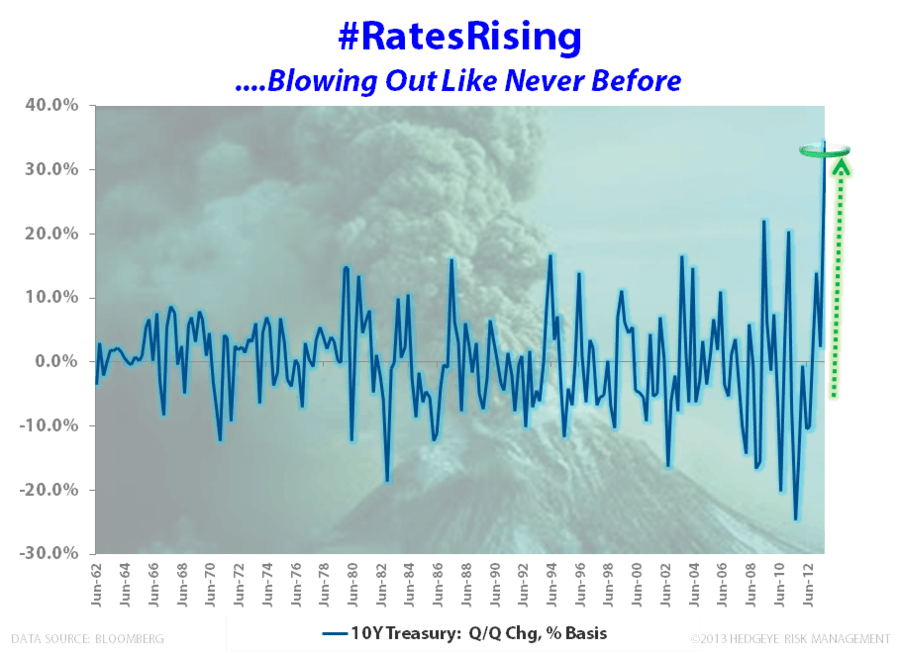

In case you were at the beach last week and missed it, we'll fill you in on the earth-shattering news: The 10-year US Treasury yield? It corrected a whopping 4 basis points.

Unreal.

For the record, the 10-year is making yet another higher-low today trading back to 2.85%. There's no resistance up to 2.93%. Our Hedgeye immediate-term risk range is 2.71-2.93%.

Yes. We are still bearish on bonds. Emphatically. It's Hedgeye's #1 Q3 Macro Theme for good reason.

Click here for information on how you can start subscribing to Hedgeye's research products.