with sessions on Medicare Advantage, hospice svcs, rehabilitation

- 10am: CFTC holds closed mtg

- 11am: Senate Finance Cmte votes on nominations: Sarah Bloom Raskin Deputy Treasury Sec.; John Andrew Koskinen IRS commissioner; Rhonda Schnare Schmidtlein ITC member

- 1pm: Panel of President’s Export Council meets on encouraging trade, incl Export control reform update

WHAT TO WATCH:

- Ford to hire 11,000 in U.S., Asia next year with new plants

- SAC reconsidering relationship with Deutsche Bank: WSJ

- Steinberg told by judge to decide whether he’ll testify

- U.S. House passes $625.1m defense authorization bill

- Microsoft said to consider Qualcomm’s Mollenkopf for CEO

- Anadarko may be liable for up to $14b from Tronox spinoff

- Boeing says it has evaluated 54 sites for newest 777 work

- KKR, Goldman said to exit stakes in Dollar General: WSJ

- Texas Indus. said to explore sale as construction rebounds

- DirecTV said to be near deal to extend NFL Sunday Ticket

- RRJ Capital buys Everbright Intl. stake for $350m

- Hilton exploring new lifestyle hotel brand, WSJ says

- Calpers criticizes Carl Icahn’s push for Apple cash return

- Coke makes management changes to improve North America ops.

- Wetjen said to face vote to become acting CFTC head

- Mexico’s 2 legislative chambers pass energy reform bill

- China to take deposits on some U.S., Japan, EU steel imports

EARNINGS:

- No earnings scheduled for S&P 500 companies

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Gold Swings as Investors Weigh Demand Signs Against Fed Outlook

- Crude Declines in Survey as Fuel Supply Grows on Weaker Demand

- Copper Bulls Extend Run as Tight Supply Lifts Price: Commodities

- Freeport Working With Indonesia to Clarify Planned Export Ban

- Palm Oil Imports by China Climbing to Eight-Month High on Demand

- Copper Drops on Record China Output, Fed Stimulus: LME Preview

- Palm Oil Tumbles Most in Three Months as Demand Seen Weakening

- Rebar Caps First Weekly Loss in Four as Production Costs Fall

- Abe Breaks Micro-Farms to End Japan Agriculture Slide: Economy

- Amplats Agrees to Wage Deal With National Union of Mineworkers

- Eric Shi Said to Join Newedge in Commodities After Bank of China

- Shale Boom Shakes U.K.’s $32 Billion Chemicals Industry: Energy

- Rubber Set for Third Weekly Advance on Weak Yen, China Optimism

- Brent Set for Weekly Loss Before Reopening of Libyan Oil Ports

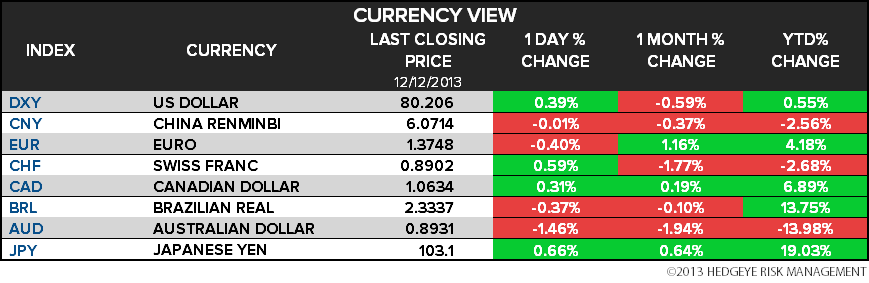

CURRENCIES

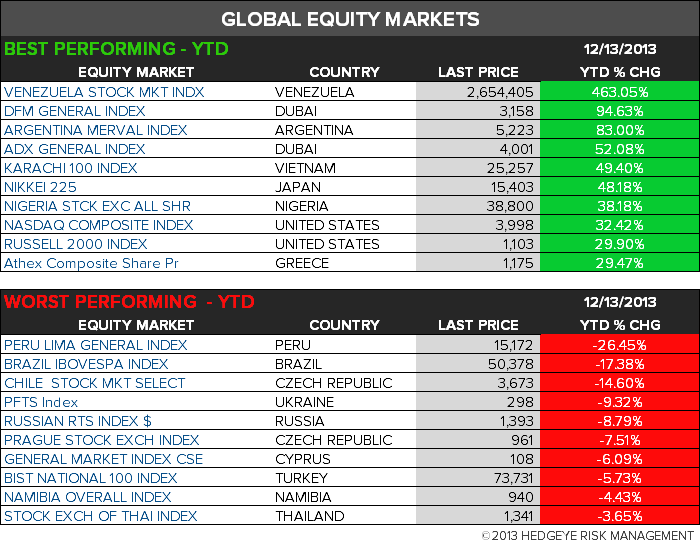

GLOBAL PERFORMANCE

EUROPEAN MARKETS

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team