This note was originally published at 8am on October 11, 2013 for Hedgeye subscribers.

“Boom, crush. Night, losers. Winning, duh.”

-Charlie Sheen

Yesterday was one of those days that people absolutely loved or hated. Watching my Twitter #ContraStream was quite comical actually. Some of the “intellectual” types just couldn’t believe what was happening. Some of the bros were tweet-panting.

I think most of you know that I’m not the smartest player in this game. I think that helps me. I think less when I change my mind and/or position. That’s by design. After making almost every mistake you can make in this game with live ammo (multiple times), I’ve built in blinders (machines) for my emotions. They stop me from over-thinking.

To each their own. Like you, I have my style biases. One of the big ones is approaching this game of globally interconnected-risk from an athlete’s perspective. I know we can’t win unless I grind alongside my teammates. I also know we’ll lose if we don’t respect Mr. Market’s signals.

Back to the Global Macro Grind…

VIX snaps @Hedgeye TREND support of 18.98; SP500 rips through 1663 @Hedgeye TREND resistance. “#Boom, Crush!” The Signal within the manic media’s noise made it so simple that even a hockey player could do it.

And what did we learn?

- Respect the setup (the signal was screaming into event risk that government could save us from themselves)

- Stay with the confirmation (the signal said stay with the early part of the move; don’t sell)

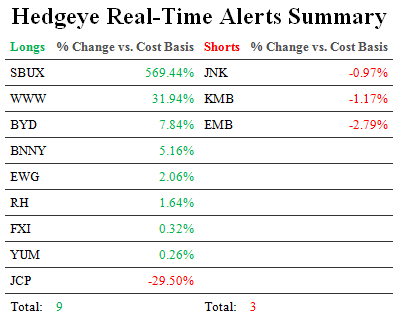

- Let it ride (9 LONGS, 3 SHORTS @Hedgeye – with 2 of the 3 SHORTS being bond shorts)

Do you know how many times in the last 15 years that I have violated not one, but all 3, parts of that risk management process? I don’t. And that’s primarily because 5 and 10 years ago, I didn’t have this dynamic signaling model. It evolves.

What you’ll quickly note in steps 1-3 of the decision making tree is that there are no points for intellectual IQ. Mr. Market doesn’t care how smart you are. He couldn’t care less what your position is either. The only thing that matters is how well you listen to him.

For me at least, just getting to step 1 was tough – and that’s primarily because I think the Fed leaning on the long-end of the curve, suppressing rates, and devaluing the Dollar, is a textbook #GrowthSlowing signal. But that fundamental signal should never be confused with a quantitative risk management signal. In the immediate-term they can be 2 very different things.

Once I accepted the VIX/SPY signal for what it was, what did I do next?

- Stayed with the confirmation – that means I got longer on green (covered a short, bought a long)

- Then I let it ride throughout the day despite every bone in my body telling me to sell

What do my bones have to do with it? Listen to them and prepare to be crushed. “Night, losers.” Letting a winning move ride is easily the hardest thing for me to do. Why? Because I love booking gains. And for that very reason, I tend to book them too early.

So, I need to be better than that and let the signal tell me when/where it’s the right time to sell. I’m nowhere near as bad as I used to be on this front. But I have a lot of room to improve.

Let’s use SP500 levels as an example of why I’d let that ride yesterday and drop our Cash position to 42% (we started the week net short in #RealTimeAlerts and had a 55% Cash position in the Hedgeye Asset Allocation model):

- SP500 intermediate-term TREND resistance became support at 1663; that’s a big line

- SP500 immediate-term TRADE breakout line = 1681; layered on top of the TREND, that’s even bigger

- SP500 immediate-term TRADE resistance = 1708; that’s up another +0.9% from the 1692 close

All the while, I’m considering the emotion and intensity of the move (this is where the Twitter #Contra-Stream I built is priceless) within the context of the prior 2013 US stock market “corrections.”

As you can see from Darius Dale’s Chart of The Day, each of the last 3 corrections has:

A) been to higher-lows

B) been less of a % move than the prior correction

C) been on less volume than the prior correction

Markets that people hate are the best ones to be long; particularly when corrections are confirmed by weak volume and lower-high volatility signals. Again, to contextualize this recent SP500 correction:

- SEP 18 to OCT 8 correction = -4.1%

- AUG 2 to AUG 27 correction = -4.6%

- MAY 21 to JUN 24 correction = -5.8%

And I get it. For the last 3 weeks I wrote to you every day that I wasn’t buying this correction like I did the AUG and JUN corrections. But I also get when and why I changed my mind. There are no rules against doing that. “Winning, duh!”

My Macro Team and I will be hosting our Q413 Global Macro Themes Conference Call at 11AM EST. Ping Sales@Hedgeye.com if you’d like to have access to our most recent research and risk management thoughts.

Our immediate-term Risk Ranges are now:

UST 10yr 2.65-2.71%

SPX 1682-1708

DAX 8601-8729

VIX 15.18-18.98

USD 80.20-80.74

Gold 1271-1311

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer