The Most Important Economic Data Series We Follow? It Remains ... Green

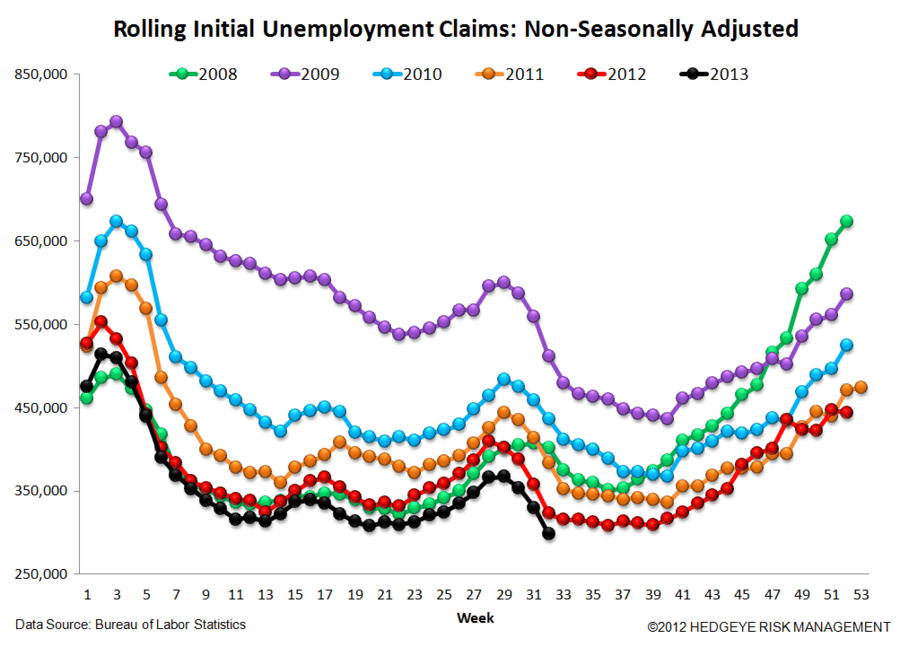

For many weeks now, Hedgeye Risk Management has been highlighting the accelerating strength in the US labor market. This week is no exception. Non seasonally adjusted (NSA) initial jobless claims were better year-over-year (YoY) by 11.2% this week, compared with 10.1% and 10.9% in the prior two weeks. Meanwhile, the 4-week rolling average NSA claims was lower YoY by 10.5%, and improvement from the prior week's 10.2%, and the second strongest rate of YoY improvement we've seen year-to-date.

The bottom line takeaway here is that the labor market is, in fact, stronger than most think and financials that are positively levered to ongoing improvement in labor conditions should continue to outperform. Moreover, given the growing shadow of uncertainty painting the recent tape, we'd look to this data series more than any other as a green light for buying weakness.

The Data

Prior to revision, initial jobless claims fell 5k to 331k from 336k week-over-week (WoW), as the prior week's number was revised up by 1k to 337k.

The headline (unrevised) number shows claims were lower by 6k WoW. Meanwhile, the 4-week rolling average of seasonally-adjusted claims rose 0.75k WoW to 331.5k.

The 4-week rolling average of NSA claims, which we consider a more accurate representation of the underlying labor market trend, was -10.5% lower YoY, which is a sequential improvement versus the previous week's YoY change of -10.2%