“Difficulties are just things to overcome, after all.”

-Ernest Shackleton

Sir Ernest Shackleton was one of the principal figures of a period known as the Heroic Age of Antarctic Exploration. Initially, this period was most identified by Roald Amundsen reaching the South Pole in December 1911. Shackleton decided to try to one up Amundsen and launched an expedition to cross Antarctica from sea-to-sea over the pole.

In 1914, Shackleton began fundraising for this “Imperial Trans-Antarctic Expedition”, which was eventually launched in September 1914 despite the outbreak of World War I. Misfortune struck Shackleton and his crew early in the trip when their ship, the Endurance, was frozen into an ice flow in the Weddell Sea. The ship eventually had to be abandoned.

For the next almost 500 days, Shackleton and his men were stranded in Antarctica. They had no contact to the outside world and routinely faced temperatures that dipped below -50 degrees Celsius. Eventually after an almost impossible trip to a nearby whaling station, the entire crew was rescued. While the expedition fell short of its goal, Shackleton and his colleagues certainly gained some polar perspective.

Back to the global macro grind...

Similarly, for many hedge fund managers this has been a year to gain perspective, if not outperformance. As an example, as of the end of October 2013 the Hennessee Hedge Fund Index was up 9.9%, which paled in comparison to the return of the SP500 of north of 23%. Now to be fair, returning close to 10% on 2 and 20 money isn’t the worst thing in the world, but undoubtedly for many underperforming a passive strategy by more than 1,000 basis points is frustrating.

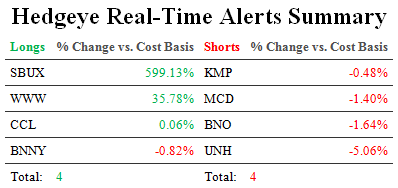

Keith touched on this yesterday, but a key reason for the underperformance of hedge funds is the outperformance of heavily shorted stocks. Specifically, heavily shorted stocks are outperforming the SP500 by some 570 basis points this year. That’s enough to make any great short seller bi-polar!

Long / short equity managers likely aren’t the only investment managers going a little bi-polar this year. As an example, the PIMCO Total Return Fund has returned a capital eroding -0.87% in the year-to-date. Clearly, the big bond boys at PIMCO are having some performance issues (not to say that it would at all be easy to steward that much capital!).

The broader issue with bond managers of course is how far afield they eventually have to search for yield. Just like Shackleton and his crew in Antarctica, who eventually found land, the question for bond managers is ultimately: what is the cost of this search for yield?

As it relates to the PIMCO Total Return Fund, prospective underperformance may even be more concerning given the fund’s holdings and where the managers have gone to find yield. According to analysis by our Financials Team, almost 34% of PIMCO Total Returns holdings are in agency mortgage backed securities. In the Chart of the Day, we highlight the spread of agency MBS to the 10-year Treasury Yield. As the chart highlights, prior to the financial crisis this spread was ~126 basis points, but has now narrowed to ~68 basis points.

The almighty chase for yield has effectively priced mortgage backed securities to one of the lowest levels of risk that we’ve seen in the asset class. Even if the spread for Agency MBS just normalized by 50 basis points to pre-crisis levels, it would have a meaningful impact on the market. By our estimation, allowing for modified duration, a 50 basis increase (reversal of tapering for instance) in yield would lead to 5% downside in the Agency MBS market.

The issue for firms like PIMCO is that a 5% correction in one of its more significant asset class exposures is likely to lead to continued underperformance and accelerated outflows. Outflows and decreased liquidity, of course, are only likely to exacerbate any move in price in the MBS market.

The Financial Times this morning emphasized this point even further in an article looking at managers of collateralized loan obligations. According to the article, managers of CLOs have increased the proportion of risky loans that their investment vehicles are allowed to buy to the highest level on record. Currently, 55% of new leveraged loans come in the covenant lite form, which eclipses the 29% reached shortly before the financial crisis.

Covenant lite loans are fine, in theory, if the economy is stable, but if there is volatility in economic activity, these loans get much more difficult to repay for many corporates. A good analogy is probably Shackleton and his crew in -50 degrees Celsius weather in Antarctica. You know weather that cold is dangerous but it is survivable, until the wind starts to blow and wind chill sets in . . .

To dig further into the topics of asset allocation, our Financials Team will be hosting a call his Thursday November 21st at 11am with Carl Hess who is the global head of Towers Watson’s investment advisory services that provides asset allocation recommendations to more than $2 trillion in assets under advisement. We think this call will provide an interesting perspective on asset allocation and active management, and if you’d like details on how to get access to the call, please email .

Given the challenges faced by large asset allocation funds that rely heavily on yield for performance, going forward it might be prudent that managers of these funds search for analysts for their investment teams with a similar advertisement to what Shackleton used to find his crew:

“Men wanted for hazardous journey. Small wages. Bitter cold. Long months of complete darkness. Constant danger. Safe return doubtful. Honour and recognition in case of success.”

Indeed.

Keep your head up and stick on the polar ice,

Daryl G. Jones

Director of Research