With a good majority of consumer staples companies having reported their quarterly results, below we give a round-up of our highest conviction ideas on the long and short sides over the intermediate term TREND. As we begin sizing up company performance in the quarter, we note a few key take-away themes that are largely a continuation of last quarter:

- Investors chasing yield

- M&A speculation (more recently around PEP and MDLZ and in the wake of the HNZ acquisition)

- Declining commodity prices and expectations for improvement in gross margins

While we believe points two and three can both help fuel investor appetite, point one remains an area of concern for the broader sector given our macro team’s Q3 theme call of #RatesRising. We see the prospect of rates rising as unfavorable for the XLP (and other sectors that have been targeted for yield). During 2009-2012, the data suggested that many investors sought out staples and other dividend-yielding, stable, sectors for a steady return on investment. This would suggest that much of the capital flowing into staples may have been more focused on yield than fundamentals, which could result in that same capital exiting the group as expectations increase that the Federal Reserve tapers.

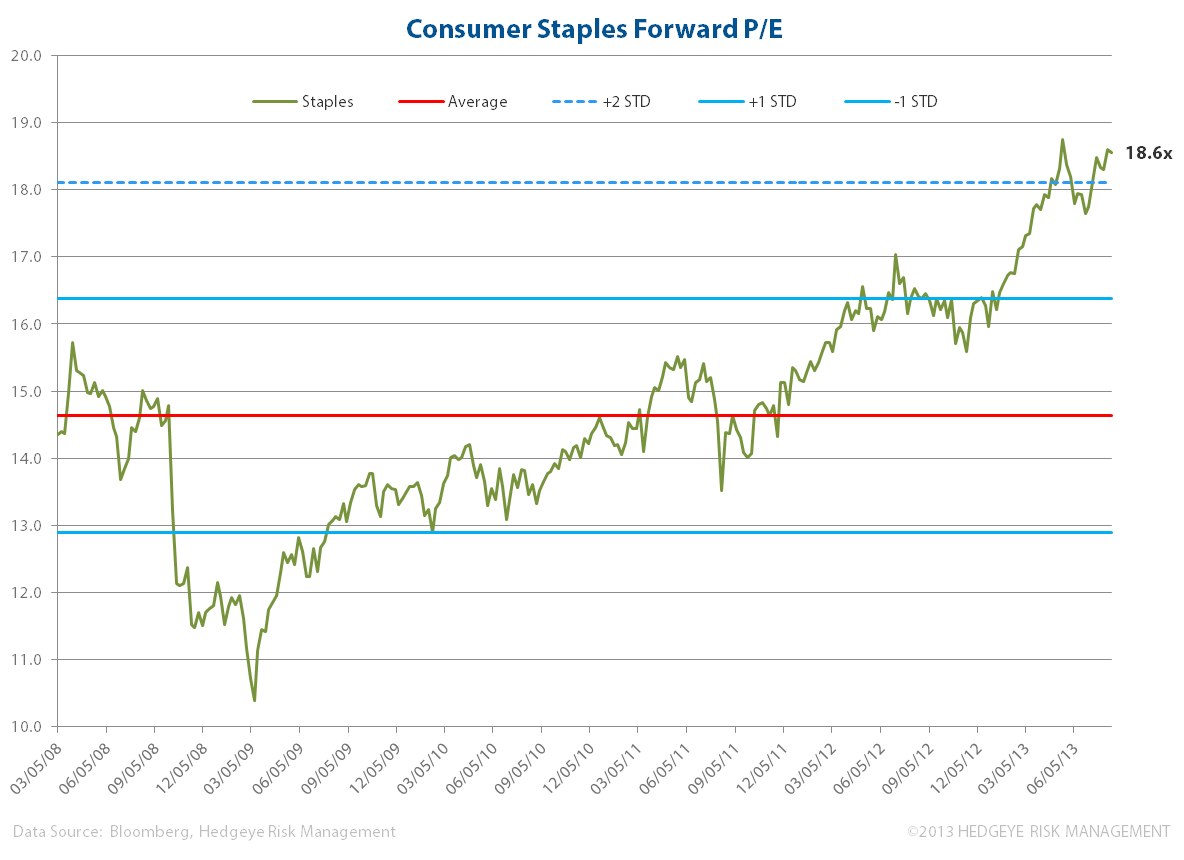

With so many factors at play, analyzing names within this space can feel like playing dodgeball. Below, we go through the names we expect to outperform, and those we expect to underperform, over the TREND duration. Valuations for the sector remain stretched but we still see some opportunities on the long side (valuation charts below, also).

Long Ideas

- LO – we expect Lorillard to continue to see outperformance on strong demand for its full-flavored offerings and dominate share of menthol, both contributing to volume outperformance versus the industry (Q2: -1.7% vs -6.1%). We think FDA rulings around menthol will be pushed out to at least the intermediate term. LO’s first-to-market (of big tobacco) e-cig Blu is enjoying top market share, which should help to boost interest in the stock given the excitement around the category.

- HSY – the company’s portfolio is benefiting from lower input costs and see strong volume gains; we expect strong merchandizing around Halloween and the holidays to further benefit 2H results. The fruits of the Brookside acquisition should continue to pay dividends (expected to contribute 1 pt of growth in 2013).

- TSN – consumers preferring the value of chicken versus other proteins is a dynamic we expect to continue in 2H. The company has been able to pass on or well manage input costs given its diversity in protein offerings and geographic exposures. Protein over carbs remains an import component of health and wellness trends that TSN has at its back.

- SAM – the maker of Boston Lager had surprisingly strong Q2 results and wet investor’s pallets with news that given excessive demand and capacity constraints, the company is increasing its cap-ex guidance to expanding its brewery production. Despite the craft category growing ever more competitive, we like SAM’s positioning in the market and management’s ability to profit from an establish brand as it mixes in new tea and cider offerings.

Short Ideas

- PM – we expect continued FX headwinds given our #StrongDollar call. PM revised down its FY guidance as it forecasts larger volume declines in the year across its geographies, including due to increased excise tax headwinds in key geographies like Russia and the Philippines, and an uptick in illicit trade in Turkey.

- DPS – the company’s portfolio is ~ 80% carbonated soft drinks (CSD), a category that continues to be challenged as consumers switch to both healthier carbonated and non-carbonated offerings. The company is hopeful around the launch of its 10 calorie DP 10 offering, but we do not expect it to offset the declines across the portfolio.

- CCE – on-going macro weakness in Europe and the continued impact of the French excise tax, along with competitive pressures, have hampered the company’s results. We do not expect to see an inflection in weak trends as we’re forecasting at best only slow and modest economic improvement in Europe.

- K –Kellogg reduced its FY guidance on increased FX headwinds and its results reflect weakness in key categories and geographies that we expect to persist in 2H. The U.S. business remains particularly challenged, especially in cereal. K needs to realign its marketing spend and innovation, which may take at least a couple of quarters to turn around.

- KMB – Kimberly Clark reported disappointing earnings in July and has underperformed since then. FX and competitive pressures will continue to weigh on earnings growth as inflation sequentially accelerates. We see downside risk to the company’s FY13 estimates, with personal care volumes in the U.S. and other developed markets particularly concerning for shareholders.

Our quantitative real-time set-up for consumer staples (etf: XLP) is bullish, trading above its intermediate term TREND line.

-Rory Green and Matt Hedrick