Editor's note: This is an excerpt from a piece written by Hedgeye Financials Sector Head Josh Steiner. For more information on how you can subscribe to Hedgeye research click here.

Rising Rates Love Falling Claims

It's getting harder to ignore the improvement in the labor market, unless, of course, you're the Fed.

Increasingly, however, it seems as though the bond market is taking fewer cues from the Fed and more from the labor market. True, seasonally-adjusted initial claims have a 2-handle on them principally because of the Thanksgiving mismatch this week vs last year (a week later this year), but adjusting for that and all the other recent turbulence in the data reveals one unmistakable fact. The data continues to strengthen and the bond market is taking notice.

Aside from the obvious, which is that this is more good news for credit quality, the upward pressure being exerted on rates is ferreting out clear winners and losers, i.e. good for banks and online brokers, and bad for homebuilders and mortgage REITs. For more details, see our note from 11/22 "#Rates-Rising: A Current Look at Rate Sensitivity Across Financials."

Next week should be the first week in a long time where we get a clean print on the labor market, so stay tuned.

Nuts & Bolts

Prior to revision, initial jobless claims fell 18k to 298k from 316k WoW, as the prior week's number was revised up by 5k to 321k.

The headline (unrevised) number shows claims were lower by 23k WoW. Meanwhile, the 4-week rolling average of seasonally-adjusted claims fell -10.75k WoW to 322.25k.

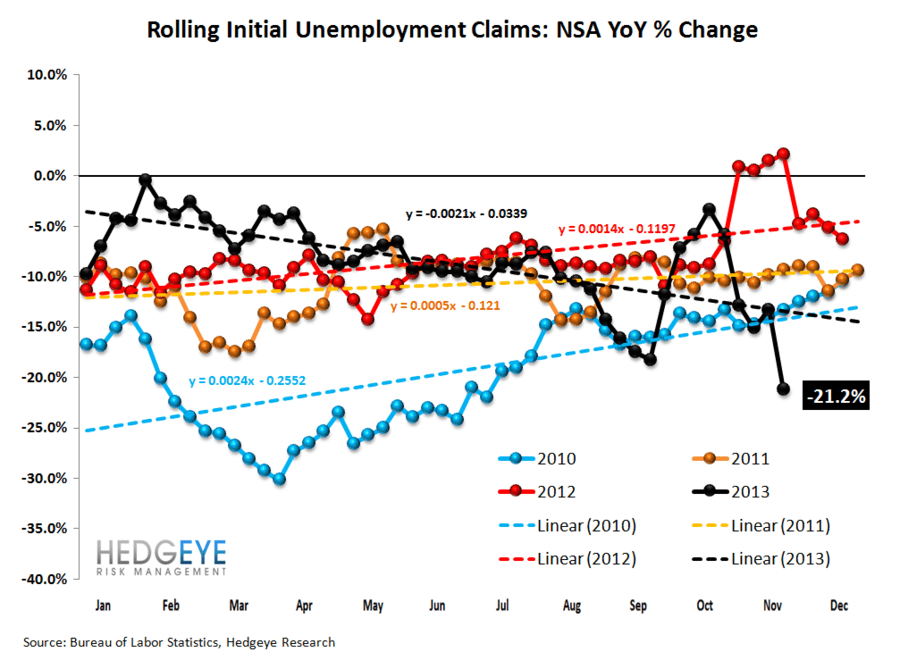

The 4-week rolling average of NSA claims, which we consider a more accurate representation of the underlying labor market trend, was -21.2% lower YoY, which is a sequential improvement versus the previous week's YoY change of -13.3%