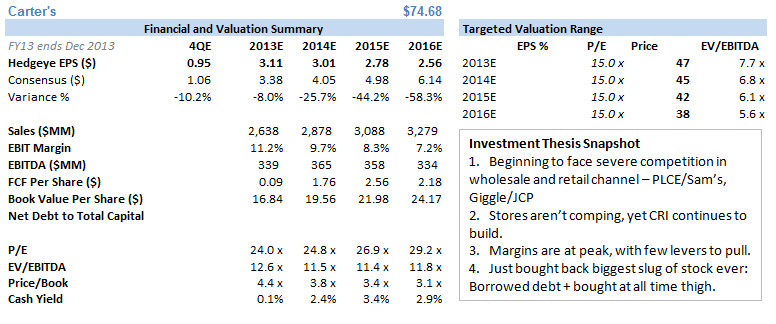

We didn't like this CRI quarter one bit. In fact, with the exception of good growth in e-commerce, there wasn't a single thing we liked. To be clear, we were negative on this name last year, and though we were mostly right on the model, we couldn’t have been more wrong on the stock. Though we continued to have a serious bias against the sustainability of the business model, we kept our discipline and (painfully) threw in the towel on our short. Congratulations to all of you that rode this horse from $50 to $75 over the past year. Lesson learned for HedgeyeRetail.

All of that said, there's no shortage of reasons for selling your position today. Consider the following…

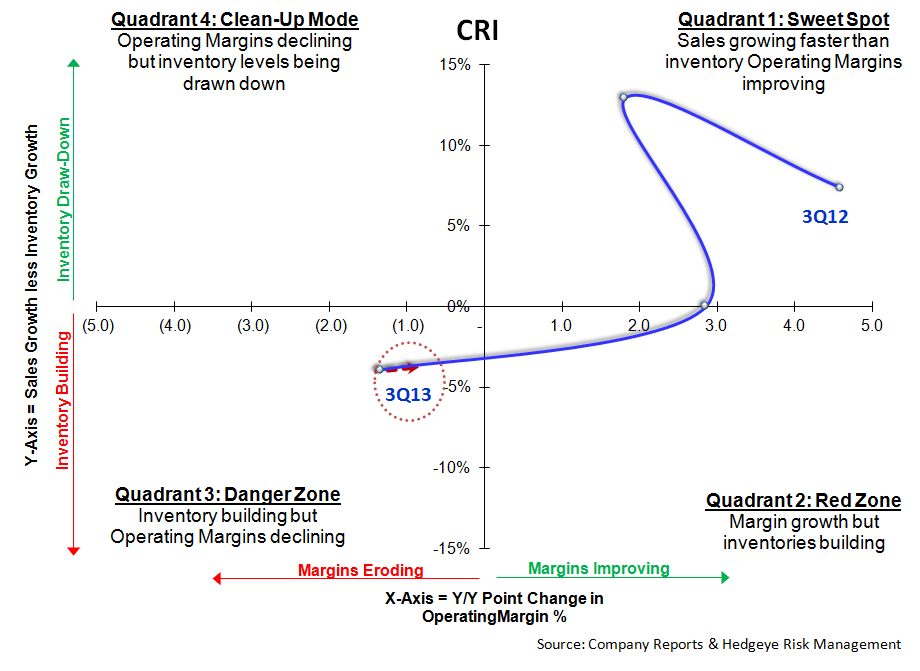

1. Here's the elephant in the room: CRI borrowed an extra $400mm in debt to repo $454mm stock (thus far). We ordinarily would give a company credit for such a buyback, but to execute on such a big program when Margins are at peak, your stores are comping down, inventory is building, and your stock is at an all-time high??? We're sure it went through an exhaustive corporate governance process, but quite frankly, we're surprised that any board let it get past the goalie.

2. At face value, the growth algorithm looks good -- until you get to SG&A. On a GAAP basis, earnings were down for the second quarter in a row. We know no one cares about GAAP anymore, but hey, it's the REAL earnings of the company. Even excluding all special charges, earnings only grewby 9.5% -- well below the rate of revenue.

3. Wholesale Carters was the star. Kinda.

4. Carter's Retail put up slammin' revenue numbers as well -- up 16% in aggregate, but 8.9% when we exclude e-commerce. The comp was up only 0.5%. But get this…they're on track to open 66 new stores for the year. Can someone explain to me why a company is growing 14.5% square footage while its stores are not comping. This is a little reminiscent of Coach (but not as pathetic).

5. As good as a 15% retail top line number is, it's hard to get excited about it when EBIT grows 500bp slower.

6. Dot com looked really good for CRI, but keep in mind that its still only 7% of brand sales. Other premium brands are 2x that rate. The good news for CRI is that the new DC in Atlanta will help keep this growth rate in gear.

7. In wholesale Carters, the Brand printed 6.4% EBIT growth on a whopping 15.6% top line performance. Clearly it did not play the promotional game wisely this quarter. The company noted an ad shift into the quarter, as well as some air freight expense. If we assume that all of this a) actually happened, and b) was about $7mm, then margins were about flat versus last year.

8. Osh Kosh Wholesale: Down double digits for the fourth quarter in a row, with operating profit clocking in at a whopping $2mm. In fact, if you add up all the EBIT generated by Osh Kosh Wholesale over the past five ears, you come up with an embarrassingly low number -- $15mm. It's not getting better.

9. Retail Osh Kosh put a better foot forward by NOT shrinking its revenue base for the first time in 8 quarters. That said, it was entirely due to e-commerce, as the base stores comped down by 4.3%.

10. Here's a comment we don't get...

Management: "We continue to see strong demand for our brands in international markets. Our growth in the quarter was largely driven by our business in Canada. The decline in earnings reflects the start-up costs in Japan."

Hedgeye: Why don't we get it! Comps were -3.6% in Canada, -6.4% for Bonnie Togs, and -1.3% in the co-branded stores (the latter is billed as CRI's saving grace in Canada).