This note was originally published July 17, 2013 at 15:36 in Healthcare

NEAR-TERM FORECAST: GROWTH ACCELERATING 2Q13/3Q13

We recently updated our birth regression model for 2Q13 and 3Q13. Our model continues to call for accelerating growth in the near-term given the trajectory of the underlying factors that drive our model. Below we discuss the drivers of that forecast as well as recent developments related to our thesis

- Women’s employment (20-34 YOA) ACCELERATING: One of our better leading indicators. Growth has accelerated through most of 2012 and suggests accelerating growth through 3Q13

- PKI Human Health Organic Growth ACCELERATING: Product portfolio focuses primarily prenatal and neonatal testing, and has been a strong lead for US Births. Calling for continued growth through 2Q13.

- Household Formation NEUTRAL: Complements of our Financials Team, has been a good coincident read on birth trends. Although improving sequentially in 2Q13, the 2-yr average (the better read) calls for a slowdown in 2Q13

- Home Prices ACCELERATING: The implication here is rising prices are a signal for growing demand for housing. Has been a surprisingly strong read into US Births. Current trajectory suggests improvement into 2Q13

- DEST 2Q13 SS Sales ACCELERATING: Decent overlay with US Births. Preannounced accelerating SS sales growth for 2Q13 (the highest the company has seen since 2006), suggesting accelerating growth for 2Q13

- HCA/THC 2Q13 Admission Trends NEUTRAL/ACCELERATING: Both companies SS admissions trends are pointing to steady to moderately improving trends in 2Q13. Note US births represent 25% of hospital inpatient volumes

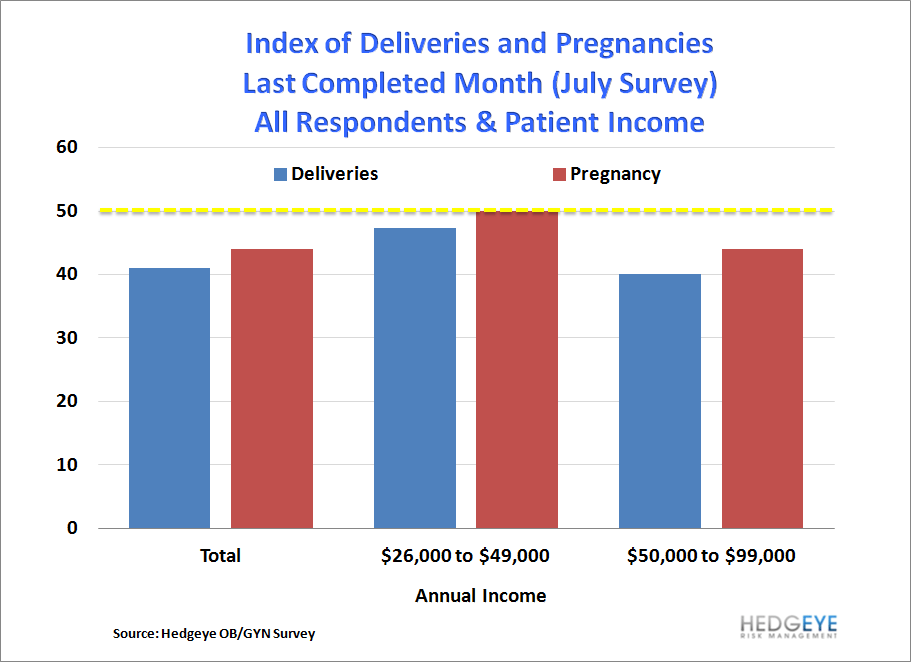

- Hedgeye OB/GYN Survey (July 2013) DECLINING: Our survey asked respondents about the y/y trend in June, which we created an index off of (base 50). The data suggests both births and pregnancies declined in June. We will be running the survey again in August.

- CSFB Survey NEUTRAL: Anecdotal callout from a competitor’s survey, suggests births were flat y/y in 2Q13.

INTERMEDIATE FORECAST: GROWTH SPUTTERING 4Q13/1Q14

We do not have as strong a read longer-terms since many of the macro factors we track are coincident indicators. Our two longer-term reads our Women’s Employment and PKI Human Health, which point to slowing, potentially negative trend in 4Q13/1Q13

- Women’s employment (20-34 YOA) DECELERATING: Suggests a moderating, but positive trend for births into 4Q13/1Q14

- PKI Human Health Organic Growth DECELERATING: Suggests moderating, if not negative, growth in 3Q13/4Q14. We do note the that 1Q13 results for PKI may be negatively skewed due to externalities (working days/weather)

LONGER-TERM FORECAST: RECOVERY THESIS INTACT

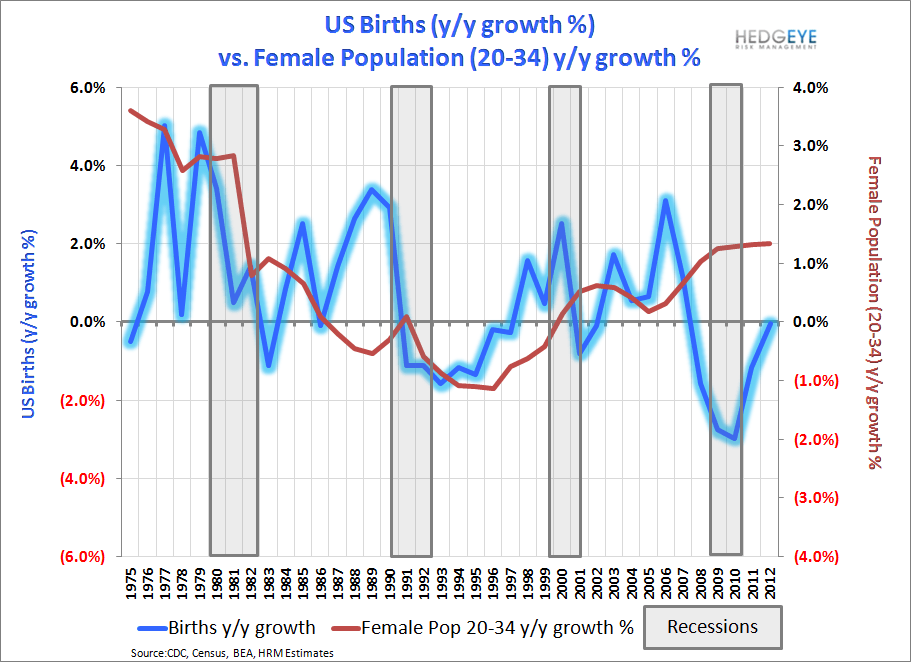

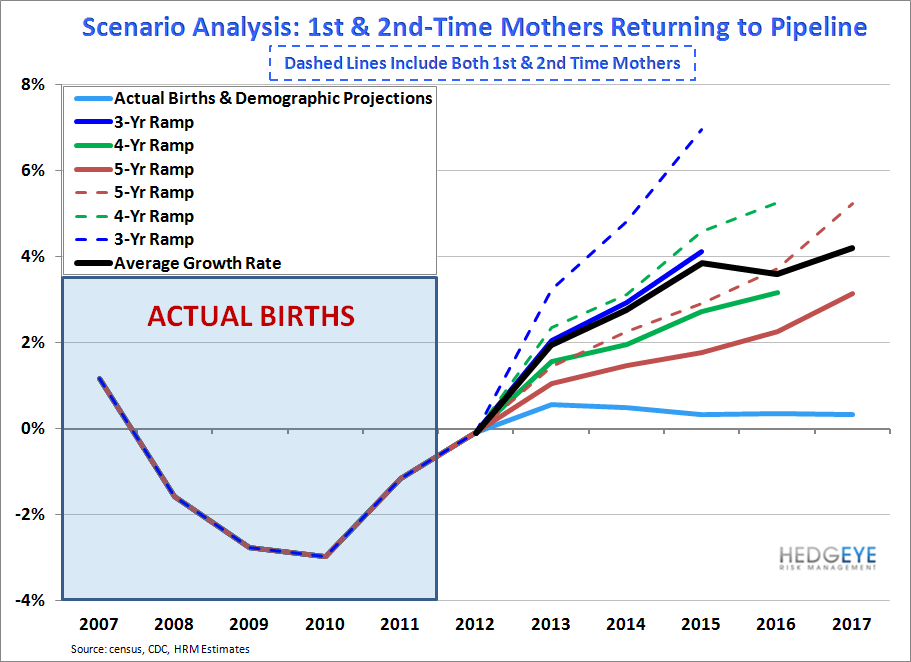

One of the major tenets of our forecast is what we refer to as the Deferred Birth Opportunity, which is the number of pregnancies/births that were delayed for economic reasons because of the Great Recession. Note that the size of primary birth demographic (women aged 20-34) was not only growing, but experienced accelerating growth from 2007-2012, alongside a cumulative decline of 9% in US Births during that period.

Ultimately we see some percentage of that Deferred Birth Opportunity coming back into the system; particularly among first-time mothers, which annually represent 40% of US Births. We estimate that between 1.0 and 1.5 million births have been deferred during the Great Recession. Given the currently deflated base of US births (2012 was lowest annual nubmer since 2000), the growth potential could be significant.

Charts below. Feel free to contact us for more detail, underlying data, or with questions.

Thomas W. Tobin

203-562-6500

@HedgeyeHC

Hesham Shaaban, CFA

203-562-6500