TODAY’S S&P 500 SET-UP – October 2, 2013

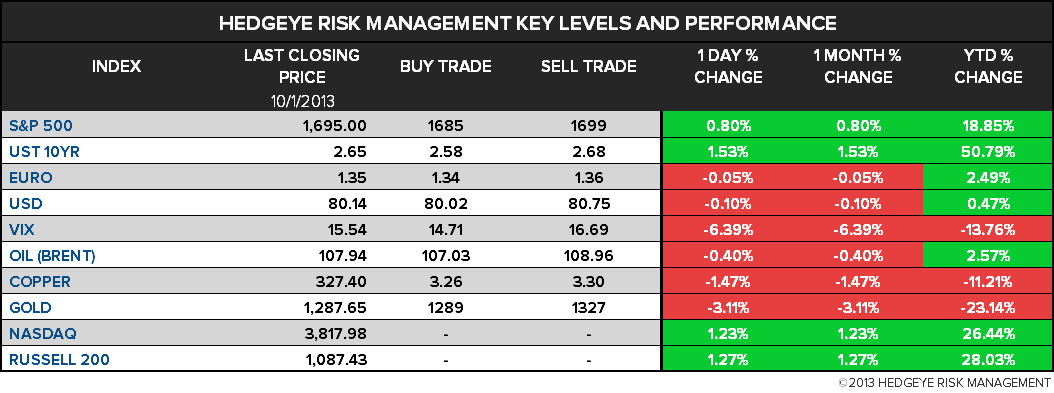

As we look at today's setup for the S&P 500, the range is 14 points or 0.59% downside to 1685 and 0.24% upside to 1699.

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 2.31 from 2.32

- VIX closed at 15.54 1 day percent change of -6.39%

MACRO DATA POINTS (Bloomberg Estimates):

- 7am: MBA Mortgage Applications, Sept. 27 (prior 5.5%)

- 7:45am: ECB seen holding benchmark interest rate at 0.50%

- 8:30am: ECB’s Draghi holds news conference on interest ra

- 8:15am: ADP Employment Change, Sept., est. 180k (prior 176k)

- 9:45am: ISM New York, Sept. (prior 60.5)

- 10:30am: DOE energy inventories

- 11:30am: U.S. to sell $20b cash management bills

- 12pm: Fed’s Rosengren speaks on economy in Burlington, Vt.

- 3:20pm: Fed’s Bullard speaks on community banks in St. Louis

- 3:30pm: Fed’s Bernanke speaks on comm. banks in St. Louis

GOVERNMENT:

- Second Day of federal govt shutdown, events may be canceled

- Obama meets with CEOs of large banks, incl. Goldman Sachs CEO Lloyd Blankfein, to discuss stalemate on budget

- House Armed Services Cmte hearing with Marine Corps logistics officials testifying on risks of sequestration, future force readiness, 2pm

- SEC Chairman Mary Jo White speaks at Security Trader Association’s 80th annual Market Structure Conference, 2:45pm

- House Transportation and Infrastructure Committee hears testimony on reauthorizing FEMA, 10am

WHAT TO WATCH:

- U.S. government shuttered with no quick end seen amid discord

- Overwhelming Obamacare demand signals potential success

- Shutdown seen merging with debt-limit fight

- Federal shutdown for a week seen shaving 0.1 point from growth

- CEOs say shutdown poses risk to U.S. economic rebound

- Microsoft board said to consider Mulally as Ford touts bench

- Wells Fargo said to face New York action over accord compliance

- ‘Candy Crush’ maker King said to file for U.S. public offering

- BP wasn’t prepared for Deepwater blowout, professor testifies

- Apple faces delay in producing new version of iPad Mini: Reuters

- HTC, Qualcomm redesigning phone chip after patent ruling: WSJ

- Cargill said to be close to buying ADM cocoa unit: Reuters

- Bank credit-card fees face new scrutiny by U.S. consumer bureau

- Tokyo Electron seeks deals after Applied Materials takeover

- Facebook offers mobile promotions aimed at boosting app usage

EARNINGS:

- CalAmp (CAMP) 4:01pm, $0.16

- Monsanto (MON) 8am, $(0.43) - Preview

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Iron Ore Forecasts Raised by Australia as Chinese Demand Surges

- Corn Reaches Three-Year Low as U.S. Production Outlook Improves

- WTI Drops Ninth Time in 10 Days as U.S. Crude Stockpiles Advance

- Gold Rebounds From 8-Week Low as Investors Weigh U.S. Shutdown

- Sugar Rises to 5-Month High After Brazil Output Cut; Cocoa Falls

- Copper Swings Between Gains and Drops Amid Shutdown in U.S.

- Sugar Trade Spurs Land Grabs in Developing Countries, Oxfam Says

- Yoshinoya to Grow Rice in Fukushima to Expand Farming Business

- Falklands Tax Dispute Clouding Oil Dream for Investors: Energy

- Aluminum Financing Threatened as Interest Rates Rise: Bear Case

- Maersk Four Rate Rises Fail to Spread as Demand Falls: Freight

- German Power’s Rebound Seen Ending on Coal Slide: Energy Markets

- Barclays Hires Four Commodities Staff From JPMorgan, Citadel

- Rubber Reaches 7-Week Low as U.S. Auto Data Raise Demand Concern

CURRENCIES

GLOBAL PERFORMANCE

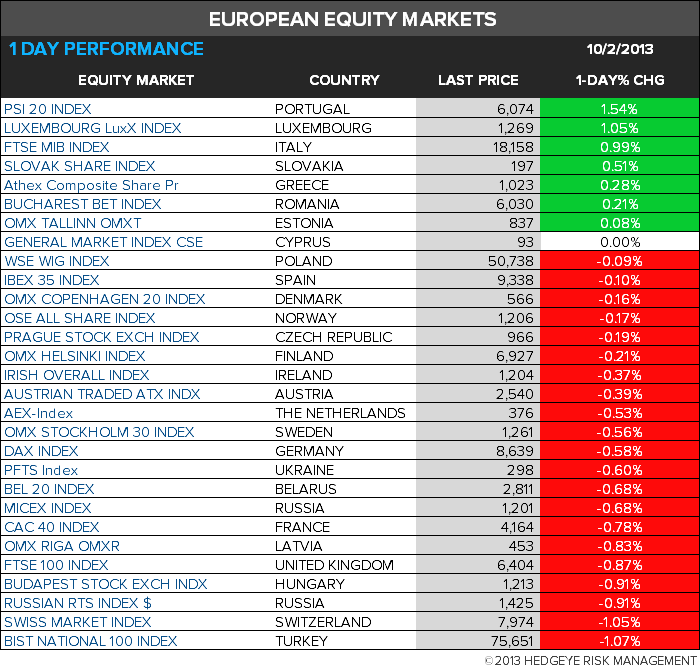

EUROPEAN MARKETS

ASIAN MARKETS

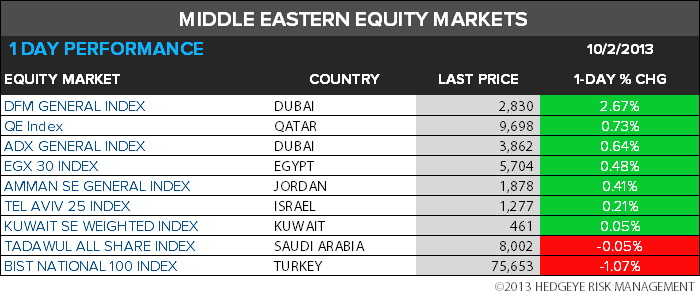

MIDDLE EAST

The Hedgeye Macro Team