This note was originally published September 27, 2013 at 07:48 in Morning Newsletter

Editor's note: Please enjoy this complimentary "Morning Newsletter" from Senior Analyst Darius Dale. While Hedgeye CEO Keith McCullough typically writes this newsletter, periodically, other members of the team jump in for guest appearances.

“What people fail to realize is that we spend ~70% of the time at record highs in the equity market.” Anonymous Seasoned Investor

The big picture

Keith and I picked up that gem in a recent meeting with a client out in San Francisco. Truly a savvy investor, this gentleman belongs to the increasingly rare camp of investors that has managed market risk across multiple decades and economic cycles.

Regarding the aforementioned quote, he dropped that line in a discussion about the pervasive lack of enthusiasm for 2013’s non-consensus equity market rally, specifically in response to our conjecture that baggage from the hard times of 2008-09 is broadly preventing investors from buying into the sustainability of said rally.

While I believe he was merely throwing a number out there to make a [wise] point, the reality is that he’s actually not that far off as it relates to the assertion he was trying to make:

- Being worried about allocating capital to the equity market at/near its all-time high is hardly as big of a deal as the average investor – fully loaded with 2000-02 and 2008-09 baggage – would have you believe.

- Over the past 30Y, the S&P 500 has traded within 5% of its [then] all-time high 43.8% of the time.

- Over that same duration, only 26% of the time has the index traded 20% below its [then] all-time high.

Oddly enough, when looking at aggregated fund flow and securities market allocation trends, it seems that investors are still positioned for yet another blow-up in the equity market, when, in reality, it’s the inevitable unwinding of Bernanke’s bond bubble they should be most concerned about.

Per Jonathan Casteleyn, the newest member of our highly-regarded financials team:

- Per the most recent data (2008-11 period), pension fund allocations to stocks is at an all-time low of 44%, while their allocations to bonds is at an all-time high of 37%. That ratio was 52% to 33% in the 1984-94 period, 64% to 27% in the 1995-00 period and 60% to 28% in the 2001-07 period.

- From the start of 2008 through the most recent data (JUL ’13), bond mutual funds have seen a cumulative $1.09T of inflows, or 17% of starting AUM. This compares to a -$441B outflow from equity mutual funds, or -7% of starting AUM.

- At $38T outstanding across the various categories, bonds represent 68% of the total US securities market (equities and debt). That compares to a 20Y average of 64% and a balanced ratio of 50/50 in 1999. Reversion to the mean implies a greater than $2T outflow from bonds into stocks over the long term.

Regarding that last point, we get a lot of pushback from fixed income managers that bonds funds don’t necessarily need to see outflows for the equity funds to receive inflows, citing record “cash on the sidelines”.

Indeed, un-invested cash in money market mutual funds, credit balances in margin accounts and deposit and currency assets on household balance sheets currently totals ~$12.4T, which is just off of all-time highs. As a percentage of the securities market, however, it hovers just above all-time lows (23% vs. a record low of 22% in 1999 and a record high of 32% in 2009).

If in 1999 someone thought the aggregate investment community was going to take its liquidity ratio down to new all-time lows in order to continue financing a bubble in stocks or even to take up its gross exposure by simply increasing its allocations to bonds, boy, were they sorely mistaken. Making that argument in defense of fixed income right now is equally off base, in our opinion.

Macro grind

In summary, we continue to believe there is a compelling, long-term fund flow case to be made in favor of the equity market in lieu of the bond market.

Not from every price, however…

We need to see the US Dollar Index recapture its TREND line of $81.35 for us to believe that tapering is an intermediate-term event, rather than one that is far off in the distant realm of “potentially never”.

Simply put, as long as a collection of fear-mongering doves dominate the domestic monetary policy debate, the probability of a Japan-like, no-growth economic scenario will remain heightened.

Besides a natural monetary policy response to economic gravity, what else would get investors excited about investing for growth in lieu of safety?

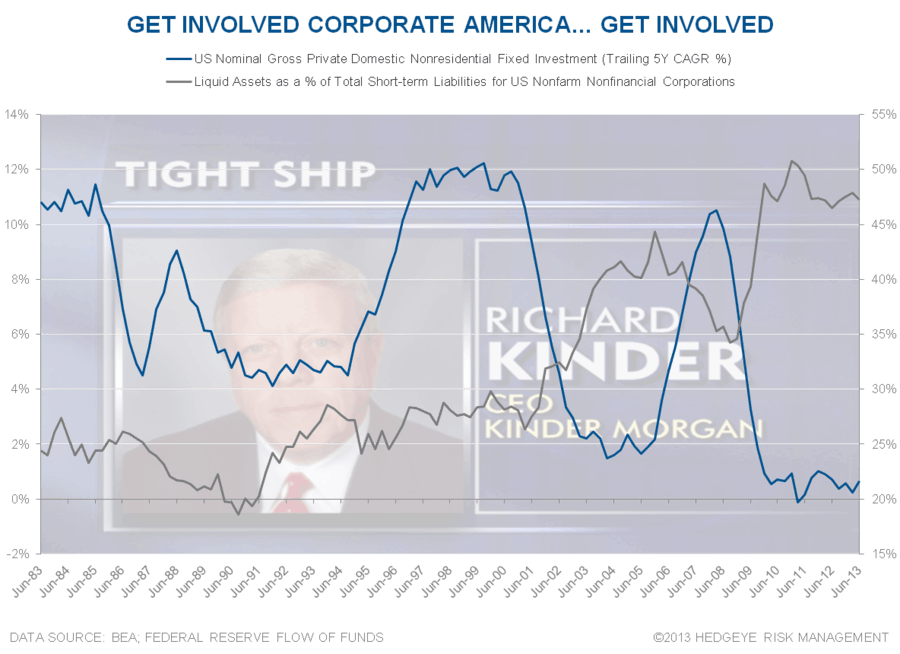

Corporate America would be a good place to start. My, how they have been conspicuously absent from this recovery!

Despite…

- Record cash on their balance sheets ($1.8T per the latest data);

- A near-record ratio of liquid assets to short-term liabilities (47.3%; 1.8 standard deviations above the 30Y mean);

- An effective tax rate of 19.9% that is near all-time lows (-1.6 standard deviations below the 30Y mean);

- An estimated $700B in interest savings since 2009 that can be specifically attributed to QE*; and

- Profits that have grown +34.7% since 2007…

… Corporations have reduced employee headcount by -2.9% since 2007 and grown nominal CapEx by a measly +0.6% on a trailing 5Y CAGR basis – a growth rate that is just above a generational low.

Regarding the former point on corporate, QE-derived interest savings, $700B is enough to employ 9.6M workers for 1Y, assuming a $51k median income (per the Census Bureau) that represents 70% of all-in employee compensation costs (per the BLS), effectively taking up the median annual comp to $72.9k. To put that in context, there have been only 6.8M net hires since 2009 per the seasonally-adjusted nonfarm payrolls numbers.

Obviously that’s nothing more than a hypothetical analysis meant to draw attention to the fact that QE to-date has been little more than an overt transfer of wealth to Corporate America and the rest of the top-10% that owns the lion’s share of financial wealth in the this country.

It’s time both parties said, “thank you” by putting capital to work (corporations) and allocating capital back to pro-growth assets (investors).

- CASH: 49

- US EQUITIES: 16

- INTL EQUITIES: 20

- COMMODITIES: 0

- FIXED INCOME: 0

- INTL CURRENCIES: 15

Our levels

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 2.57-2.74%

SPX 1684-1705

VIX 12.95-14.98

USD 79.99-81.35

Yen 98.02-99.17

Brent 107.40-110.61

Keep your head on a swivel,

Darius Dale

Senior Analyst