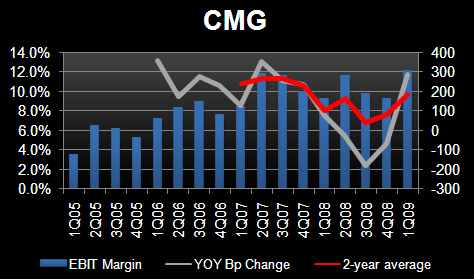

Chipotle, like every restaurant company is currently "over earning" which is not a bad thing, just a function of the times. By "over earning" I mean the rate of pricing running through the P&L is far out stripping the rate of inflation the company is seeing, so margins are exploding. For CMG this will continue for at least one to two more quarters, depending on traffic trends and how the new menu initiatives perform.

Given how young the Chipotle concept is, there is not a lot of history to understand how consumers will view the concept in a recession. Fortunately, senior management has bought themselves some time and margin to adjust to the new reality; consumers are not flocking to the concept as they once did on the past.

In 2007, Chipotle was enjoying rapid growth with little or no advertising expense. Much of the growth was driven by word of mouth and CEO Steven Ells justified the scant spending on advertising in March 2007, saying, "Advertising is not believable." Fast forward to today and Chipotle's traffic was down 4.5% in 1Q09 and the company is launching its first advertising campaign.

Ells and his team have come up with mychipotle.com as a centerpiece for an advertising campaign seeking to bring the credibility of word of mouth promotion to a wider range of people. The aim is to get more people into Chipotle. I'm sure we will hear how successful mychipotle.com site is, but I'm skeptical that it will translate into increased traffic.

While I have no doubt that social media advertising is powerful and could possibly benefit CMG in the future, value is a key theme today. Clearly, the concepts declining traffic trends are down partly in response to the 8.5% price increase implemented last year. In the short run, the menu price increase certainly helped margins, but may create some difficulties should traffic not pick up significantly in 2010.

By the time we reach 2010, the Chipotle concept will have little or no pricing flexibility and at some point variable costs and lower price points on the menu will impact margin. At the same time, the company will have opened over 250 stores at lower margins or 25% of the store base. There will continue to be a "portfolio" impact on the overall margin structure of the company.

The following are some of the key issues the company faces. CMG clearly has a number of significant issues to overcome, but nothing is terminal. The comparisons in 2Q09 are difficult, but the "over earning" status suggests that it might not be that difficult to compare against. In this scenario, the 19% short interest is a bullish signal.

MENU CHANGES

By design the Chipotle menu is simple and easy to execute as it displays the individual ingredients, and leaves it up to the customer to mix and match. The company research suggests that this design leads to a perception of limited variety and discourages experimentation. More to the point, the concepts price points are not flexible enough to provide choices for families with kids. In order to broaden the appeal of the concept, the company is testing a new menu that includes new entree options, several featured items, new, smaller, lower priced options, and a complete kid's menu. Without a broad based communication strategy to communicate the menu changes and drive incremental customer traffic, the risk that the concept sees a lower average check from current customers is high.

Can they introduce value and maintain margins; that thought is inconsistent in the restaurant industry!

MARKETING

Chipotle new marketing campaign is called My Chipotle and is designed to engage directly with Chipotle's current customer base. The idea is build on the traditional word-of-mouth strategy. The new campaign will be using radio, print, outdoor and a website called mychipotle.com. The intent is for the concepts customer to become part of the ongoing My Chipotle advertising campaign. The new strategy appears to be directed at the concepts existing heavy users and not drawing in new customers.

As a percentage of sales, Chipotle spent 2.2% in 1Q08, 2.5% in 2Q08, 1% in 3Q08 and 0.7% in 4Q08. In. Overall for 2008, CMG spent 1.75% of sales on marketing. In 2009, advertising should remain at 1.75%, with 1Q09 spending 2009 at 1%, advertising is expected to accelerate for the balance of 2009 putting pressure on margins in 2H09.

SAME STORE SALES

Chipotle took a very aggressive approach to pricing in 2H08 and given the decline in overall restaurant traffic, it's hard to quantify how much of the decline in traffic is in response to higher prices. In 2009, the price increases taken last year will result in an effective increase of about 6% for the full year with effective pricing of around 6% for 2Q09 and 3Q09 and less than 3% in 4Q09. Currently, guidance is for same-store sales to be in the low single digits for 2009. In 2Q09, CMG will lose a day as a result of being closed on Easter and it will lap a 2% menu price increased from last year.

A critical issue going forward will be management expectations for its new marketing initiatives and the impact on traffic. I would not be surprised to see management be overly optimistic about the potential impact for the increase in customer counts. It's unlikely to see a significant improvement in same-store sales from current levels.

NEW STORES/LOWER RETURNS - A RESTAURANT INDUSTRY CLASSIC!

This is where one of my biggest concerns lies when looking at CMG. I don't know one restaurant company that has been able to overcome the "portfolio impact" on margins and returns from opening stores with lower average unit volumes.

Total capital expenditures in 2008 were $152 million; declining to $140 million in 2009, of which $120 million relates to the construction of new stores. In 2008, CMG spent, on average, $916,000 to build a new store - up from $880,000 in 2007. This is due to opening a larger portion of the restaurants in urban locations being partially offset by a decline in the percentage of free-standing restaurant openings and smaller square foot per store. In 2009, development costs are expected to remain the same as 2008.

Here is the problem; CMG new growth is coming from building new stores with lower average unit volumes that cost more to build! This trend will not reverse as they have built out all the best return sites. Also weighing on future performance is the company ability to pick only A/B sites; right now there is room for error in site selection.

Going forward, incremental growth provides a diminishing return. Over time while the company may be able to grow total EPS, but the multiple on the EPS will contract providing very little upside to the stock price.

Another classic pattern will be for the investment community singularly focused on the performance of the existing store base relative to the new stores being opened. The company reported its first decline in system-wide AUVs in 1Q09 as more new stores are annualizing at $1.35 million to $1.4 million are brought into the comp base. Currently the system average is about $1.7 million. In 1Q09 I calculate new store average unit volumes at $1.26 million versus $1.40 million in 1Q08, down 10%. This compares to management stated number of $1.350 million to $1.4 million. I know that the new store performance is not a new issue, but it's one that should not be over looked.

Over the past year CMG has been opening lower volume stores; as a result, the company's return on incremental invested capital has declined from 26% in March 2008 to 17% in 1Q09. While this metric has improved from the low of 12% in 4Q09 the trend will decline given the company current strategy.

Toward the end of 2009, I would not be surprised to see the company accelerate unit development in an effort to maintain a growth multiple!