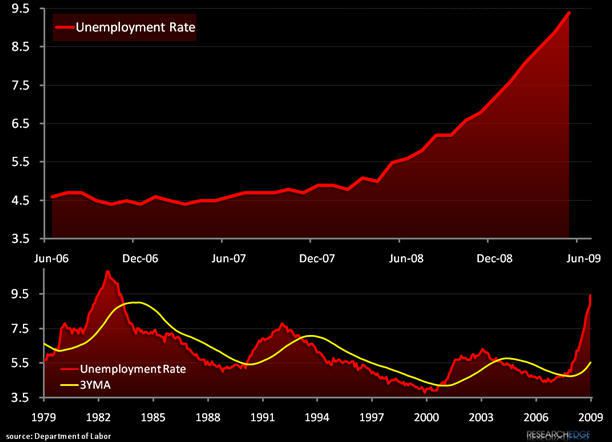

Yes, the 345,000 print that the manic futures traders chased each other on was better than expected, but I don't think they could have had the time to model the number that matters here - the unemployment rate.

I was at 9.3% for the month and it came in even higher than that at 9.4% (consensus was 9.2%). I was at 9.3% because I thought that the sequential acceleration in the unemployment rate would stay at 40 basis points (month-over month). It shot above that to +50 basis points.

So THE point here is that the sequential rate of unemployment just RE-ACCELERATED!

Recall that one of the main tenets to our bullish bias for the last 3-months has been the (E - Employment) in our US Consumer MEGA Squeeze call. The call was based on the unemployment going up at a lesser rate - and that it did for the past few months...

That delta shifts back to the danger zone today. Sequential accelerations matter.

KM

Keith R. McCullough

Chief Executive Officer