INVESTING IDEAS

Here are the latest comments from Hedgeye Sector Heads on their high-conviction stock ideas.

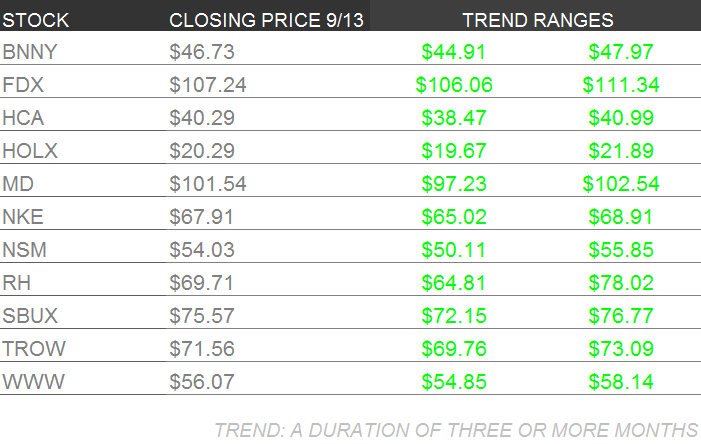

BNNY – Despite slightly disappointing top and bottom line Q1 2014 results (released on 8/8/13), Consumer Staples analyst Matthew Hedrick says Annies’s maintained its FY revenue outlook of +18-20% and EPS guidance in the range of $0.97 to $1.01.

Hedrick believes BNNY’s premium valuation is justified by higher growth rates across organic offerings, of which Annie’s is a leader, especially as it increasingly moves its products to the mainstream aisle from the organic aisle. BNNY caters to a higher income demographic that Hedrick says should continue to pay a premium for organic foods despite fluctuations in macroeconomic conditions.

Hedrick says BNNY could see another quarter of challenged gross margins but he expects a rebound in sales as the company spend more on advertising, rolls out its frozen pizza and family sized frozen meal offerings, and continues to take share across mac & cheese, crackers and fruit snacks from more traditional brands. BNNY’s strategy to innovate everyday foods and create healthier and better tasting options should sustain long-term growth, and Hedrick looks for BNNY to maintain its market leadership and gain share as it moves more of its items to the center of the store.

FDX – FedEx reports next Wednesday, so Industrials sector head Jay Van Sciver expects volatility in the coming week. Van Sciver says the market will likely focus again on the adjusted margin in the Express division. FDX will be reporting just the second quarter with benefits from the Express division restructuring.

If the company can come close the excellent Express margin improvement delivered last quarter, then expect the report to be well received. Van Sciver is confident that FedEx can either meet or come close enough to meeting its FY16 Express profit improvement goals to drive share price outperformance, but he cautions that a single quarter can swing either way, with a short-term knee-jerk reaction in the marketplace.

The operating environment this quarter should have been supportive, with many macro data series improving through August. That said, Van Sciver says investors worried about short-term volatility could pay up to hedge with pricey September 21 puts.

HCA – Last week Healthcare sector head Tom Tobin flagged two data series which would be important to our near term outlook for HCA Corp. The US Treasury released their Monthly Treasury Statement yesterday. Unfortunately, the update continued a weakening trend Tobin has been documenting for some months.

In addition, Tobin’s proprietary OB/GYN Tracking Survey for September continues to reflect a soft maternity trend, a key source of inpatient and outpatient admissions for hospitals. Thesis drift happens when you’re long a stock for a reason and things don’t go as planned, and HCA appears to be heading in that direction. Tobin will be taking a step back to reviewing the case for HCA over the coming days.

MD – Mednax shares have had a good run in recent weeks and this week responded positively to news of an additional acquisition. The company has guided to significantly more acquisitions than they have completed so far in the second half of 2013. That’s good news in terms of having something positive to look forward to.

Tobin’s proprietary OB/GYN tracking survey for September came in weak again in September for maternity trends. Tobin believes the survey, which represents approximately 20,000 patients, is representative of a significant part of the Medical Economy.

HOLX – New Hologic CEO Jack Cumming threw some cold water on expectations for 2014 at the Morgan Stanley Healthcare Conference earlier this week. The shares did not respond well to comments that 2014 is a rebuilding and investing year.

Healthcare sector head Tobin says it is difficult to tell how much of Cumming’s commentary was an effort to lower expectations so he can beat them, or the cold reality of what he’s seeing in his weekly sales reports and ongoing business review.

Says Tobin, “We still have a lot to look forward to with September quarter guidance cut to the bone, an expected 3D Mammography payment code issued, and the Affordable Care Act, which if it helps any company, will provide a big tailwind to Mr. Cumming’s planning.”

NKE – Retail sector head Brian McGough saw good news for Nike this week out of the largest sports apparel and footwear retailer in the UK, Sports Direct, which reported sales growth of 18%, and 23% gross profit growth, marking a definite pick-up in sales cadence from earlier this year (and all of last year). This synchs with recent comments out of Foot Locker that its European business is stabilizing.

The cadence of growth in the channel appears to be going the opposite way compared to what we see in the US, with the latest week’s footwear sales growing by less than 1%. That said, NKE’s sales are trending in the mid-single digits, showing yet continued share gain in the US. In the end, the datapoints are positive with NKE’s earnings 2 weeks out, and analyst meeting in a month at its world HQ offices.

NSM – Nationstar Mortgage remains on a roll, hitting another new high this week. This past Friday the mortgage industry trade publication Inside Mortgage Finance (IMF) reported that both Wells Fargo and JPMorgan were close to announcing sales of $40 Billion and $70 Billion, respectively, in UPB mortgage servicing rights.

It’s interesting how these two figures together match quite closely the $100 Billion increase to the acquisition pipeline that Nationstar announced when it rolled out its 2Q13 earnings results. We would expect NSM to be a prime contender for acquiring one of these blocks of servicing. As we’ve been highlighting recently, the main risk to keep tabs on with Nationstar remains interest rates rising.

The reality is that rates continue to rise on the back of strengthening US economic data and a growing expectation that the Fed will begin tapering asset purchases sooner than previously expected. Rising rates are inversely correlated with mortgage origination volumes, as refinancing activity drops rapidly in response to higher rates.

Nationstar derives a significant portion of its earnings from mortgage origination, but is more defensive than a traditional mortgage bank as their originations are largely sourced through the HARP channel, which is less rate-sensitive than the traditional refi channel. Nevertheless, origination volumes are likely to come under pressure amid further increases in rates and this will weigh on earnings upside going forward.

TRADE: In the short-term, we think the market will be watching for the next sizeable MSR sale.

TREND: Over the intermediate term, the stock will key off 3Q13 earnings results, deal announcements and the direction of long-term interest rates.

TAIL: In the long-term, there is still a tremendous opportunity for non-bank servicers like Nationstar to roll-up the servicing business. NSM is well positioned to be a prime beneficiary. We continue to think consensus earnings estimates remain too low for 2013/2014.

RH – Retail sector head Brian McGough says people are asking the wrong questions about Restoration Hardware. The key question, says McGough, is when will the company earn $8.00 per share. McGough believes the answer is 2018.

McGough says it was painful listening to analysts grilling management on the RH earnings call, all wanting to be spoonfed precise guidance in the coming quarters. “We love math as much as anyone.” Says McGough, “but seriously…this is a company that should earn about $1.50 per share this year, and people are asking for guidance on items that account for maybe a nickel a share?

Here’s a better question… How long will it take for RH to earn $8.00?”

McGough’s math suggests that we’ll see that number around 2018. That’s $6.50 in incremental earnings in 5-years, or a 40% earnings compound annual growth rate (CAGR), a pretty potent argument for those who think RH is too expensive or, worse, that they “already missed it.”

The definition of a Growth Stock is, first you buy future earnings, then you buy upcoming earnings, then you buy current earnings. Finally, you buy an established cash cow. McGough concedes that RH shares can be volatile, but says simple projections on forward earnings extrapolate out to a $90 stock within a year, a $125 price in two years, $175 three years out… that’s just the way that growth grows.

We did an institutional call on RH at the IPO (at $32) and have an update coming in the next couple of weeks – which we’ll feature here. McGough thinks the stock has already worked, notwithstanding a bump in the road this week, and says it should continue to work for much higher numbers over the next 2 years or more.

SBUX – Hedgeye Restaurants sector head Howard Penney has no update on Starbucks this week.

TROW – Hedgeye Financials director Jonathan Casteleyn has no update on T. Rowe Price (TROW) this week.

WWW – Hedgeye Retail sector head Brian McGough has no update on Wolverine World Wide this week.

Macro Theme of the Week – How Fragile Is China?

Hedgeye’s Q3 Macro Theme - #AsianContagion – has not swerved into reverse, but senior Macro analyst Darius Dale says this week’s developments indicate we should not be short China right now. Of course, the lift in the Chinese markets has brought out a sudden emergence of China bulls – or perhaps better put, an emergence of sudden China bulls. Nothing like a short-term market reversal to have people switching hats and sneering “I told you so!” Dale counsels caution on both sides. The markets are not so clearly in trouble as they were – but neither are they out of the woods.

This week saw the Shanghai Composite close above Hedgeye’s proprietary model TREND line amid what Dale calls “the only positive data point that actually matters.” The Politburo announced plans to speed up the development of the Shanghai free-trade zone (to be launched later this month), with the intention that it will take the lead in financial reform – eventually rivaling Hong Kong as China’s main international financial center, and with intentions for it to become a global financial center by 2020.

We hosted expert call in April titled “Will China Break?” with former JPMorgan China head Dr. Carl Walter, who said China still has far to go before it develops credible capital markets. The stock markets were primarily a policy tool to permit China’s State-Owned Enterprises (SOEs) to raise non-bank capital, offering visions of Potemkin capital markets to the outside world. It is significant to note that, out of tens of millions of trading accounts on China’s exchanges, only about 7% actually execute transactions.

Without a true financial marketplace, China has had no market discipline to accurately price its securities, bonds and loans to attract serious inflows of foreign capital, or to drive growth. The captains of China’s ship of state – headed by the dynamic and personable General Secretary Xi Jinping – recognize that economic growth is the ultimate safety valve. More than the solidity of their banks – which they will keep in business by fiat, if necessary – Party officials are deeply concerned about the potential for civil unrest. This has led to excessive focus on local economic programs. But the country is already significantly overbuilt. At the same time, economic inequality continues to grow.

Some 300 million people have been brought up out of poverty in China in the last 20 years – but that leaves one billion people who have not. There is still significant inequality, an aging population, and a diminished younger generation to rely on, thanks to years of the one child per family policy. The difficulty of establishing a consumer-based economy under these circumstances is exacerbated by a very real possibility of social unrest in the coming years. Dale believes the Politburo announcement could signal a take-the-Chinese-bull-by-the-horns approach that could wrench the economy to its feet.

The program contemplates broad liberalization across commercial sectors, with the banking sector being the most important, as the Shanghai free-trade zone will be at the forefront of interest rate liberalization in China. Regulators will authorize full capital account conversion on a trial basis, as a first step towards attracting foreign capital. This could wind up being extremely positive, if it manages to offset China’s structural liquidity headwinds with new sources of capital. So far, it’s only an announcement, and far too soon to tell what the real outcomes are likely to be. But note that, unlike Western politicians, the Chinese do not speak very often. And when they do, they invariably carry through on what they say they’re going to do.

Says Dale, “if the market truly believes the Shanghai free-trade zone will be meaningful enough to help offset the structural liquidity constraints we see weighing on Chinese economic growth over the long term, then so does Hedgeye.” This is definitely a call to stand aside and watch while China’s leadership determines its next steps. At a bare minimum, Dale says investors should no longer be shorting China here.

Un-Shorting The Contagion

China is not “cured” of its contagion, even if the condition is dormant. Dale emphasizes that we are still plenty bearish on emerging markets. The bounce in the emerging markets this past week has some forgetting that these markets are still down for the year, some of them substantially.

But the recent announcement means it is no longer prudent to speculate on China’s banks collapsing. Or, as Dale delicately puts it, “a wholesale negative revaluation of the Chinese banking sector.” Yes, there have been significant liquidity and credit quality issues plaguing the banks for some time. But the government would not, in any event, have permitted the banks to go out of business. American analysts recall the Chinese were agog when Lehman failed – how could a major power allow one of its flagship financial institutions to just go out of business? If the Politburo manages to introduce even a small increase in market discipline to the banking sector, it will be a very great leap forward, indeed.

Dale notes that this poses a new dilemma for the individual investor, because most of us can’t go to Beijing to meet with local business executives and bankers and identify which companies are likely to suffer in the current environment. Thus, investors have generally gone long or short the Chinese market through a number of ETFs. Dale says the most liquid ones are generally heavily concentrated in markets that are flashing improved fundamentals (South Korea and China, for example) making them poor short candidates. The EEM Asia ETF, for example, is over 30% weighted to South Korea and China, making it a poor proxy for general Asia weakness.

At the same time, conditions have not improved to the point where it is unambiguously safe to go long these ETFs. We remain bearish on emerging markets from a top-down perspective. But it is no longer prudent to passively short EM capital and currency markets at the asset class, regional and country levels. This makes ETF investing dicey in the current environment, on both the long and short side.

You may consider it bad news that there’s no one trade you absolutely have to do today. The good news is that China is too big to recover on its own. Its eventual transformation from a state-controlled economy fraught with waste, corruption and social inequality, to a market economy with a banking sector that participates fully in the global marketplace, will be both the result, and a driver of a global economic recovery. Critically, if market reforms show signs of gaining traction, it will add greatly to China’s ability to convince Westerners to bail out its banks (and the broader Chinese economy) for the second time in as many decades.

Sector Spotlight – Restaurants: Will Fast Food Take Wing?

Nothing To Be Casual About – Restaurants sector head Howard Penney has been negative on the casual dining group since early June, and he says a preliminary look at August figures “showed little improvement from an ugly July.” A number of the top casual dining companies saw their same-store sales either revised downward, or left unchanged in the past month, and Penney notes that September’s back-to-school effect historically has been a drag on the sector in general.

Penney says investors warming up to growth in the casual dining segment need to watch the road with both eyes. Listening to too many talking heads can lead you to some very wrong conclusions, with a significantly bad outcome for your investment portfolio.

The Full Service Restaurants added some 17,500 employees in July, and Limited-Service added just under 16,000. Penney says this continues the trend where the restaurant industry ís among those leading the improvement in payroll data.”

All well and good. But full-service casual dining is losing customers, as industry statistics indicate traffic declined 1.9% in August, leading to softer same-store sales.

Recent employment trends are also flashing negative signals for casual dining, as employment growth rates slow, or actually decline across the 45-64 year-old groups. Managements readily acknowledge the impact of employment in their core consumer groups, and the shift to younger workers and shorter work weeks could lead to persistent weakness across the sector, says Penney.

As for stock buyers, remember that investors chase price. Penney cautions that the Bloomberg Full-Service Restaurant index is up 30.8% year to date, while the S&P 500 is only up around 18%. Do you rush out and buy the sector that’s outperforming? Do you buy right when the group is about to underperform – maybe substantially? Penney cautions that both hiring and stock prices in the segment may be way ahead of themselves.

McDonald’s: A Wing And A Prayer?

Among the most visible of the fast-food giants, Penney has been notably negative on McDonald’s (MCD) since putting out his Short call on the stock on 4/25 (closing price on that date: $100.94). His stark read today: “MCD has a top-line issue, and not a cyclical one.” To put it in Hedgeye’s macro context: in an environment of economic growth, MCD management has maneuvered the company into a position where it cannot benefit from improving economic fundamentals.

We have seen this coming. Penney earlier quoted (you should excuse the expression) the whopper of a statistic (see Investing Ideas of 31 May) that over 70% of MCD’s customers order almost exclusively from the Dollar Menu, a promotion that has turned into a Frankenstein Monster that generates little ongoing sales growth, and almost no profit margin. Penney called this an iron-clad cap on the company’s ability to grow its business domestically. “Why would you buy a double-quarter-pounder-with-cheese meal for $6,” he asked, “when you can buy four McDouble cheeseburgers plus fries and a soda off the Dollar Menu at the same price?”

Now, MCD management has come up with a new product to save the day: “Mighty Wings.” Penney fears this is almost guaranteed to crush the remaining life out of the franchise. You’d think MCD management never steps inside their own restaurants. The company has already put their franchisees behind the 8-ball with the Dollar Menu, forcing them to run their business on razor-thin margins. Their new brainstorm is to bail out this sinking business with a product that is not novel (chicken…?), not differentiated (think: Buffalo Wild Wings), not glowing with premium cachet (like we said, chicken), and actually takes a longer time to prepare than the traditional MCD menu items, which are already beset with time-and-motion issues.

If 70% of your customers are buying your lowest-margin product, you can only salvage profitability by cutting down the resources required to prepare and serve. In earlier discussions Penney criticized management for putting the drinks stations too far from the service counters, for example, adding precious seconds to the time required to get to the next customer, and slowing critical drive-through times. If the wings product really is that much slower to prepare, MCD could be setting themselves up for a disaster that could manifest as early as the fourth quarter.

Confirming Penney’s dim view, MCD’s management was fairly opaque at this week’s Goldman Sachs investors’ conference. “The initial comments from the presentation suggest that they believe the economy is to blame for their difficult sales trends,” reports Penney. He says this is starting to mirror the decline of a “mismanaged McDonald’s brand” during 1 when “the company was focused on unit growth and cost reduction rather than driving high margin, top line sales. As the image of the brand began deteriorating, management failed to invest in the brand and customer experience. Rather, they turned to monthly promotional tactics to in order to drive short-term sales at the expense of brand equity and margins. This strategy did not end well for either the company or investors and we’d be surprised if this time was any different.”

For Penney, MCD continues to be a situation where the mainstream investing community is paying more attention to management’s story line than to the meat on the bun – a classic case of sizzle with very little steak. The company reported August sales this week, and while the numbers were slightly better than anticipated, Penney says it was not enough for him to change his fundamentally bearish view. So not only is MCD not about to get a break domestically, they also don’t look to be bailed out by China, even though Asian sales overall were less bad than anticipated. Penney still sees “a disconnect between investors’ expectations and the company’s fundamentals.”

Until management changes the business model to tackle profitability instead of quarter-by-quarter cosmetic boosts to revenues, MCD shares are not going to provide a Happy Meal for investors.

Don’t Mind The Gap – Penney issued a fascinating analysis this week of what could be a definitional new demographic, a gender gap-less society. In his posting (9/10 “The Boomer/Millennial Convergence”) Penney highlights a handful of new products and business models that appeal to both the Baby Boomer and Millennial generations.

Among such gapless phenomena he lists:

- Tesla premium electric vehicles

- Chipotle’s food and preparation process

- Whole Foods’ holistic approach to selling food and health

- E-Cigs’ new experience for smokers

- LinkedIn redefining professional networking, recruiting and job searching

- Smartphones

“In the new consumer landscape,” says Penney, “a product or service that can span two generations is a game changer.” Penney says Boomers and Millennials are converging as parents and their kids “enjoy shopping and eating out at the same places,” and not infrequently groove to each other’s music.

We suspect this arises from a cross pollination, where Boomer generation parents permit themselves to be influenced by their children’s choices, rather than insisting on rigid adherence to old rules. We further speculate that it is the product of a society bathed in luxury and freedom from want. In most of the world, people walk several miles before dawn to stand on line for hours to obtain a half a loaf of bread. In America, it’s the latest iPhone.

But whatever the complex of reasons behind it, the Gapless Society is clearly an important new demographic. (Indeed, as a somewhat further-along Boomer than Howard, your correspondent witnesses within his own family his 92 year-old mother who learned to surf the ‘net from her granddaughter, and who now emails with her grandchildren, Skypes with her great-grandchildren, and tells her son, the writer, “what? You mean you haven’t read it yet? You have to Kindle it right away!”) Much of Wall Street hasn’t yet figured out that people are no longer doing things the way their parents did – largely because so many influential consumers are doing things the way their children do.

The convergence is more than one of tastes. It is also one of values. Penney points to a company like Whole Foods (WFM) as “a company that spans multiple generations,” and is a paradigm for the kind of company Penney is on the hunt for, “companies that are leveraging new business models, while avoiding companies with traditional business models that are coming under pressure.” There are many people who have never known a world in which just-in-time production was not available, in which customizable content downloads were not the norm, and where you could not instantaneously blast out your most idle passing thought to tens of thousands of devoted friend-fans. If you are one of those folks, God bless you. You have no idea how massively the world has changed.

Much of industry – and Wall Street, to be sure! – also has no idea how massively this gapless shift has altered the landscape of business. Focusing just on what goes into our mouths, Penney notes that Millennials put a high priority on healthy food options and high integrity companies, and that “Technology, in particular mobile, has emerged as the best channel of communication for producers and suppliers, giving them a competitive advantage and the ability to appeal to a widespread, growing base of consumers.”

Penney believes a major motivating factor is consumer stress, arising from information overload. You may not realize it, but when your parents started watching television, they had to get up out of their seat and walk over to the set every time they wanted to change the channel. Now, their grandchildren blitz through several thousand internet entries in the space of seconds and come up with a menu of choices: do you want coffee, or tea? Artisanal fresh-roasted coffee, or beans from a premium chain? Free trade coffee, or imported by a major supplier with reliably predictable standards of flavor and aroma? And so on…

With the plethora of available information, Penney says “people consistently seek to make smarter choices, leading them to purchase items with a higher perceived value. Value is not simply about price and varies from industry to industry. For example, in the restaurant industry, value is now a combination of price, quality, environment and experience, with an added emphasis to experience. This is why a $7.50 burrito from Chipotle may have a higher perceived value than a $4 Big Mac from McDonald’s.”

Now comes the kicker. The consumer is feeling a pinch. Disposable income per capita is growing at an annual rate of 1.1% in 2013 year-to-date. That’s less than one-third of the 3.8% average annual growth rate during the decade 2000-2009. Penney hypothesizes that the combination of access to more information, more sophisticated tastes, and a definite need to obtain more value for one’s money are “driving consumers toward higher perceived stores and restaurants and away from lower perceived, traditional ones.”

This is proving out, writes Penney, in a shift in the kind of restaurant company investors are willing to pay for. In the age of the gapless consumer, choice and quality are the sine qua non of a successful business. Penney says companies that provide better quality food, and provide it in a “just in time” setting, are going to increasingly take business away from traditional casual dining companies.

As just one example, Penney cites recent IPO Noodles & Company (NDLS) which offers cooked-to-order dishes, served on real china – and which boasts a stock price that has risen over 150% since its IPO in late June. Now that’s what we call Made To Order!

Investing Term – Master Limited Partnership

Hedgeye’s senior energy analyst, Kevin Kaiser, has gotten plenty of publicity over his analysis of oil and gas Master Limited Partnerships – MLPs. This week Charlie Gasparino interviewed Kaiser about his recent bearish report on Kinder Morgan Energy Partners (KMI), the granddaddy of all energy MLPs.

MLPs are favored by investors looking for safe, above-average returns. This includes a large percentage of folks in, or nearing retirement. And there’s no denying that many MLPs have provided impressive returns for the last decade or more. It has been a popular sector. According to the National Association of Publicly Traded Partnerships, the total MLP market is over $440 billion, of which $395 billion, or 89%, is in energy and natural resources. We estimate that some 70% of the holders of MLPs are retail investors.

Investors (“unitholders”) in an MLP, like shareholders of a public company, exercise no control over the business and have no liability beyond the amount of their investment. (Hence “limited” partners.) The partnership is managed by the General Partner – usually a separate legal entity that makes the business decisions and hires and directs management.

Unitholders receive regular cash distributions, which are generally specified in the partnership documents. The tax code allows certain companies, especially those in oil and gas production and transportation, to operate as MLPs, which exempts their income from most state and local taxes. This leaves a pool of cash for distributions to unitholders. The GP receives cash incentive payments when distributions are made, based upon the total amount of LP distributions. The bigger the distribution, the bigger the payment to the GP. And MLPs have a pattern of increasing payments, with the result that the GP takes in larger payments. Depending on whether you are a cynical stock analyst, or the GP, this is either a vicious cycle, or a virtuous one.

MLPs have many of their own accounting metrics. They have been permitted – we would say “incentivized” by a supine Congress and comatose regulators – to apply subjective accounting standards not in conformity with GAAP (Generally Accepted Accounting Principles, the fundamental standard metrics on which all businesses report their financial results). Companies generally use non-GAAP accounting if the result is justified by the unique realities of their business, and non-GAAP reports are sometimes presented alongside a GAAP near-equivalent, to permit clear comparison.

MLPs report an item called Distributable Cash Flow (DCF), which is the mother of all non-GAAP metrics. Logically, DCF is the money left over after paying the expenses of running the business. But as managements must smooth quarterly payments, and often increase them, the job of managing DCF can become far more important than the job of actually running the operating business.

Every MLP puts a slightly different spin on how they report DCF. Some of their measures appear vague, opaque, misleading, or simply wrong. Among the problems Kaiser identifies are: accounting for hedges on oil and gas production, accounting for the cost of acquiring other companies to capture their cash for distribution payments, and accounting for the cost of repairing and maintaining capital equipment such as pumps and pipelines.

Use of non-GAAP reporting could substantially understate the actual cost of doing business, and the MLPs often compound the issue by adding back expenditures to their stated asset base. Certain MLPs report capital expenditures as “expansionary,” when in reality a lot of the spending is basic maintenance without which their business would literally dry up.

These issues appear especially in “upstream” MLPs that produce oil and gas. Upstream MLPs got in trouble in the 1980s when many of them borrowed heavily to buy producing properties that were running dry, then were hit with price volatility and inefficient hedging markets. Upstream MLPs fell out of favor and were replaced by Midstream MLPs, middlemen who transport oil and gas through their pipelines. In the media debate around Kaiser’s latest research, you may have heard folks say “these companies are a toll road: they get paid every time something travels along their route.” That’s mixing apples and oily oranges.

“These companies” – the ones Kaiser is focused on – are upstream MLPs; their own oil and gas sales revenues are a critical part of their revenues. They must actually produce oil and gas, they must hedge efficiently, and the energy market has to be willing to pay a price that allows them to book a profit. They also really need functioning pipelines to deliver their production, and if Kaiser’s analysis is accurate, some of these pipeline MLPs may be starving their infrastructure of critical maintenance capital.

The upstream MLP segment has had a terrific run. Kinder Morgan has routinely been praised as one of the top companies in US industry, with good reason. Its founder and CEO, Richard Kinder, is an acknowledged giant among business leaders and a multi-billionaire who receives $1 a year in total compensation as CEO of Kinder Morgan. Since its creation in 1997, Kinder Morgan has provided approximately a 25% compound annual average total return to its unitholders. When Kaiser’s report on Kinder came out, the stock price sagged. Richard Kinder showed his faith in the operation, plunking down $18 million to buy half a million units in the open market.

So how can we be so negative on this company?

Kaiser’s analysis shows the MLP sector is fraught with accounting irregularities, all of which appear to be legal, and none of which appears to feature prominently on the radar of either Congress or the SEC. (Well, maybe Congress, considering the flow of campaign contributions and payments to lobbyists from the energy sector.) Among the most opaque and convoluted financial reporting, Kaiser’s analysis leads him to believe KMI’s true free cash flow is not anywhere close to the DCF number it reports.

Does this mean Kinder Morgan is a fraud? No, – they appear to be following the law to the letter. Does this mean the MLP sector as a whole is dishonest? Not at all. Particularly not on Wall Street (or in Washington), where the concept of “honesty” is on a par with the concept of “privacy” in the Age of Facebook (and the NSA.)

And it especially doesn’t mean that Kinder Morgan is about to spin, crash and burn. Kinder Morgan has produced outsize returns for an army of happy investors for a decade and a half, and there’s nothing to say that will stop today. But Kaiser is convinced it will ultimately stop. Like so many of the implosions we have seen in recent years, this will happen imperceptibly slowly – and then, all at once.

This is a huge story – there are some 100 energy MLPs. Kaiser has tackled five of them, and all have shown the same issues around transparency. There’s no immediate catalyst to make these stocks all go down. What there is, is – there are about $395 billion in natural resources MLP units held largely by individuals in, or planning for retirement. These are “safe” and conservative portfolios. What there is, is a large number of individual investors who sleep soundly at night, because they actually have no idea what they really own in their portfolios.

When they wake up, there could be hundreds of billions all racing for the exit, all at once.

Last Word: Just A Number

We haven’t overlooked the folks falling over one another to be the first to point out that Kaiser is “only” 26 years old, with the strong implication that, at that age, he should be seen and not heard. The rabbis of the Talmud observe that the finest old wines may be packaged in new containers and urge us to taste the wine, rather than criticize the barrel.

We note that at age 26, Napoleon saved the French Republic by single-handedly organizing the artillery defense of the Directorat. And it was purportedly at age 26 – or thereabouts – that Alexander sat and wept because there were no further worlds to conquer. Age is a number, not a measure of competence. Experience may be an excellent teacher, but most folks don’t pay attention in class.

Kevin Kaiser – and the rest of us at Hedgeye along with him – will either be right on this analysis, or we will be wrong. That’s a risk we take each day. To those who take exception with Kevin’s analysis, please show us where he’s wrong. We welcome the dialogue – it will make us better analysts. To those who publish snotty comments about Kaiser’s age, aren’t you ashamed for criticizing him over being something at age twenty-six that you were not?

- Moshe Silver

Moshe is a Hedgeye Managing Director and author of the Hedgeye e-book Fixing A Broken Wall Street