This note was originally published at 8am on September 18, 2013 for Hedgeye subscribers.

“If you want to get open under the basket, don’t just run towards the hoop – run to the free throw line first, then cut to the baseline to get open. Get High to Get Low. “

-Coach Ken Smith, Windsor CT basketball

Standing on stage in a Speedo with a freshly shaven body while a bunch of guys cheer for you elicits kind of an odd feeling.

The whole competitive bodybuilding scene is a singularly peculiar, multifarious mix of culture and personality and I do miss parts of it…kinda.

For the un-indoctrinated, the canonical approach to (natural) bodybuilding contest preparation, from the nutritional side, goes something like this:

In the 3 months leading up to contest day, you progressively tighten up the diet by concomitantly lowering total consumption and shifting your macronutrient profile increasingly towards protein and polyunsaturated fats (think olive oil, fish oil, mixed nuts, etc).

At some point, as caloric intake declines, you initiate or increase caffeine consumption for its beneficial thermogenic and appetite suppression effects. Nearer the end, if you need to further accelerate progress (and it’s the mid-2000’s when it was still legal) you may add in some measured amount of additional stimulant (via ephedrine) to help augment fat loss.

In general, the diet-stimulant combo works exceptionally well - for a while. Continue the regiment too long and the impact starts to diminish and ultimately reverse.

While there is some definite science underpinning the contest preparation process, there’s an undeniable element of art in manipulating all the diet and exercise dynamics so that your physique peaks exactly on contest day.

There is also the invariable, post-contest frustration. Inevitably, following the aesthetic ‘peak’ on contest day, the veins start to disappear, muscle definition fades, and you begin to smooth out as both diet and fluid balance renormalize to sustainable levels. After a week or two of physiological adjustment, you’re back to feeling (and looking) normal.

Does that over-consume à diet à stimulate à adjustment cycle look familiar?

Bodybuilding contest preparation is not dissimilar to monetary stimulus in the aftermath of a multi-decade credit binge. After the fun time (pizza eating/credit amplified consumption to offer both sides of the analogy) comes the diet/deleveraging and the stimulants/monetary stimulus to help things along - followed by the inevitable, but necessary, let down on the back end of the whole process.

Consensus continues to believe we’ll start the QE reversal adjustment process today with something on the order of a $5-10B reduction in monthly purchasing. Maybe it’s fully priced in, maybe not. Ultimately, measured policy normalization is a healthy and necessary adjustment and one we think justified given the positive breadth of the data YTD.

Back to the Global Macro Grind…..

There are three primary fiscal policy catalysts on the calendar in the near term:

- Oct 1st – Government Funding: the current Continuing Resolution, which provides funding for government operations in the (now all too familiar) event there is no official budget, ends on September 30th.

- Late October - Debt Ceiling: The latest statements from Treasury Secretary Lew, place the breach date between the end of October and mid-November.

- Year End - Sequestration/Fiscal 2014 Budget – Spending levels decline in accordance with sequestration if Congress fails to reach an agreement on an alternative.

Government funding, the Debt Ceiling, and the fiscal 2014 budget are three discrete events that have coalesced into a single, policy amorphism as each political side threatens standoff or promises compromise/concessions on one as a condition for an accord on another.

The majority of recent reports suggest the appetite of Republicans to present a united front in tying a delay in Obamacare implementation and other spending and tax initiatives to the Sept 30th government funding deadline is fading – which leaves the debt ceiling as the brinksmanship event of choice.

So, does the Debt Ceiling matter?

In large part, the debt ceiling matters as a political issue only in so much as the debt level exists as a partisan point of contention and a pervasive populous concern. For both the politico and the populous, the precedent appears to be that debt generally only matters when the slope is going the wrong way.

Consider the broader realities existent in 2011 vs. those prevailing today. The contrast is both illustrative and stark.

In 2011, when the Debt Ceiling clash roiled equities, we were still well north of $1T in deficit spending, the US credit rating hung in the balance, Europe was still on the brink, confidence remained near trough, QE was only midstream, and fixed income remained fully bid.

Presently, deficit spending is in retreat, the US credit rating isn’t a headline concern, confidence has inflected, Europe is stable-to-improving, policy is re-normalizing, and fund flows have begun a secular reversal.

Clearly, both the macro and sentiment dynamics have changed materially since Debt Ceiling 1.0. So has the trajectory of debt spending.

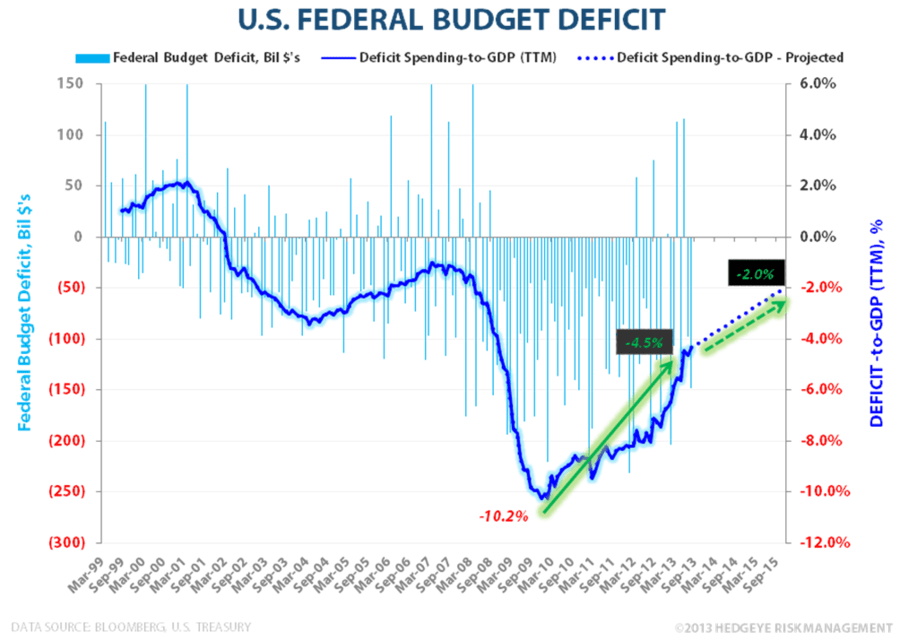

In the Chart of the Day below, we show the Trend in the deficit-to-GDP ratio. As can be seen, after reaching a peak of ~10% in 2009, the ratio has showed steady decline with accelerating improvement over the last year alongside stronger economic growth, higher taxes, a retreat in stabilizer payments, and a number of non-recurrent inflows.

We expect the ratio to retreat further as the domestic macro data continues to reflect ongoing, albeit modest, improvement.

Indeed, yesterday, in its latest update to the long-term budget outlook (Here), the CBO projected deficit spending would continue to drop over the next few years, falling to 2% of GDP by 2015 with the Debt-to-GDP ratio declining to 68% from its current level of ~73%.

Yes, the long-term budget outlook, saddled with unsustainable growth in entitlement obligations, remains dire. We’ll break down the budget outlook in detail, by duration, in subsequent notes, but the key takeaway here is that the outlook for both growth and debt spending over the intermediate term remains positive.

Markets and political strategy move on the slope of the line (better/worse, not good/bad) not on a highly uncertain, 12 year forward projection.

At present, the Trend slope of improvement in domestic growth, credit, confidence, and deficit spending are all positive and both Treasury Yields and the $USD (our key price signals as it relates to concern over the debt ceiling) remain Bullish from a price perspective.

#RatesRising has been reflecting that positive fundamental reality as have market prices as pro-growth exposure continues to get marked higher (new YTD high yesterday for the QQQ’s and another new all-time high for the R2K) while the underperformance spread for slow growth, yield chase assets (Utilities, MLP’s) continues to expand.

Notably, policy normalization and #RatesRising alongside Trend improvement in debt and deficit levels also holds important implications for future fiscal policy initiatives.

If we actually allow rates to go higher over the next couple of years – monetary policy can again be used as a tool to help offset employment and output drags stemming from fiscal policy decisions aimed at putting the budget on a sustainable long-term course.

If we stay at zero percent until projected debt/deficit ratios trough in 2015/16 we lose that optionality. To reiterate the basketball strategy quote from my AAU coach above: “Go High to Get Low”.

Perhaps the journey starts today.

Our immediate-term Macro Risk Ranges are now as follows:

UST 10yr Yield 2.82-2.99%

SPX 1680-1714

USD 80.79-81.73

Brent 107.58-111.43

NatGas 3.59-3.73

Gold 1288-1349

Christian B. Drake

Senior Analyst