Position: Tactically short on strength.

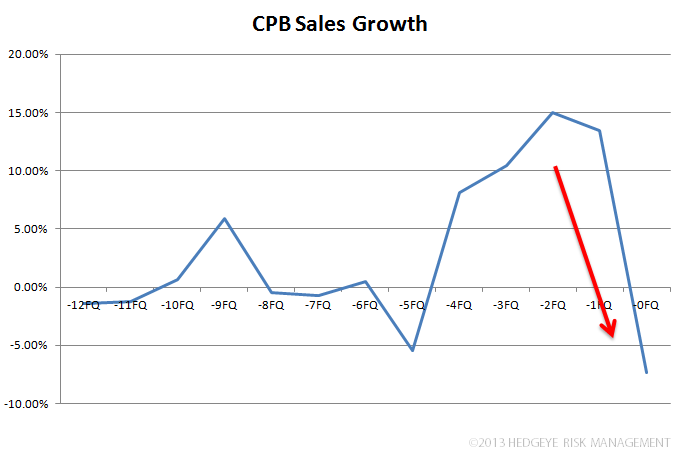

Campbell’s had a rough quarter to say the least; the stock is trading down -6% intraday on management lowering FY guidance.

Despite concerted efforts to reduce costs (CPB completed the sale of its European Simple Meals business, the exit of 4 plants in the past two years, and plans to save an additional $40 in FY 2014) we struggle to get behinds CPB’s plan to increase its marketing spend (and likely promotion) as it accelerates the launch of eight new soups in the next two quarters (Fiscal Q2 and Q3). The drivers under the hood suggest further top-line pressure on increasingly more difficult comps and continued gross margin and operating margin pressure over the next two quarters. We also don’t think the company has not hit the mark on soups, launching hearty and healthier higher premium soups that look to be missing on the consumer’s value perception given the still very strapped labor market and macro environment.

In short, CEO Denise Morrison continues to under-deliver on her promise to turn around an ailing portfolio; US Simple Meals and US Beverages were clearly significant laggards in the quarter. Fiscal Q1 revenues of $2.17B fell -7.3% in the quarter (underwhelming consensus of $2.29B) and EPS declined -21% to $0.66 (vs consensus $0.86). Management attempted to explain away the decline citing unexpected light retailer inventory building and this year’s late Thanksgiving that will push more shipments into next quarter (Q2).

CPB is immediate term TRADE oversold and bearish on the intermediate term TREND. Therefore, this is a name we’re not comfortable owning over the intermediate term, and may only tactically trade around it to take advantage of price imbalances.

Given the weakness in the quarter, CPB lowered it FY 2014 guidance: sale 4% to 5% (prior 5% to 6%); EBIT 4% to 6% (prior 5% to 7%); and EPS 2% to 4% or $2.53 to $2.58 (prior $2.58-2.62).

Matthew Hedrick

Associate