This note was originally published at 8am on October 16, 2013 for Hedgeye subscribers.

“You know that the Englishman’s idea of a compromise is? He says, some people say there is a god. Some people say there is no god. The truth probably lies somewhere between these two statements.”

-William Butler Yeats

I would hardly call myself a classical music aficionado, but I do enjoy tuning Spotify into classical music while grinding away in the office. One of my recent favorites, “Fanfare for the Common Man”, was written by American composer Aaron Copland for the Cincinnati Symphony Orchestra in 1942. (Incidentally, the Chicago Blackhawks use this as a pre-game song as they enter the ice.)

Copland’s idea for the fanfare came from a speech by then Vice President of the United States, Henry Wallace. He gave this speech at a time when Americans were debating wartime strategy and America’s role in the post-World War II order. One of Wallace’s key points in the speech was that any post war peace should be such that it makes the common man better off for the long run.

This morning it seems our two great political parties, and their esteemed leadership, are coming together on a compromise to benefit the common man. According to reports this morning from our contacts in Washington, the Senate deal that is on the table is to extend U.S. borrowing authority through February 7th and fund the government through January 15th 2014.

Thank goodness that these folks are looking out for the common man by cobbling together a deal that my 11 year old niece could have negotiated. Despite the short term and non-materiality of this proposed agreement, it still has two hurdles – a) Ted Cruz, or another Senator, could filibuster and delay passage until next week and b) Speaker Boehner in the House could opt not to send the bill to the floor for an up / down vote.

There is one data point out this morning that gives me great confidence that the debt ceiling will be resolved orderly. No, it’s not that credit default swaps are trading lower, that Libor is benign, or that gold has been selling off, but rather that the ultimate contrarian indicator, a ratings agency, Fitch specifically, placed the U.S. credit ratings on negative watch yesterday.

Back to the global macro grind . . .

A major call-out this morning is the Shanghai Composite which is down almost -2%. This weakness is being driven by the property sector which is under pressure based on local news reports that longer term regulations could be in place soon for controlling property in China.

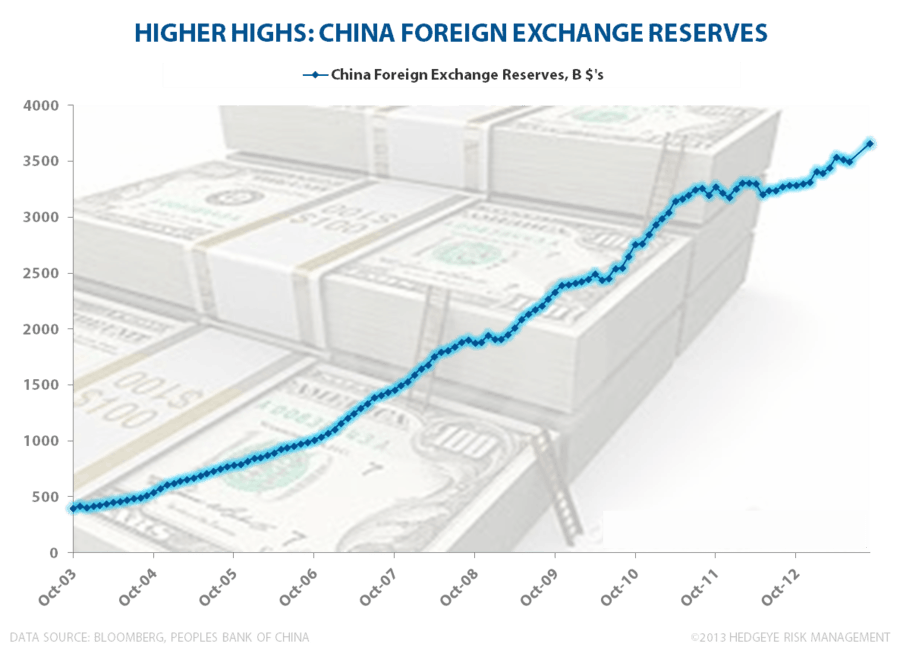

Being the price and market driven analysts we are, the move in Chinese equities this morning is certainly a red flag in our notebooks, but isn’t changing our more positive view on China. In the Chart of the Day today, we highlight China Foreign Exchange Reserves, which have continued to build even as money has left other emerging markets in recent quarters.

Admittedly, though, China is hard to ignore as it compromises more than 30% of the world’s foreign currency reserves. Japan is a not so close second at about 10%. After that we have Saudi Arabia, Switzerland and Russia rounding out the top 5.

From the currency war perspective, there is certainly a bit of People’s Bank of China manipulation going on as exports were admittedly a little soft in September and the Chinese Yuan is eclipsing twenty year highs. Of course no rational person could blame the PBOC for playing games with their reserves as the U.S. central bank continues to confuse the market with its intentions. To taper, or not to taper, that is the question?

Sadly, if we can actually get the debt ceiling and government shutdown resolved in the next day or so, then all eyes will once again be fixated on the Fed. We’d be remiss this morning if we didn’t at least highlight how ineffective the program of quantitative easing has been. Hat tip to David Einhorn from Greenlight Capital for flagging this in his recent investor letter:

“In August, the San Francisco Fed published an economic research paper that estimated that the $600 billion spent on QE2 added a meager 0.13% to real GDP growth in late 2010 (about $20 billion) and that the benefit fades after two years. Given that, what practical difference does it make whether the Fed buys a monthly $85 billion or $75 billion or no additional securities at all for that matter?”

Buying any good, even say jelly doughnuts, as Einhorn highlights, has a more direct impact on economic activity than QE. After all, that is actually how the real economy works. We buy and sell goods and the velocity of money grows the economy naturally.

Interestingly, based on the math above, the Fed could actually be the worst investor in history. Just imagine a $600 billion capital allocation that generates a 0.13% return! Even there my 11 year old niece could do much better.

Our immediate-term Risk Ranges are now:

UST 10yr yield 2.66-2.73%

SPX 1685-1725

VIX 15.21-17.63

USD 80.11-80.67

Brent 110.01-112.05

Gold 1265-1303

Keep your head up and stick on the ice,

Daryl G. Jones

Director of Research