Below is the detailed breakdown of this morning's claims data from the Hedgeye Financials team. If you would like to setup a call with Josh or Jonathan or trial their research, please contact

More Good News on the Labor Front

This week's data shows a continuation and modest acceleration in the rate of improvement in the labor market. As is our convention we largely disregard the seasonally adjusted data and instead look at the year-over-year rate of change in the non-seasonally adjusted data.

This week is a bit difficult on that front because we are lapping the impact of Hurricane Sandy. This week last year we saw a 78,000 W/W increase in claims from Sandy. If we adjust the numbers for Sandy we find that the Y/Y rate of improvement this week came in at -8.9%, i.e. claims are lower than last year by 8.9%. This is a modest acceleration in trend from the previous week's -8.4%. On a rolling basis the dynamic is similar, where the rate of improvement strengthened to -8.1% from -5.1%, but we are also coming off the distortion of the California IT hiccup.

The net of it is that the labor market continues to gain momentum and this should, on the margin, push up tapering expectations and push up the long end of the yield curve. Beneficiaries include asset sensitive and credit sensitive financials.

Nuts & Bolts

Prior to revision, initial jobless claims rose 3k to 339k from 336k WoW, as the prior week's number was revised up by 5k to 341k.

The headline (unrevised) number shows claims were lower by 2k WoW. Meanwhile, the 4-week rolling average of seasonally-adjusted claims fell -4.75k WoW to 343.75k.

The 4-week rolling average of NSA claims, which we consider a more accurate representation of the underlying labor market trend, was -13.2% lower YoY, which is a sequential improvement versus the previous week's YoY change of -5.9%. This is unadjusted for the Sandy distortion we profile above.

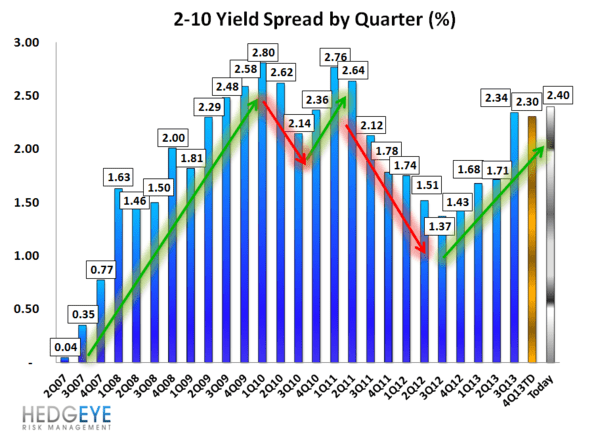

Yield Spreads

The 2-10 spread rose 5 basis points WoW to 240 bps. 4Q13TD, the 2-10 spread is averaging 230 bps, which is lower by 4 bps relative to 3Q13.

Joshua Steiner, CFA

Jonathan Casteleyn, CFA, CMT