We wouldn't chase JNY on the 'exploring strategic options' announcement.

This story does not have the guts to become FNP Part II. There are a lot of skeletons in this closet. While there could be some upside with a deal, it's not enough for us on a risk-adjusted basis.

- In part, a transaction is already priced in. We started to field 'activist-related' questions when the stock was about $12 in Feb and March. The financial press reported on Barrington Capital's activist intentions on April 12th of this year, by which point the stock hit $14. Over the past three months, the stock is up by 33%, or about $300mm in market value. That's not to say that it can't go higher, but simply that the M&A mill has already created some value.

- Valuing JNY is no easy task, but the way we look at the world, the current price is already reasonable for what you get. Some might argue that the margins are artificially low at 5%, but the reality is that they're really not. This company has perennially bled its good content of growth capital to acquire future top line growth. In fact, when you go through the arduous exercise of separating the acquired growth from the declining core, you see that the company's sales base is the same place today as it was a decade ago. If we're right in that the company is not underearning, then 8x EBITDA sounds about right. As a check, that comes out to about 0.5-0.6x sales…a $250mm price tag on Juicy Coture (the rumored price tag, which we think sounds about right) equates to 0.5x sales.

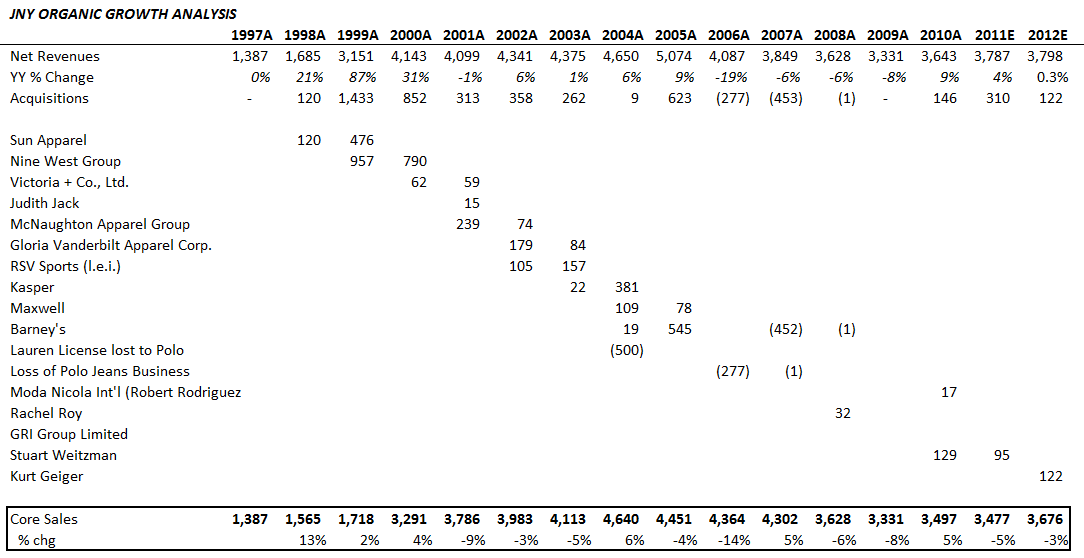

- For those who say that the loss of the Lauren and Polo Jeans business back to RL in 2005 and 2007 -- which accounted for about $775mm in revenue -- masks the organic growth in the the underlying business -- we'd simply ask the question "why did RL take back the businesses in the first place?" It's because JNY was grossly underperforming in its contractual obligation to drive that business forward. That's all water under the bridge, and was during a different JNY CEO's tenure. But, it shows our point that JNY does not have the culture of reinvesting in brands. That's why the RL situation was one of the only incidents of a license breach in recent memory, and that's also why the portfolio of brands JNY has today is simply 'Average' and not easily fixable.

- Where could we be wrong? We could be missing the boat if it turns out that the two crown jewels -- Jones New York and Nine West, fetch a far better price than we're modeling. Each of the brands is in the vicinity of $1bn -- accounting for a little more than 25% of JNY's revenue. While we still think that both brands have margin problems that will require capital to fix (ie margins need to go down before they can go up) the reality is that with the right management they are definitely worth something. We could justify ultimate earnings power of $200-$250mm in EBIT from the combo if all goes right, which at $16 suggests that you get the other brands for free. While that sounds like the kind of story we'd ordinarily be drawn towards, the reality is that we think there's a lot of skeletons in this closet. We need to be eyeing massive upside (ie at least a double) to get really excited. We're not there. In addition, if no transaction happens, you're left holding the bag with a really bad investment at $16.