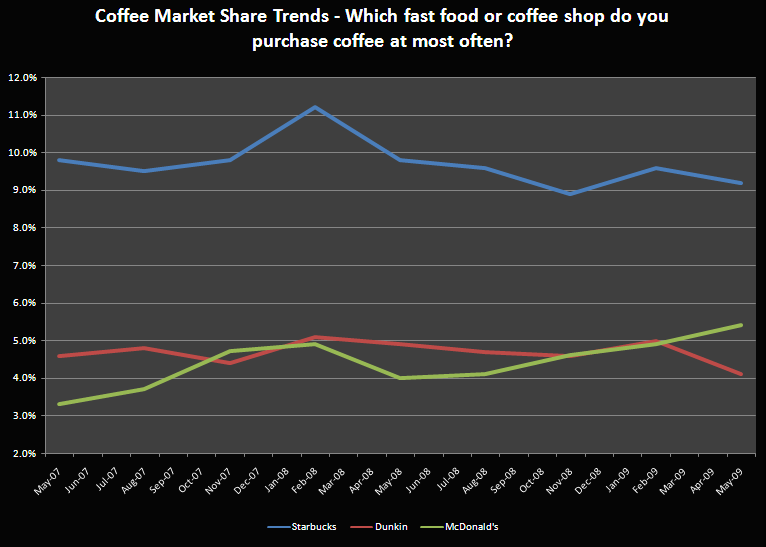

Big Research is a consumer centric research firm that does very detailed survey work in multiple retail categories. In the May survey of 6,000 consumers, they asked- which Fast Food Restaurant or Coffee Shop do you purchase COFFEE at most often?

The most recent coffee survey shows McDonald's gaining ground on both Starbucks and Dunkin Donuts. Although Starbucks is still #1 - 9.2% of consumers frequent the Starbucks most often for their coffee needs. The survey shows that McDonald's is taking more market share from Dunkin Donuts.

McDonald's market share has consistently grown since May of 2007, according the BIGresearch's May 2009 Consumer Intentions & Actions (CIA) Survey. With McDonald's spending upward of $100 million on its coffee campaign, it's likely that the momentum will continue.

According to the analysis, McDonald's coffee drinkers (those who purchase coffee most often from McDonald's) tend to be older than Starbucks drinkers with an average age of 47.7 vs. 39.2 for Starbucks drinkers. Also, 46.8% of Starbucks drinkers are in the 18-34 age range, compared to 25.8% for McDonald's.

More Starbucks coffee drinkers are single at 29.1% vs. 19% of McDonald's drinkers and a higher percentage hold professional/managerial jobs - 27.2% vs.15.7%. Starbucks customers are also more affluent with annual income of $67,487 vs. $55,572 for McDonald's.

Other Thoughts:

• 33.7% of McDonald's coffee drinkers are confident/very confident in the economy, vs. 30.3% of Starbucks drinkers.

• 72.7% of McDonald's drinkers are focusing more on needs over wants, vs. 65.7% of Starbucks drinkers.

• 44.2% of McDonald's drinkers are buying more store brand/generics vs. 36.2% of Starbucks drinkers.

• 26.4% of McDonald's drinkers feel better about their economic situation, vs. 34.4% of Starbucks drinkers.

• 20.8% of McDonald's drinkers are starting to spend more on discretionary items, vs. 21.4% of Starbucks drinkers.