We like KKD on the LONG side, as the company fits our strategy of looking for small cap growth companies with strong business models and growth prospects. Over the past three years, the company has transformed itself into a strong regional brand and asset-light business with unique global growth potential.

Our KKD LONG thesis consists of three key tenants:

- International growth opportunity

- Accelerating U.S. unit growth

- The strong financial profile of the company

International Growth Potential

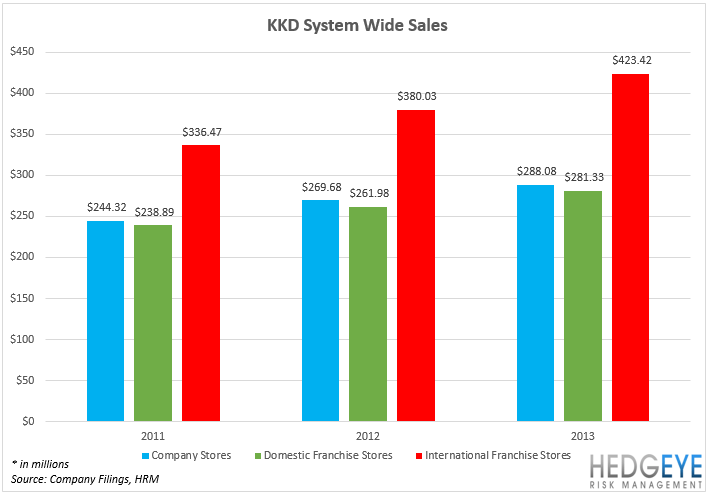

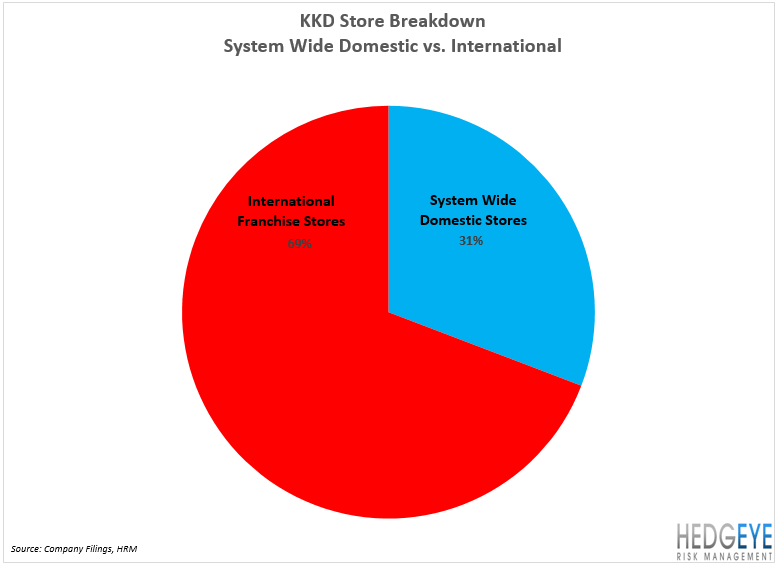

Since opening the first international store 11 years ago, international stores have grown to 532 and most recently, since 2007, have grown from only representing 31% of KKD’s total store count to approximately 69% today. International revenues now account for nearly 43% of system wide sales. In aggregate, Krispy Kreme stores are present in 21 countries outside of the United States and we believe this international presence and growth potential puts the company in a rare position within the restaurant segment. The company plans to increase the number of international shops to 900 by January 2017. This, alone, implies an increase in system wide sales of approximately +28% by January 2017. As of the end of 2Q14, total franchise commitment for international development stands at 350.

Over the past three years, the majority of the international development efforts have been in Asia and the Middle East. In FY13, new international franchise agreements have already been signed with franchisees in Moscow, India and Singapore. We will see further expansion and expect to hear about franchise efforts on new markets, including Europe and South and Central America, in the coming months.

Accelerating U.S. Growth Unit

The success of the international growth model is helping to jumpstart domestic unit growth. Over the past three years, the KKD international franchisees have pioneered the initial development of smaller, satellite shop formats and this success has been translated to the U.S. growth model.

In January, KKD opened up five of these smaller format shops in the U.S. and the results did not disappoint, as the company reported strong sales and operating performance from the shops. The company plans to move forward with these smaller unit formats and plans to open five more during the remainder of FY14. Importantly, we believe these new formats will sit well with the franchisee community and give them the confidence to incorporate these new stores into their expansion plans. In July, KKD signed a 15-store development agreement for the Dallas market, which included the sale of its three existing stores in the market. We expect to see many more arrangement similar to this, which should significantly increase the pace of U.S. store expansion.

Perhaps most impressive, the company is reporting that the 5 new, free-standing small factory shops currently in operation are seeing sales levels settling in around $30,000 a week. With an initial investment of about $590,000 per store, this indicates a sales to investment ratio of 2.6 to 1, making it one of the best in the restaurant space today.

Financial Strength

Over the past two years, KKD has generated $66 million in free cash flow and is estimated to earn an additional $31 million in FY14. Furthermore, at the end of 2Q14, the company had over $60 million in cash and practically zero debt. Combine this with the recent announcement of a $50 million stock buyback authorization and it appears as though the financial prospects of KKD are very promising.

U.S. Same-Store Sales

One of the issues we suspect will be a point of contention with some investors is the difficult same-store sales comparisons KKD will be facing.

In our view, the greatest opportunity for KKD has always been to sell more of the higher margin beverages. Over the past couple of quarters, KKD has been seeing a significant lift in transactions and a shift in the beverage mix toward coffee products. Though work is needed in order to drive more beverage sales, it appears as though the company’s strategy of connecting with the consumers through social media outlets is helping to drive sales and traffic through innovative LTOs.

Difficult sales comparisons are not new and are a known known by the investment community. That being said, we believe KKD can weather the difficult comps without hurting its strong sales momentum. 2Q14 company sales trends were strong: +12.4% in May, +9.5% in June and +8.5% in July (despite being down for a couple of weeks, as the company lapped its 75th anniversary the previous year). And, trends early in 3Q14 suggest the current momentum is continuing as same-store sales in the first week of August were up +5%, same-store sales in the second week of August were up +12% and same-store sales in third week of August were flat. We believe that 3Q14 same-stores sales growth of +4-6% is a reasonable target.

Returns Headed Higher

Currently, KKD generates some of the best returns on incremental capital in the restaurant space. The company’s current structure, coupled with the capital-light model and accelerating franchise unit development, should allow for high returns to continue well into the foreseeable future.

Equity Sentiment

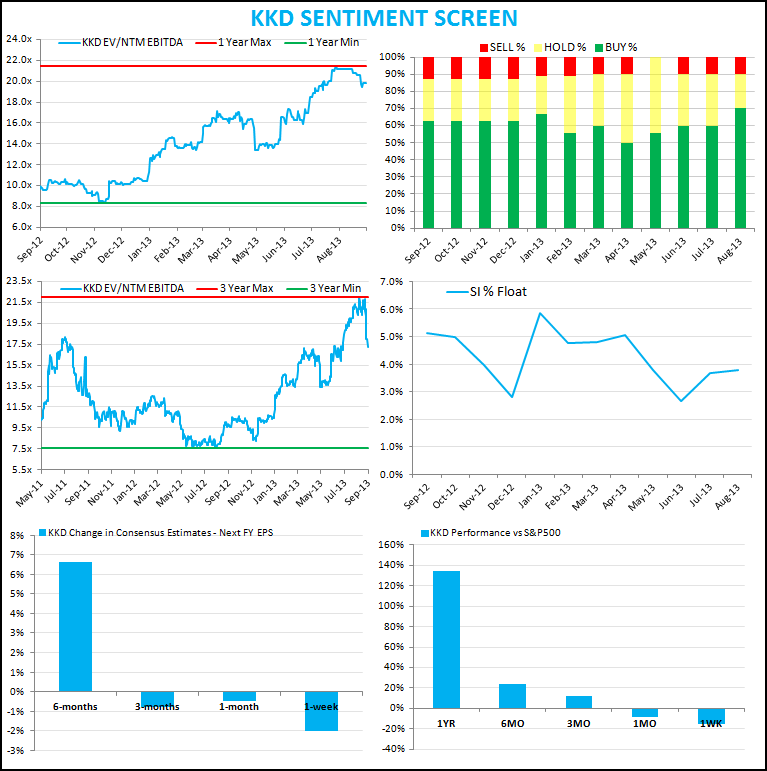

On the surface, the sentiment setup on KKD looks rather positive as 70% of the analysts covering the stock have a “Buy” rating on it and short interest only comprises 3.7% of the float. However, we would take the sentiment setup with a grain of salt, as the coverage of KKD is very limited. Only 10 analysts are currently covering the stock as opposed to 25-30 analysts covering some of the other names in the restaurant space.

Howard Penney

Managing Director