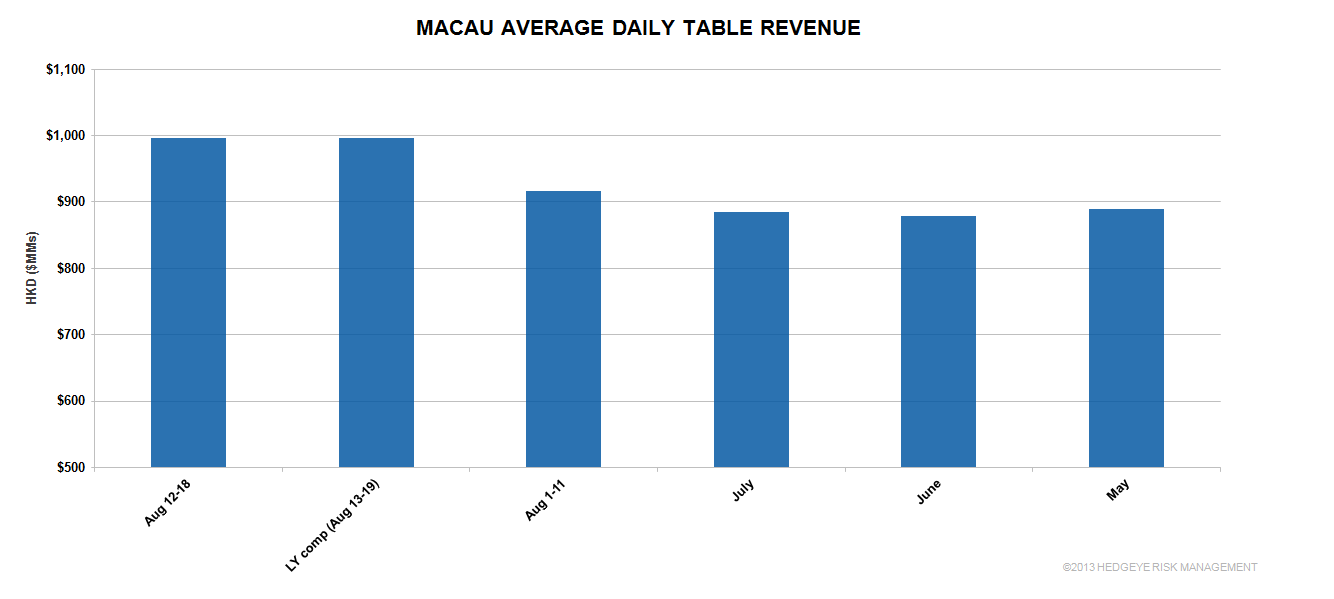

Macau posted another blockbuster week despite the typhoon that hit on Wednesday. Although we think some operators played lucky this past week, volumes were still strong. We are raising our full month projection for August to YoY growth of 16-20%, up from 14-18%. Daily table revenue averaged HK$996 million which was actually flat with last year but up 13% over July’s strong performance.

In terms of market share, LVS, MGM, and MPEL remain above trend so far in August. We like all three of those stocks.