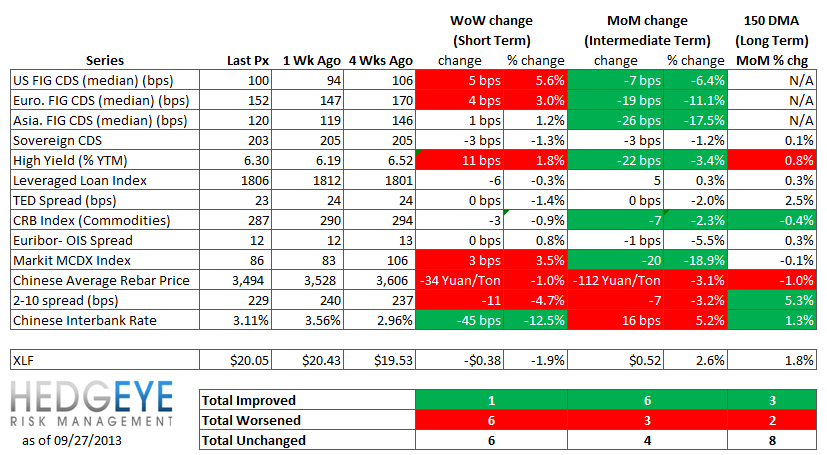

Key Takeaways:

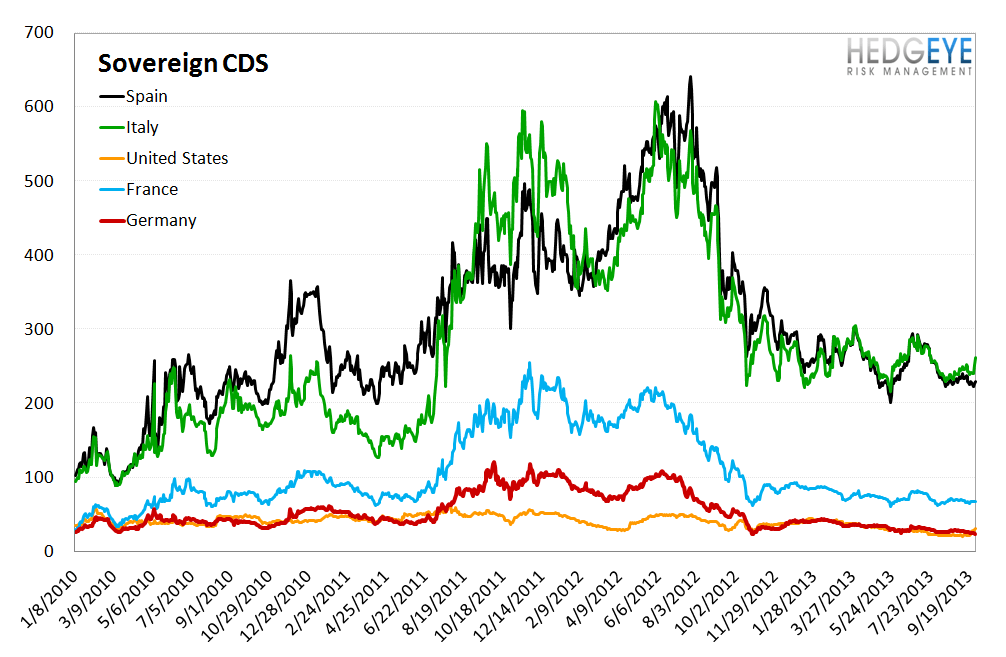

* Sovereign CDS – U.S. sovereign swaps rose 9 bps last week, rising from 22 bps to 31 bps (a 38% increase). This week will be an interesting one. We think the dual probabilities of a protracted impasse coupled with a better than expected Friday employment report could reverse the recent QE-led downdraft in long-term yields.

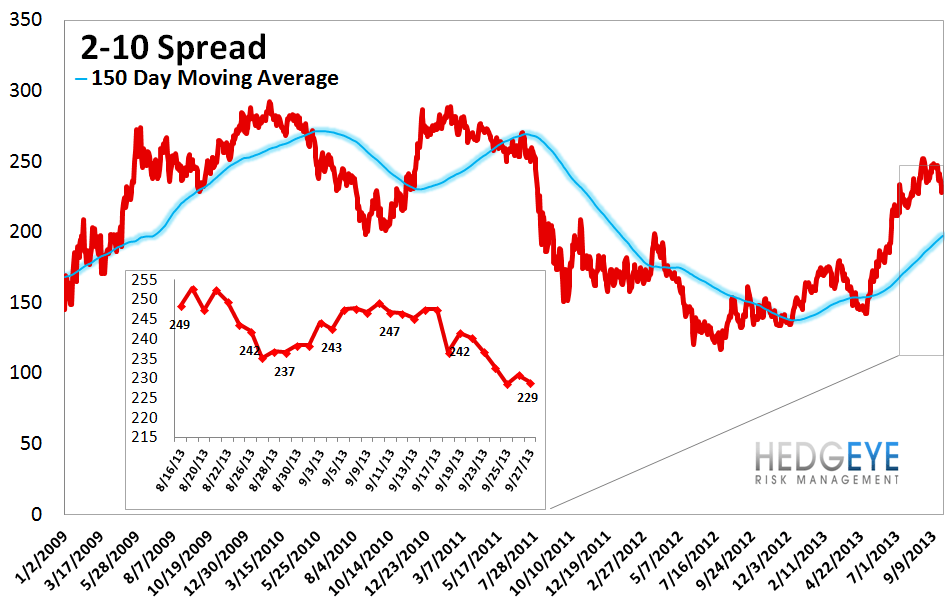

* 2-10 Spread – Last week the 2-10 spread tightened to 229 bps, -11 bps tighter than a week ago. Spreads have come in notably since their mid/late August highs of 252 bps.

* Chinese Steel – Steel prices in China fell 1.0% last week, or 34 yuan/ton, to 3494 yuan/ton. Chinese steel prices have been in steady retreat since August.

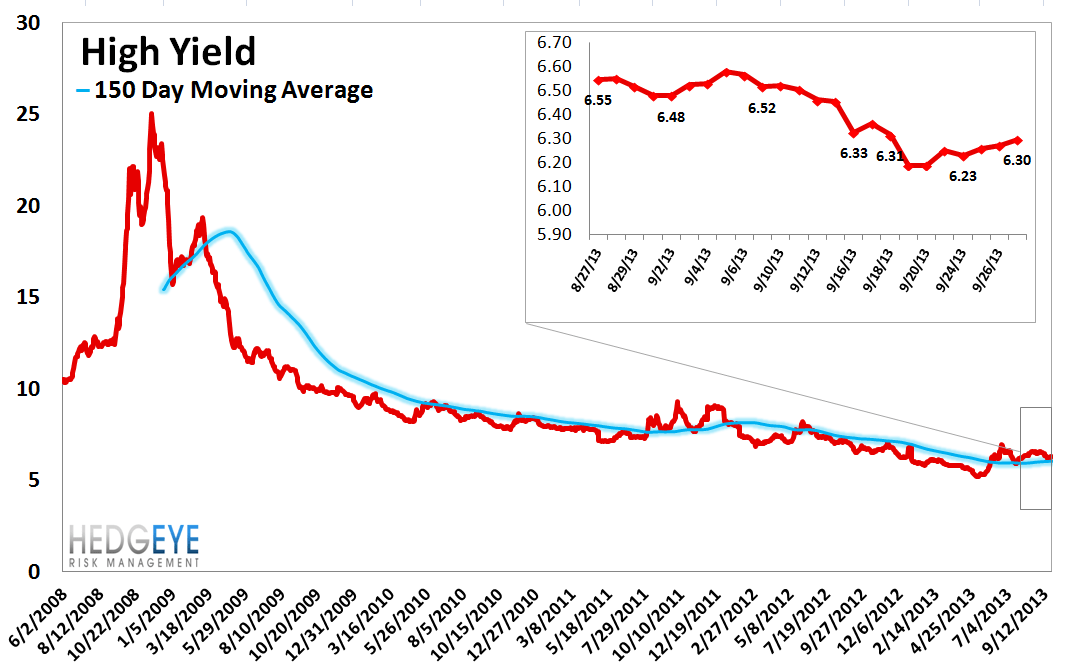

* High Yield – High Yield rates rose 10.9 bps last week, ending the week at 6.30% versus 6.19% the prior week. This marks a reversal of the trend in place since mid/late August.

Financial Risk Monitor Summary

• Short-term(WoW): Negative / 1 of 13 improved / 6 out of 13 worsened / 6 of 13 unchanged

• Intermediate-term(WoW): Positive / 6 of 13 improved / 3 out of 13 worsened / 4 of 13 unchanged

• Long-term(WoW): Positive / 3 of 13 improved / 2 out of 13 worsened / 8 of 13 unchanged

1. U.S. Financial CDS - JPMorgan led large caps higher, rising by 10 bps as reports of a settlement amount ballooned. BAC and C rose by approximately half as much. Mortgage Insurers saw 27 and 24 bps increases last week, casting a bit of a pall over the housing outlook. Overall, swaps widened for 23 out of 27 domestic financial institutions.

Tightened the most WoW: TRV, CB, XL

Widened the most WoW: MBI, JPM, COF

Tightened the most WoW: AXP, TRV, GS

Widened the most MoM: MBI, AGO, SLM

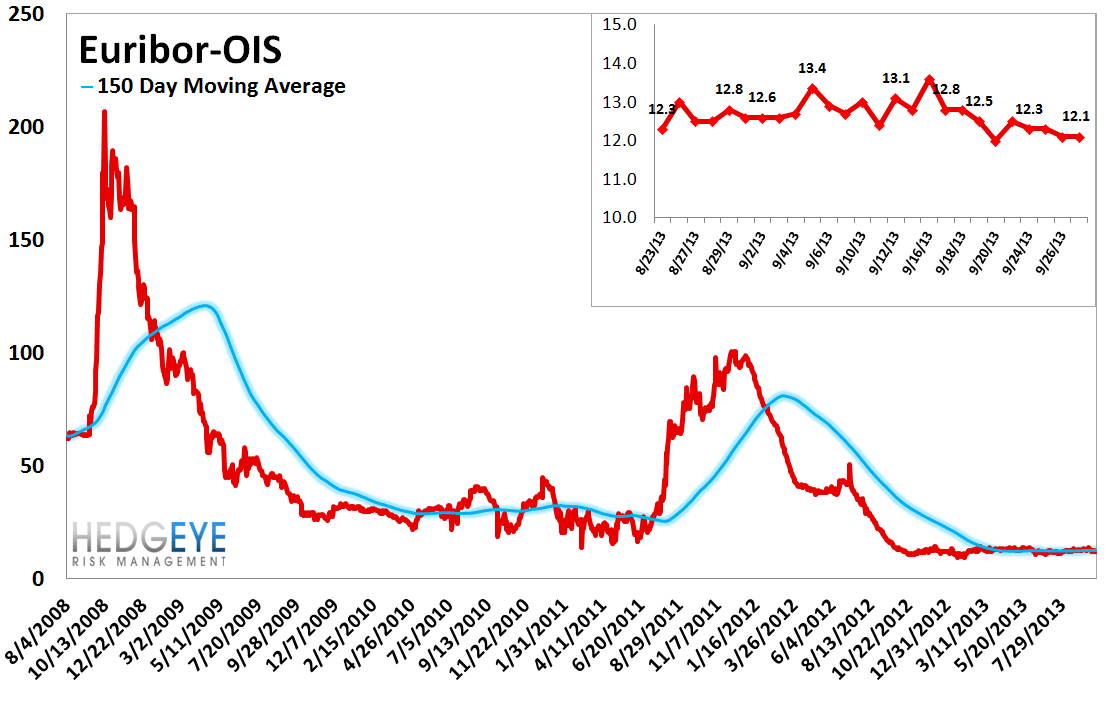

2. European Financial CDS - Swaps were wider throughout Europe's banking system last week with the exception of Spanish banks. Interestingly, Euribor-OIS was unchanged suggesting perceptions of systemic risk have not moved.

3. Asian Financial CDS - Indian banks resumed their losing ways with State Bank of India posting a 47 bps W/W increase to 309 bps. The other two major Indian banks were up 25 and 19 bps as well. Chinese banks were wider by 8-10 bps, while Japan's banks were flat to tighter by single digit bps.

4. Sovereign CDS – U.S. sovereign swaps rose 9 bps last week, rising from 22 bps to 31 bps (a 38% increase). This week will be an interesting one. We think the dual probabilities of a protracted impasse coupled with a better than expected Friday employment report could reverse the recent QE-led downdraft in long-term yields. Elsewhere, Italian spreads rose by 19 bps while Portuguese spreads fell by 32 bps.

5. High Yield (YTM) Monitor – High Yield rates rose 10.9 bps last week, ending the week at 6.30% versus 6.19% the prior week.

6. Leveraged Loan Index Monitor – The Leveraged Loan Index rose 6.0 points last week, ending at 1806.

7. TED Spread Monitor – The TED spread fell 0.4 basis points last week, ending the week at 23.3 bps this week versus last week’s print of 23.7 bps.

8. CRB Commodity Price Index – The CRB index fell -0.9%, ending the week at 287 versus 290 the prior week. As compared with the prior month, commodity prices have decreased -2.3% We generally regard changes in commodity prices on the margin as having meaningful consumption implications.

9. Euribor-OIS Spread – The Euribor-OIS spread was again unchanged at 12 bps. The Euribor-OIS spread (the difference between the euro interbank lending rate and overnight indexed swaps) measures bank counterparty risk in the Eurozone. The OIS is analogous to the effective Fed Funds rate in the United States. Banks lending at the OIS do not swap principal, so counterparty risk in the OIS is minimal. By contrast, the Euribor rate is the rate offered for unsecured interbank lending. Thus, the spread between the two isolates counterparty risk.

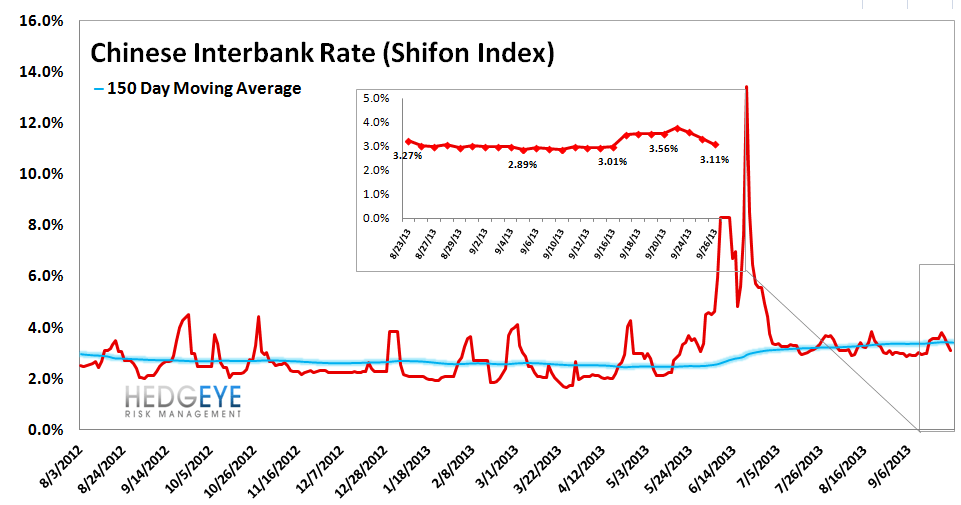

10. Chinese Interbank Rate (Shifon Index) – The Shifon Index fell 45 basis points last week, ending the week at 3.112% versus last week’s print of 3.557%. The Shifon Index measures banks’ overnight lending rates to one another, a gauge of systemic stress in the Chinese banking system.

11. Markit MCDX Index Monitor – Last week spreads widened 3 bps, ending the week at 86 bps versus 83 bps the prior week. The Markit MCDX is a measure of municipal credit default swaps. We believe this index is a useful indicator of pressure in state and local governments. Markit publishes index values daily on six 5-year tenor baskets including 50 reference entities each. Each basket includes a diversified pool of revenue and GO bonds from a broad array of states. We track the 16-V1.

12. Chinese Steel – Steel prices in China fell 1.0% last week, or 34 yuan/ton, to 3494 yuan/ton. We use Chinese steel rebar prices to gauge Chinese construction activity, and, by extension, the health of the Chinese economy.

13. 2-10 Spread – Last week the 2-10 spread tightened to 229 bps, -11 bps tighter than a week ago. We track the 2-10 spread as an indicator of bank margin pressure.

14. XLF Macro Quantitative Setup – Our Macro team’s quantitative setup in the XLF shows 0.3% upside to TRADE resistance and 0.6% downside to TREND support.

Joshua Steiner, CFA

Jonathan Casteleyn, CFA, CMT