TODAY’S S&P 500 SET-UP – November 26, 2013

As we look at today's setup for the S&P 500, the range is 17 points or 0.58% downside to 1792 and 0.36% upside to 1809.

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 2.43 from 2.45

- VIX closed at 12.79 1 day percent change of 4.32%

MACRO DATA POINTS (Bloomberg Estimates):

- 7:45am/8:55am: ICSC/Redbook weekly retail sales

- 8:30am: Sept., Oct. building permits; Oct. est. 930k

- NOTE: Oct. housing starts delayed until Dec. 18

- 9am: S&P/Case-Shiller 20-City m/m, Sept., est. 0.9%

- 9am: S&P/CS Home Price Index, Sept., est. 165 (prior 164.53)

- 9am: FHFA House Price Index m/m, Sept., est. 0.4% (pr 0.3%)

- 10am: Conference Bd Consumer Conf Index, Nov., est. 72.5

- 10am: Richmond Fed Manuf. Index, Nov., est. 4 (prior 1)

- 10am FDIC announces 3Q bank, thrift industry earnings

- 4:30pm: API weekly oil inventories

GOVERNMENT:

- House, Senate aren’t in session

- Obama to discuss economy during California visit; to meet with film studio chiefs, says Hollywood Reporter

- Supreme Court to issue list of cases it plans to take up

- Washington State genetically modified food labeling vote count expected to be completed

- Obama seeks Iran deal support; Reid says Senate my act

WHAT TO WATCH:

- FDIC’s Hoenig to weigh easing bank leverage rule he championed

- Berkshire said to cut Energy Future bond stake by a third

- Bayer in talks to buy cancer partner Algeta for $2.4b

- Samsung bid to put Apple patent case on hold rejected by judge

- Einhorn’s Greenlight Capital has $402m stake in Micron

- Silver Lake technology unit said to plan new $1b fund

- Intel said to seek $500m in sale of web-based TV startup

- Bain said in talks to sell Applied Systems for $1b+: Reuters

- Citi loses bid to block Abu Dhabi investment arbitration

- Sony says entertainment target conservative amid cost cut push

- China said to plan crackdown on banks’ loan limit evasion

- Prologis to lift Japan rents, build warehouses on Abenomics

- SpaceX delays rocket launch as Musk cites being “careful”

- Online gambling begins today in NJ

AM EARNS:

- Alimentation Couche Tard (ATD/B CN) 8:37am, $1.23

- Barnes & Noble (BKS) 8:30am, ($0.03)

- Beacon Roofing Supply (BECN) 8am, $0.62

- Brown Shoe (BWS) 7am, $0.59

- Chico’s FAS (CHS) 7:15am, $0.25

- Children’s Place (PLCE) 6am, $1.85

- Cracker Barrel (CBRL) 7am, $1.15

- DSW (DSW US) 7am, $0.58

- Eaton Vance (EV) 8:35am, $0.60

- Hormel Foods (HRL) 6:30am, $0.54

- Laclede Group (LG) 8am, ($0.07)

- Movado Group (MOV) 7am, $0.87

- Pall (PLL) 7am, $0.68

- Signet Jewelers (SIG) 6:30am, $0.42

- Tiffany & Co. (TIF) 6:59am, $0.58

PM EARNS:

- Analog Devices (ADI) 4pm , $0.58

- Hewlett-Packard (HPQ) 4:04pm, $1.00 -- Preview

- Infoblox (BLOX) 4:05pm, $0.09

- TiVo (TIVO) 4:01pm, $0.06

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Gold Fix Drawing Scrutiny Amid Knowledge Tied to Daily Eruption

- Frozen-Turkey Pileup Signals Thanksgiving Discount: Commodities

- WTI-Brent Crude Oil Spread Narrows for First Time in Five Days

- Soybeans Drop From Two-Month High on South American Crop Outlook

- Japan Dismantles Rice Output Policy as Abe Targets Farming

- Gold Swings Above Four-Month Low as Investors Weigh Fed Stimulus

- Copper Swings as Investors Weigh Demand View Against Drop Bets

- Sugar Drops to 11-Week Low in New York on Ample Supply Outlook

- Iron Ore Seen Dropping From Westpac to Goldman as Supply Expands

- Canada Grain Exports From Vancouver Seen Rising to All-Time High

- Brazil Ethanol Losing Competitiveness to U.S.: Chart of the Day

- Marcellus Goliath Transforms Region to Gas Trade: Energy Markets

- Copper Market Tightens in 3Q on Demand Rise, Output Decline

- Tate & Lyle Urges EU to Abolish a Sugar Duty as Bloc Quotas End

CURRENCIES

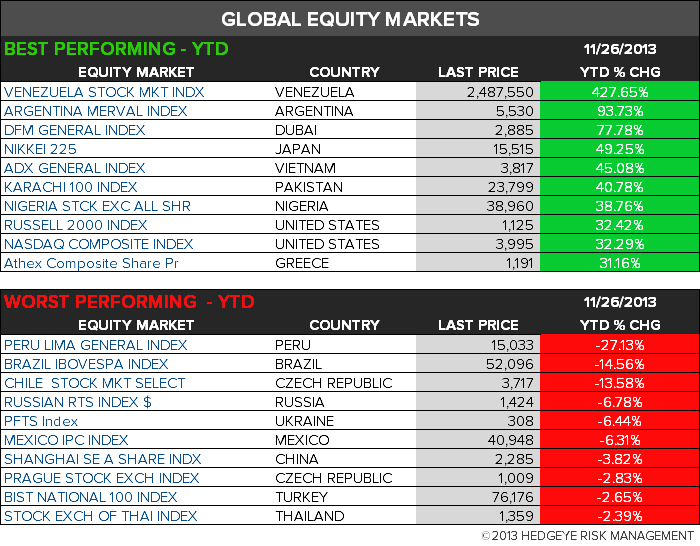

GLOBAL PERFORMANCE

EUROPEAN MARKETS

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team