Church and Dwight reported 2Q13 EPS of $0.61 versus $0.60 consensus. Top-line growth was underwhelming, with organic growth coming in at 3.2% but segment results were mixed with weather and variable consumer demand impacting performance.

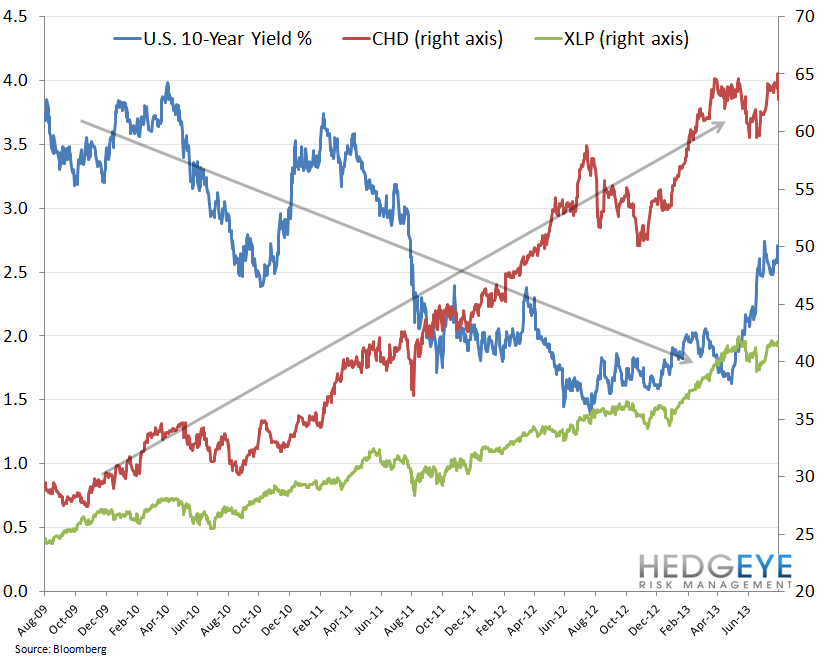

#RatesRising Pressuring Staples: If we accept the premise that rising rates are negative for the XLP, it follows that such an outcome will likely pressure CHD’s stock price. Over the past four years, CHD and the U.S. 10-Year Yield have a negative correlation of -0.8. As rates rise, we expect that to pressure XLP versus other sectors and CHD, given its premium multiple, could continue to underperform versus its peers. As the table below illustrates, CHD has outperformed its peers over the past three years but has lagged over the past three months.

Guide-Down: Management guided to 2% full-year organic sales from a previous range of 3-4% due to competitive pressure pushing the company to lower price/mix and weak results in the Specialty Products segment (6% of consolidated revenue). Productivity initiatives are sustaining gross margin expansion, which is a positive, but earnings guidance for 3Q of $0.73 falls short of consensus $0.75.

Management struck a decidedly cautious tone during the conference call, highlighting the fact that five of the company’s fourteen categories saw declining year-over-year sales while an additional five saw growth of less than 2%.

What we liked:

- EPS beat expectations

- Gross margin expanded 110 basis points unaided by commodity prices; gains were driven by productivity programs and sales growth

- Operating income growth came in at 17.8% versus sales growth of 13.1%

- Value brands (40% of revenue) continuing to appeal to price-conscious consumers

- Growth potential of Avid business

What we didn’t like:

- Lowering organic growth guidance

- Consensus expectations above guidance for 3Q

- Management’s commentary on more difficult operating environment

Rory Green

Senior Analyst