TODAY’S S&P 500 SET-UP – October 10, 2013

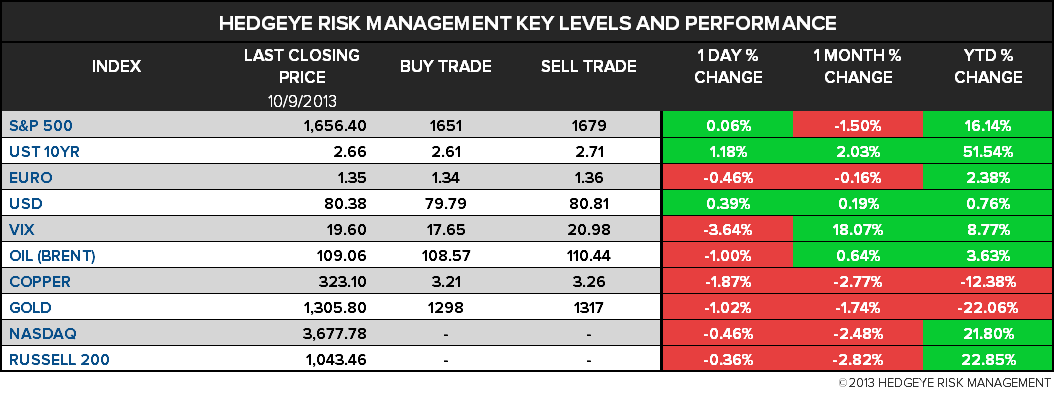

As we look at today's setup for the S&P 500, the range is 28 points or 0.33% downside to 1651 and 1.36% upside to 1679.

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 2.35 from 2.31

- VIX closed at 19.6 1 day percent change of -3.64%

MACRO DATA POINTS (Bloomberg Estimates):

- 7am: Bank of England seen maintaining 0.50% bank rate

- 7:45am: BoJ’s Kuroda speaks at Council on Foreign Relations

- 8:30am: Initial Jobless Claims, Oct. 5, est. 310k (prior 308k)

- 9:45am: Bloomberg Consumer Comfort, Oct. 6 (prior -29.4)

- 9:45am: Fed’s Bullard speaks on monetary policy in St. Louis

- 10am: Freddie Mac mortgage rates

- 10:30am: EIA natural-gas storage change

- 11am: Fed to purchase $1b-$1.5b TIPS in 2018-2043 sector

- 12:20pm: ECB’s Draghi speaks in New York

- 1pm: U.S. to sell $13b 30Y bonds in re-opening

- 1:45pm: Fed’s Tarullo speaks on regulatory reform in D.C.

- 2:30pm: Fed’s Williams speaks on economy in Boise, Idaho

GOVERNMENT:

- Sec. of State John Kerry in Bandar Seri Begawan, Brunei, for U.S.-ASEAN Summit and East Asia Summit; leaves for Malaysia to meet officials, attend Global Entrepreneurship Summit

- 8am: Treasury Sec. Jack Lew testifies at Senate Finance Committee on debt limit

- 8:45am: World Bank President Jim Yong Kim holds press briefing

- 9:30am: IMF M.D. Christine Lagarde speaks to press

- 10am: Senate Banking, Housing and Urban Affairs Committee holds hearing on consequences of default on financial stability, economic growth, with American Bankers Association CEO Frank Keating, Sifma present Kenneth Bentsen Jr.

- 1pm: House Natural Resources panel holds hearing on EPA and mining jobs

WHAT TO WATCH:

- Sept. U.S. same-store sales seen slowing from Aug.

- Debt-limit prospects gain as both sides open to short-term deal

- Hong Kong raises haircut on U.S. bills for margin cover

- Samsung set for $1.4b windfall after Seagate stock sale

- Microsoft’s board said to work on hiring new CEO this year

- Jarden’s Franklin close to buying MacDermid to add chemicals

- Blackstone receives first-round bids for La Quinta: WSJ

- KKR to pay $1b for industrial-products makers Crosby, Acco

- Manhattan apartment rents fall for the first time in 2 years

- ECB agrees to bilateral currency swap agreement with PBOC

- Telecom Italia is said to value Brazil stake at $12b

- Libyan PM seized from hotel by revolutionary group in Tripoli

EARNINGS:

- Angiodynamics (ANGO) 4:01pm, $0.03

- Bank of the Ozarks (OZRK) 6pm, $0.60

- Blackhawk Network (HAWK) 9am, $0.05

- E2Open (EOPN) 4:05pm, $(0.15)

- iGATE (IGTE) 6:45am, $0.43

- Lindsay (LNN) 7am, $0.91

- Marriott Vacations Worldwide (VAC) 8am, $0.39

- Micron Technology (MU) 4:04pm, $0.23 - Preview

- Safeway (SWY) Aft-mkt, $0.16 – Preview

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Brent Crude Rises as Libya Prime Minister Freed From Detention

- Soybean Reserves Reach Record as Goldman Sees Slump: Commodities

- Cocoa Reaches 21-Month High on Demand Indications; Robusta Rises

- Copper Rises on Speculation U.S. Will Avoid Defaulting on Debt

- Gold Falls as Investors Weigh Prospects for Debt Deal, Tapering

- Tin Membership Increases at ICDX as Indonesia Targets Benchmark

- Gold Seen Lower by Morgan Stanley in 2014 as Goldman Says Sell

- Soybeans Climb on Supply Outlook Before South American Harvests

- Japan Buys Least Milling Wheat in 3 Months in Regular Tender

- Refiner Gains in Asia to Rebound as Units Shut: Energy Markets

- Cold European Winter Could Create Energy Crisis, Cap Gemini Says

- Costlier CO2 Permits Boost Long-Term EU Gas Demand: Bull Case

- Apple to Toyota Seen Gaining From Thailand’s Upgrade: Freight

- Rebar Rises on Bets Chinese Economic Growth to Support Demand

CURRENCIES

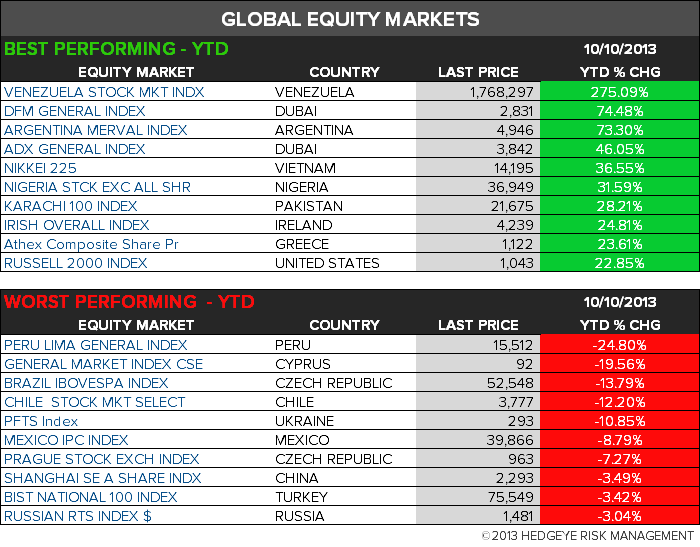

GLOBAL PERFORMANCE

EUROPEAN MARKETS

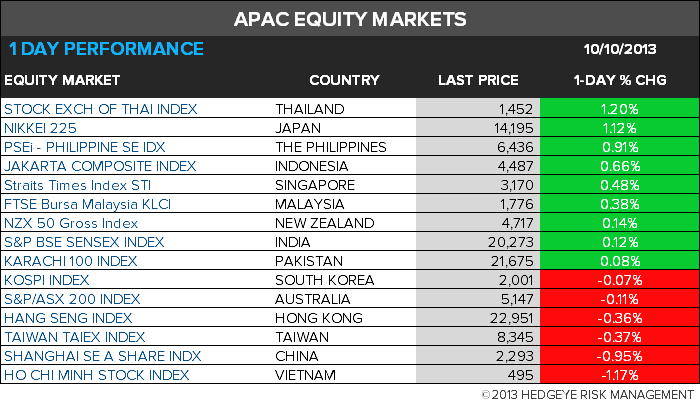

ASIAN MARKETS

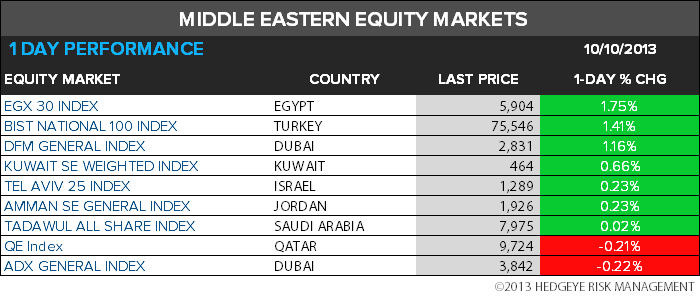

MIDDLE EAST

The Hedgeye Macro Team