Conclusion: Credit trends continue to strengthen as employment, loan demand, and credit availability all continue to improve, household financial obligation ratio’s remain troughed, and household net worth makes new nominal highs. Employment, credit and confidence are key macro factor ingredients for perpetuating a positive, self-reinforcing economic upswing, and trends across all three metrics remain positive.

-----------------------------------------------------------------------------------------------------

According to the latest Fed data, total U.S credit market debt totals ~$57T dollars. The total Monetary Base (currency + reserves) meanwhile sits at ~$3.2T. So, at present, there is ~17.8X more obligations to pay dollars than there are actual dollars - Fancy that, Credit Matters.

Generally, credit is pro-cyclical with banks loosening standards and extending credit in response to rising demand and improved credit risk. The reason for the pro-cyclicality is rather straightforward - Household capacity for credit increases as incomes rise alongside positive employment growth and as net wealth rises alongside the rise in real and financial assets that typically accompanies an expansionary economic phase.

Thus, cash flows to service debt and the collateral values backing the debt both support incremental capacity for credit and serve to drive an upswing in the credit cycle, which can serve to jumpstart and/or amplify the economic cycle.

The Fed’s release of its 3Q13 Senior Loan Officer Survey this morning reflects further strengthening in both Loan Demand and Credit Availability. A review of the 3Q13 Loan Officer Survey data below along with a quick tour of household debt and balance sheet trends.

3Q13 Senior Loan Officer Survey: Rising Demand, Loan Spreads & Credit Standard Easing Steady

Stronger:

- Stronger Demand for Prime, Nontraditional, and Subprime Residential real estate loans

- Stronger Demand for Auto and Consumer loans excluding Credit Cards and Autos.

- Stronger Demand for Commercial Real Estate loans

- Stronger Demand for C&I loans from both large & Small Firms. Notably, the net percentage of bank reporting stronger demand for C&I loans from small firms went jumped from 7.7% in 2Q13 to 24.3% in 3Q13.

- Lower Standards on Auto loans

Weaker:

- The net percentage of banks reporting easing credit standards remained positive but cooled (modestly) sequentially across C&I, Commercial Real Estate Loans, and Credit Card Loans.

CREDIT FLOW: The idea of the Credit Impulse, popularized by Biggs, Meyer & Pick (2010), centers on the idea that it’s the flow, not the stock, of credit that matters relative to economic growth. The implication is that if the change in net new credit is positive, credit can still support demand even if the nominal stock of total debt is still declining, and vice versa.

The first chart below illustrates the Credit Impulse (Household and Non-Financial Corporate Debt, Flow of Funds data) vs. the Y/Y change in consumer and business demand (represented by the y/y change for the Consumption and Investment components of GDP) along with the Y/Y change in total household and Non-financial corporate debt. As can be seen, the trend in private sector demand growth tracks the credit impulse closely and leads the positive inflection in y/y debt growth.

The second chart shows the Credit impulse vs. the ‘Banks Willingness to Lend’ measure from the Senior Loan Officer Survey. Again, the Trend relationship is strong and with Willingness to Lend accelerating in 3Q13 the read through for credit catalyzed private consumption remains favorable

We’ll get the updated Flow of Funds data from the Fed on Sept 25th.

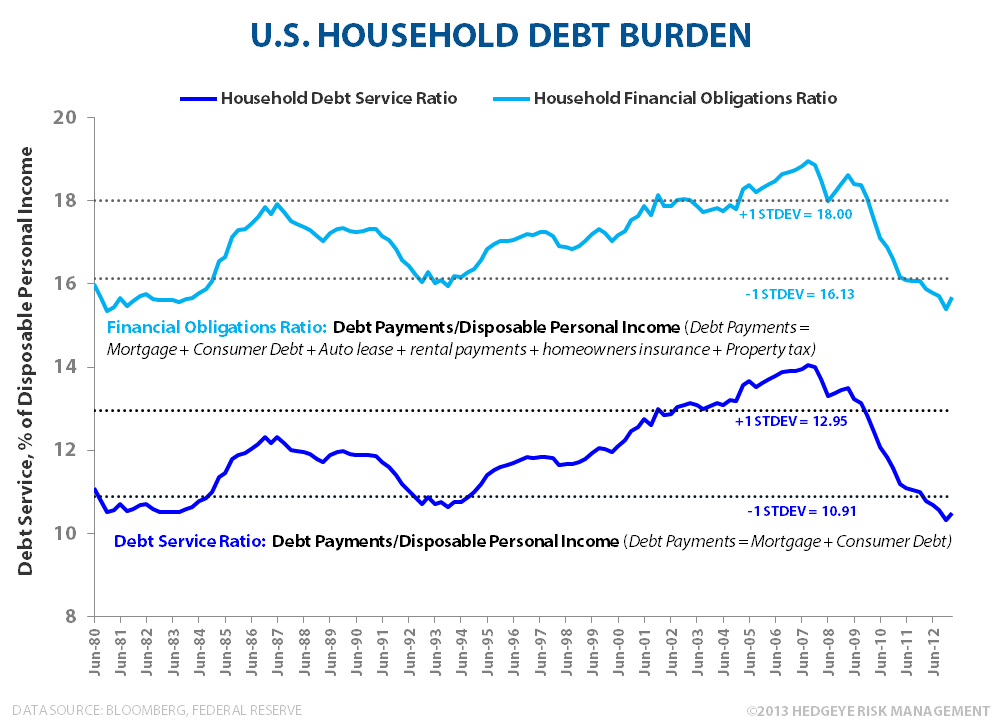

Household Debt-to-GDP & Debt Service: Household Debt/GDP continues to fall as nominal debt declines alongside ongoing, albeit modest, GDP growth. At 77.4%, we’re currently 16.9% off peak 2009 Debt/GDP levels and have nearly retraced back to (1) trend. Financial obligation ratio’s remain just north of trough levels due to the combination of organic deleveraging, low interest rates, and nominal earnings growth.

Debt Growth vs. Income Growth: Debt growth in excess of income growth is (obviously) unsustainable with a long-term credit cycle ultimately ending with a 2008 style deleveraging. In the wake of the financial crisis and through to the present, income growth has run at a positive spread to debt growth.

Debt growth has already inflected and given positive mortgage, auto, and consumer loan trends YTD is likely to turn positive when 2Q13 is officially reported. The closing of the delta between income and debt growth represent the upside to credit driven consumption.

Household Net Wealth: Household net wealth is +5.2% above the prior 2007 peak on a nominal basis, -4.2% on a inflation adjusted basis, and -7.6% when adjusted for both inflation and the number of households. Reported net wealth should continue to recover/advance alongside strong, ongoing home price growth and higher equity market highs. Asset/Collateral inflation and a strengthening in the household balance sheet will support capacity for incremental credit and should serve to drive some measure of wealth effect spending.

Christian B. Drake

Senior Analyst