This note was originally published at 8am on August 20, 2013 for Hedgeye subscribers.

“We were forever inventing new tricks.”

-Hans Bethe

From a strategy and teamwork perspective, one of the most fascinating aspects of reading American Prometheus (The Triumph and Tragedy of Robert Oppenheimer) has been how well these to-be-famous scientists collaborated with one another.

Hans Bethe, who eventually won the Nobel Prize in Physics in 1967, said “the intellectual experience was unforgettable.” (page 182). Since he was working alongside Oppenheimer, Feynman, and Bohr, I don’t doubt that for one second!

I’m not making a political statement on nuclear. I’m simply pointing out how a culture of trust and collaboration can incubate innovation. While the powers that be will likely never acknowledge the Global Macro models we are building here @Hedgeye, we are getting more and more respect from you, the practitioners, every day. On behalf of my team, thank you for this experience.

Back to the Global Macro Grind…

One of the most interesting realities embedded in our independent research process is that we don’t know where we are going to end up next. Our Global Macro Themes are born out of intermediate-term market signals and then contextualized by long-cycle research. If it feels like we’re forever inventing new themes, that’s because the market’s ecosystem is forever reinventing itself.

Since #RatesRising and #DebtDeflation have been the two Q313 themes most of our clients want to talk about, that’s what I have focused my time ranting about. That, however, doesn’t mean that our 3rd major Macro Theme for Q3 doesn’t exist. In fact, today is as glaring an example as any in which #AsianContagion should be jumping off your screens.

Reviewing the risks of #AsianContagion:

- Some overvalued Asian currencies are breaking down from an intermediate-term TREND perspective

- Some Asian debt markets are getting increasingly nervous about the negative deficit impact of a weakening currency

- When both a country’s currency and debt deflate, you get local inflation and local #RatesRising – that’s bad

From a process perspective, our Senior Asia analyst, Darius Dale, called out the following equity divergences 24 hours ago:

- Indonesia -5.6% DoD vs. a regional median delta of -0.2%

- Thailand -3.3% DoD vs. a regional median delta of -0.2%

- India -9.1% MoM vs. a regional median delta of -1.2%

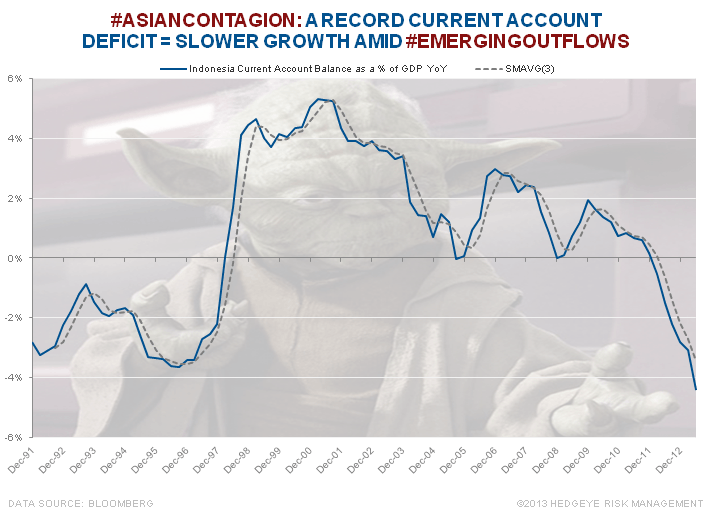

Then, on Indonesia in particular, he called out yesterday’s key economic data point:

- 2Q Current Account Balance - current account deficit widened to a record on both a nominal basis and as a % of GDP

And finally, we get this morning’s Bloomberg headlines (under Economy):

A) “Rupiah Forwards Plunge To Lowest Since 2009 As Bond Risk Surges”

B) “Rupee Drops To Record on Fed Tapering Concern”

These macro headlines (i.e. old news) come after Indian, Indonesian, and Thai markets move. The proactive risk management Macro Trick is to know they are moving (and why) before consensus realizes it. This macro theme is 1.5 months old.

Indonesian stocks are -11% in the last 3 days and India’s stock market continues to be one of the worst in the world for 2013 YTD – all for Hedgeye playbook reasoning (this kind of stuff confuses Keynesians who think weak FX is a good thing!).

Again, to review in the most simplest of complexity’s terms:

- Currency Burns, then local

- Inflation Accelerates and Growth Slows; and finally

- Deficit worries (and credit risk) rise; and bonds fall (#DebtDeflation)

If you want to be really worried about something other than the US Bond market crashing, we’d suggest Asia (ex-Japan). That’s not a new Hedgeye Jedi Macro mind trick as of this morning either. That’s what was already trending.

Our immediate-term Risk Ranges are now:

UST 10yr 2.70-2.91%

SPX 1642-1676

VIX 13.51-15.36

USD 80.91-81.96

Yen 97.11-98.26

Copper 3.25-3.39

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer