The Initial Jobless claims data is taking a backseat this week to the advance estimate of domestic, 3Q13 GDP (3Q13 GDP: Juiced By Inventories) and the surprise ECB policy decision - ECB Cuts, EURO Plunges! – which is serving as the lead driver of risk assets globally today.

However, this week’s claims data provides important confirmation that the deterioration in the labor market observed over the last few weeks was largely optical and should reverse over the coming weeks as we revert back towards trend-line improvement.

Below is the detailed breakdown of this morning's claims data from the Hedgeye Financials team. If you would like to setup a call with Josh or Jonathan or trial their research, please contact

- Hedgeye Macro

--------------------------------------------------------------------------------

The Jury is Back and Has Reached a Verdict (on the labor market)

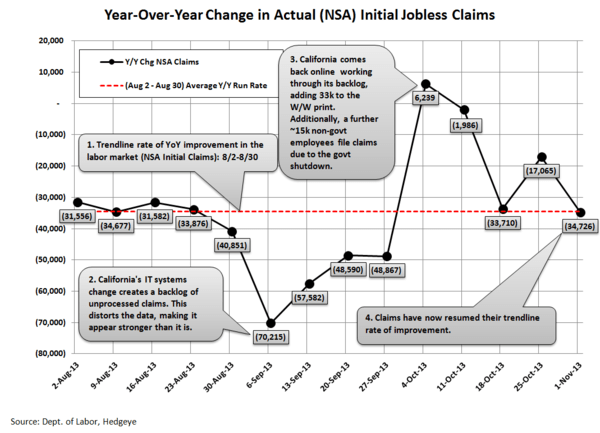

Last week we lamented the inability to conclude whether a negative inflection in the labor market was occurring based on lagged CA state level data. This week can speak more definitively. The labor market remains strong. The chart below shows the Y/Y trend in NSA initial claims nationally. The red line highlights the trend rate of improvement prior to CA's IT-related fiasco. The data has now resumed that pre-CA trend rate of improvement.

We won't belabor the point other than to say that the labor market appears not to have skipped a step as we had potentially feared. One thing we will call out, however, is that consumer confidence/comfort has fallen to a new YTD low. We include a chart later in this note illustrating that. The chart shows the 4-week rolling average of the weekly Bloomberg consumer comfort survey, but the weekly data is no less reassuring. It's unusual to see a divergence between the labor market and the consumer comfort survey data. We'll take a closer look and report back with any worthwhile findings next week.

Nuts & Bolts

Prior to revision, initial jobless claims fell 4k to 336k from 340k WoW, as the prior week's number was revised up by 5k to 345k.

The headline (unrevised) number shows claims were lower by 9k WoW. Meanwhile, the 4-week rolling average of seasonally-adjusted claims fell -9.25k WoW to 347.25k.

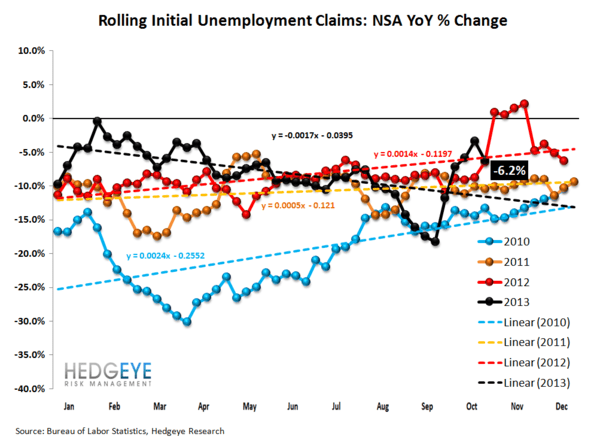

The 4-week rolling average of NSA claims, which we consider a more accurate representation of the underlying labor market trend, was -6.2% lower YoY, which is a sequential improvement versus the previous week's YoY change of -3.4%

Joshua Steiner, CFA

Jonathan Casteleyn, CFA, CMT