Hershey’s reported another strong quarter, furthering our bullish outlook on the stock since last quarter, through solid core brand performance with momentum building going into the holiday season. While net sales were driven squarely by volume (Volume +6.1%; Net Price +0.5%; FX -0.5%) and today’s -2% move in the stock may reflect concerns about its decision to invest $250MM in cap-ex to build a new plant in Malaysia (to supply markets in Asia and assist existing capacity in China), we think these concerns are overblown and would be buyers on any weakness as we look out to year-end.

Heading into year-end, the company reiterated its expectations for FY 2013 net sales of 7%, with no change to the input cost outlook, revised up its FY Gross Margins expectations to 240 to 250 bps vs a previous estimate of 220 to 230, and said it sees a more favorable tax rate and earlier Chinese New Year offsetting an increased marketing spend in Q4. We’re bullish on HSY’s performance across retail channels and its determination to grow it international business, in particular China to its second largest business, and believe the additional cap-ex spend will allow it to enhance its manufacturing scale in China (currently it has a manufacturing JV facility) and across Asia.

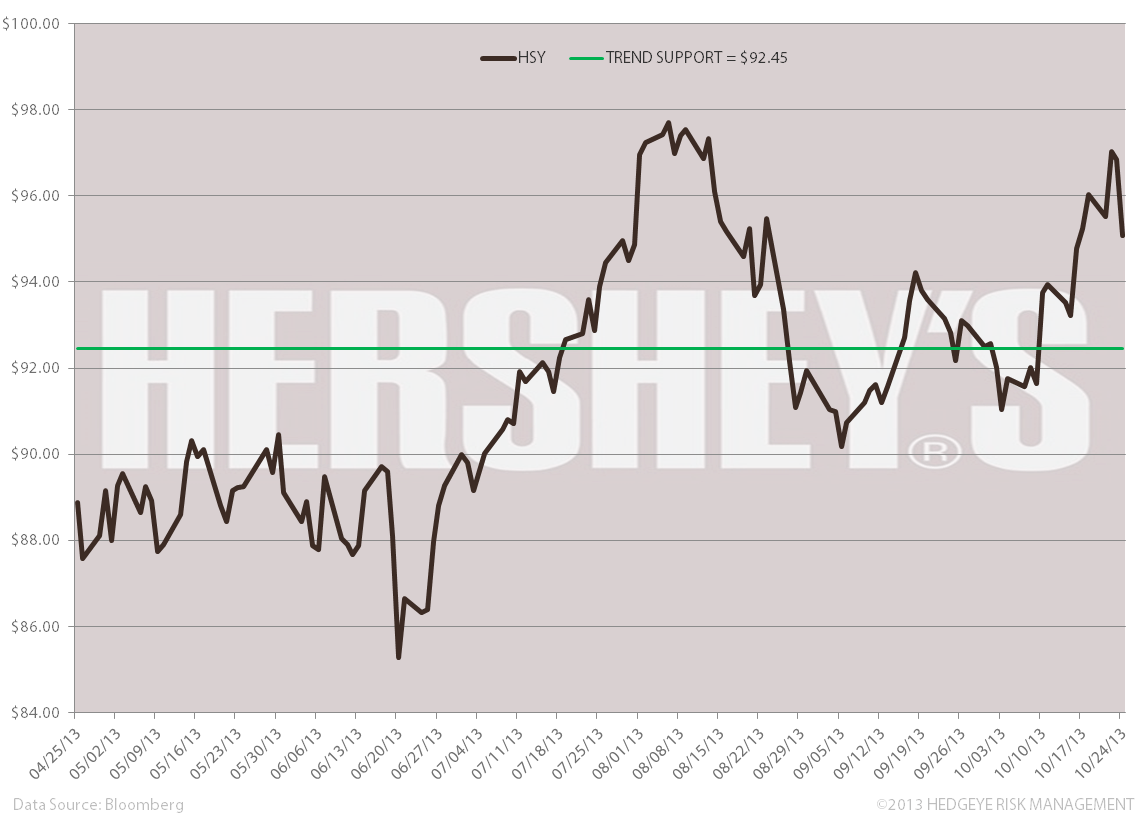

From a quantitative set-up HSY is comfortably trading above its intermediate term TREND level, confirming our bullish outlook:

What we liked:

- Net Sales increased 6.1% (Volume +6.1%; Net Price +0.5%; FX -0.5%)

- EPS of $1.04 (beat consensus of $1.01), an increase of 19.5% vs the prior-year quarter

- Candy, Mint, Gum (CMG), which equals 90% of U.S. retail business, expanded in all retail channels, up +5% Y/Y, with market share gains of 0.7 points in the quarter

- Q3 Adjusted Gross Margin increased +300bps on lower commodity costs, supply chain productivity, and cost savings initiatives

- Input cost deflation of $33MM in the quarter (in line with estimates); no change to cost outlook for the year.

- Expect a meaningful boost in advertising in Q4 due in part to a lighter spend in Q3 (increased 12% vs target of 20% due to timing); FY target expected to increase 22-23%

- Strong performance from Brookside. Expected to contribute 1.2% to 1.3% of sales growth in 2013

- Q4 will benefit from earlier Chinese new year

- International net sales up 14%, led by China, Mexico, and Brazil

- Expect 2013 net sales of 7% of sales and FY Gross Margins up 240 to 250 bps (vs previous estimate of 220 to 230)

- 2014 Guidance: 5-7% net sales growth, and 9-11% growth in adjusted EPS

Matthew Hedrick

Associate