DPS cited on its earning call an operating environment that continues to be “extremely challenging” with “significant pressures in the CSD (carbonated soft drink) category now impacting both regular and diet products”. While the company beat EPS estimates ($0.88 vs Consensus $0.83), it missed top line consensus ($1.54B vs $1.56B) on a mere +1% gain over the previous-year quarter. Total volume was down -1% versus the year-ago quarter.

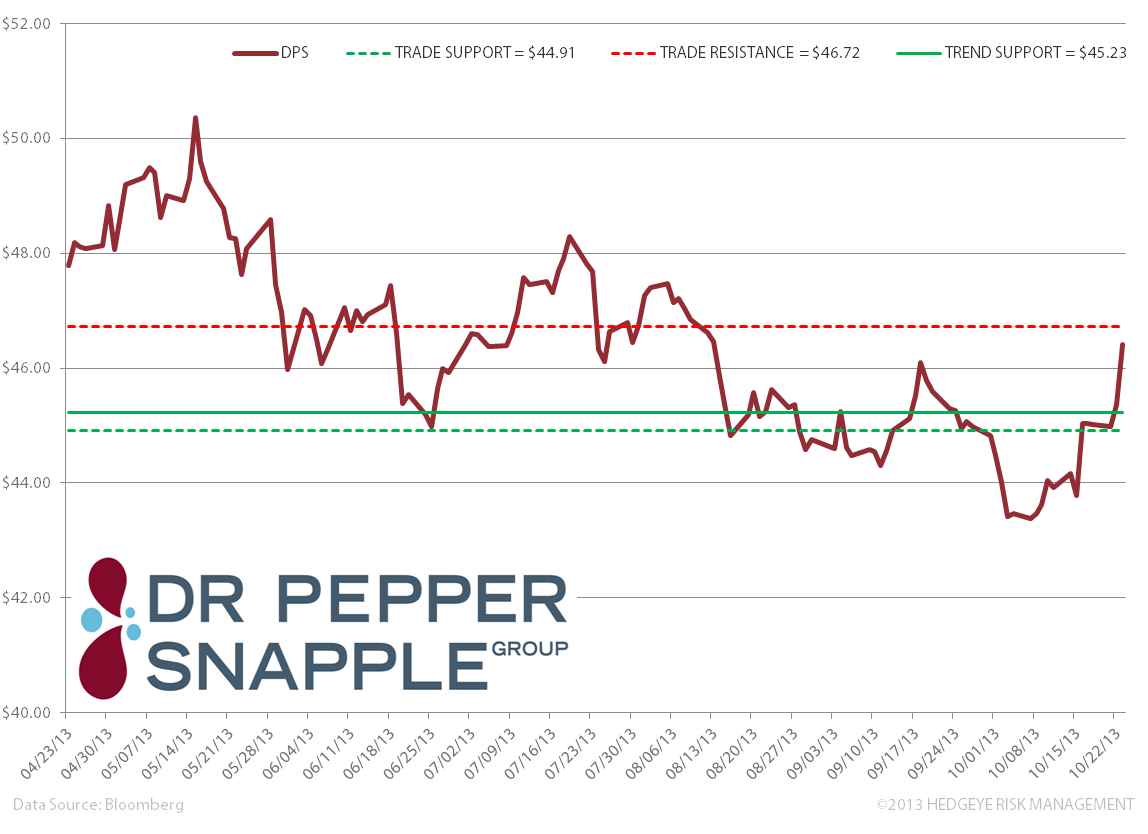

Despite today’s squeeze in the stock, we remain bearish on DPS over the intermediate term.

From a quantitative perspective, we could see the stock pull back to its TRADE level (-3.2% from its current price) over the immediate term (3 days or less).

Our primary concern is not a new one and remains grounded in the fact that DPS’s portfolio is ~ 80% CSDs, a category that has drawn less demand in recent quarters (~ 3% annual industry volume decline) given health and wellness trends as consumer switch to both healthier carbonated and non-carbonated offerings versus traditional carbonated soda.

DPS’s answer to this trend is DP 10, its newest soda offering that should have full distribution by the end of the summer. DPS says that the 10 calorie drink with a full taste profile (note: the lack of a full taste profile is often the complaint of diet drinkers) stands to address the health and wellness market. That said, the diet category across the industry is seeing declines, and our bet is that DP 10 is more likely to cannibalize its Diet DP product rather than turn around its portfolio.

Outside of CSDs, DPS saw some offsets in NCBs, including a +4% volume increase from Snapple, yet Hawaiian Punch declined -6% and Mott’s saw a mere 1% gain. Geographically, volumes were down -1% in the U.S. and Canada, partially offset by +6% increase in Mexico and the Caribbean.

To quote CEO Larry Young: “This team never gives up on CSDs”. We, however, have no mandate to be invested in CSDs, nor the beverage category for that matter. To say the least, we’re not convinced on this turn-around story based on DP 10 and will opportunistically short the stock or stay on the sidelines until further notice.

Matthew Hedrick

Senior Analyst