The Tea Leaves Are Tough To Read At the Moment

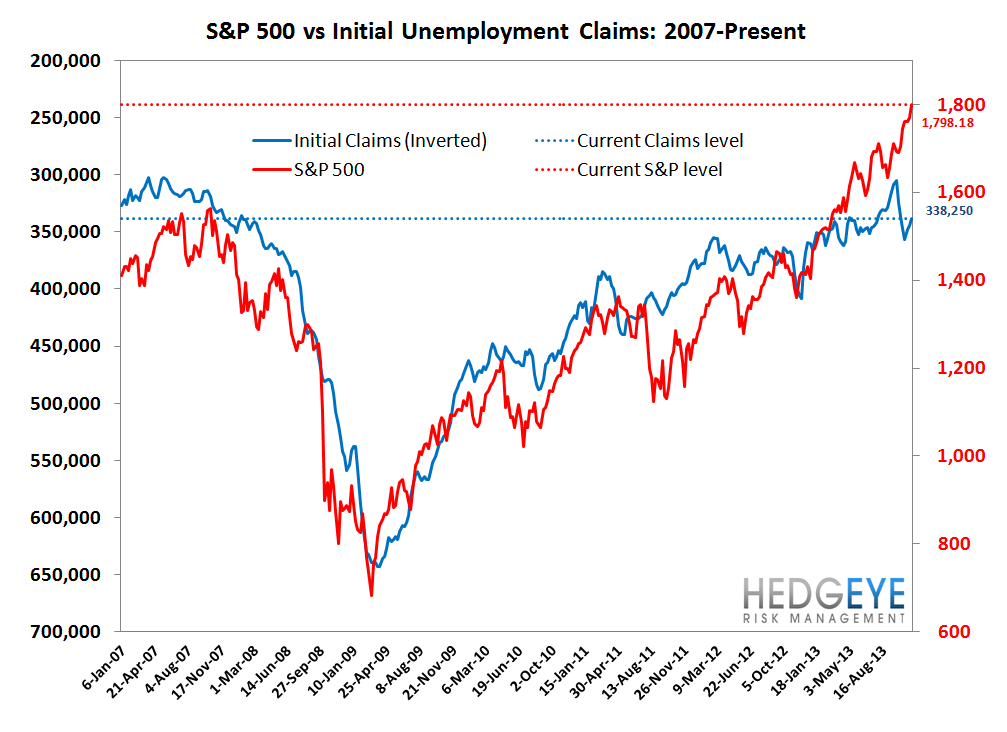

The initial jobless claims data this morning was good from a reported standpoint. Normally we like to see through the reported SA numbers by looking at the Y/Y trend in NSA claims, but unfortunately the distortions caused by Hurricane Sandy last year are reducing our precision in doing so. Our best estimate is that the Y/Y trend is down -7.7%, which is a modest deceleration from our estimate of -8.9% improvement in the prior week, but still in line with the longer-term trend of accelerating improvement. The SA data is likely the more informative measure here, in spite of the known distortions. The data showed a significant W/W improvement, but here again that number was likely clouded by the Veteran's Day holiday last week, which has distorted the data series in the past. Regrettably, it's hard to say with any good certainty whether the labor market inflected positively or negatively last week, though the SA numbers and our interpolated (Sandy-adjusted) NSA numbers suggest the trend of improvement that's been in place largely remained in place. The Sandy distortion should persist for another 2-3 weeks.

The Nuts & Bolts

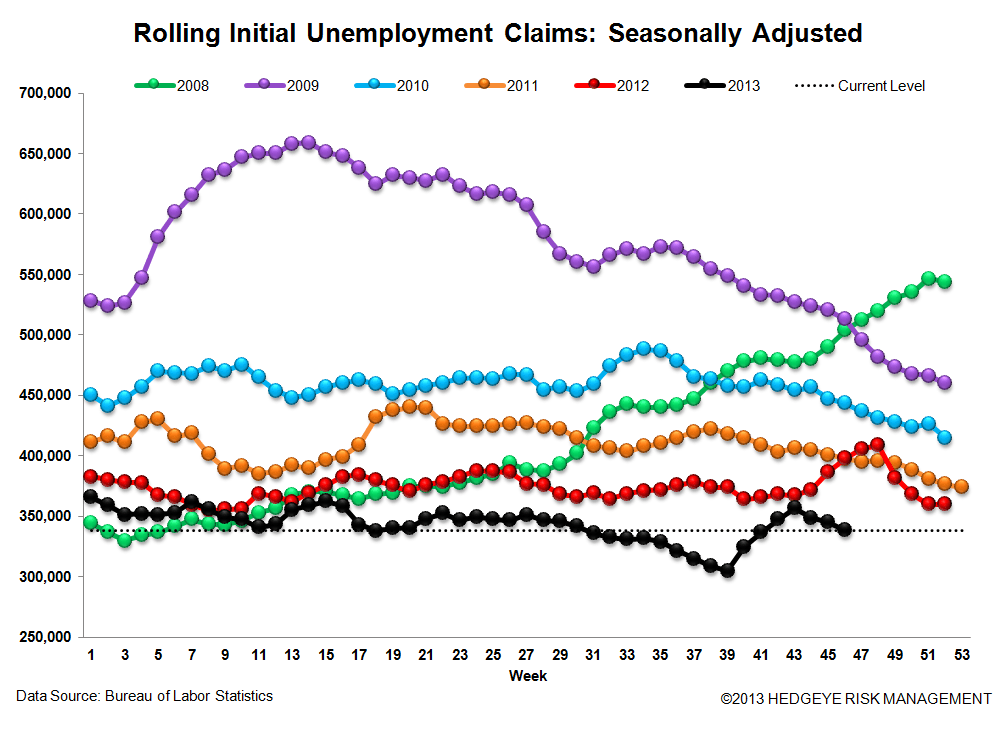

Prior to revision, initial jobless claims fell 16k to 323k from 339k WoW, as the prior week's number was revised up by 5k to 344k.

The headline (unrevised) number shows claims were lower by 21k WoW. Meanwhile, the 4-week rolling average of seasonally-adjusted claims fell -6.75k WoW to 338.25k.

The 4-week rolling average of NSA claims, which we consider a more accurate representation of the underlying labor market trend, was -15.3% lower YoY, which is a sequential improvement versus the previous week's YoY change of -12.9%

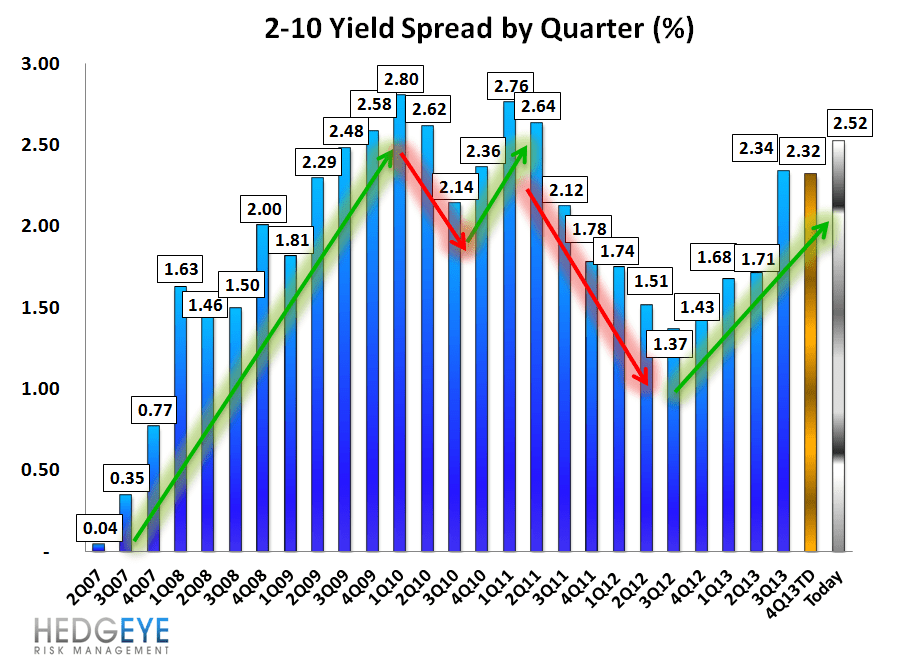

Yield Spreads

The 2-10 spread rose 13 basis points WoW to 252 bps. 4Q13TD, the 2-10 spread is averaging 232 bps, which is lower by 2 bps relative to 3Q13.

Joshua Steiner, CFA

Jonathan Casteleyn, CFA, CMT