Summary

We’ll let others summarize the FDX quarter and will instead focus on the development of key value drivers. For us, the one factor that matters most is the Express margin. FDX needed to “show” Express margin progress and the company delivered. That should be a positive set-up heading into the core of the FDX’s restructuring in FY14 and FY15. We see further evidence in the quarter that FDX will execute on its plan to improve Express margins, likely taking the share price significantly higher. We will also be looking for the 10-Q, which should be out tomorrow.

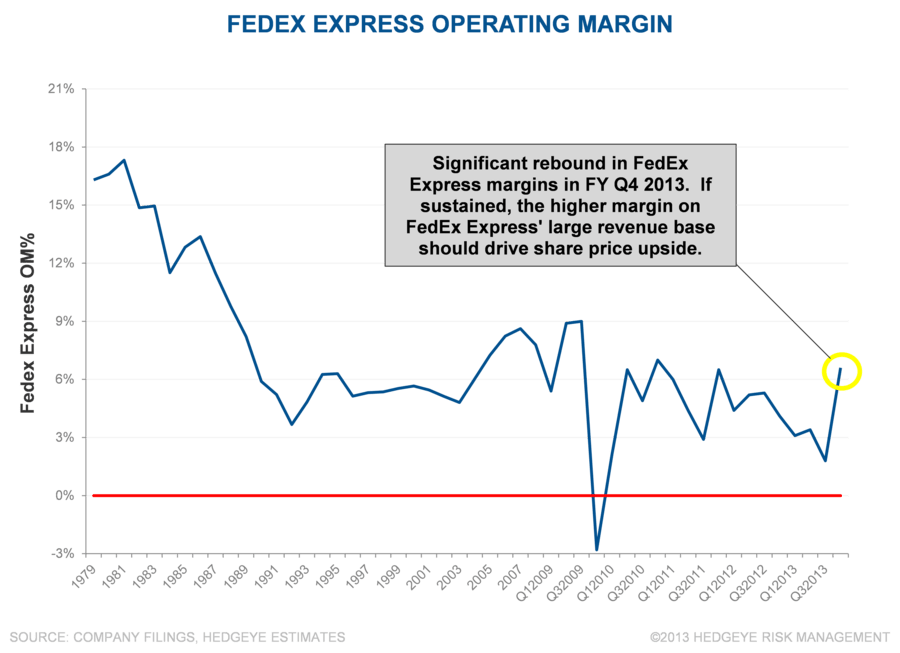

Express Operating Margin Strong: FedEx Express is not dead yet. Instead, it is improving margins and growing total volume (IP+IE, Domestic). Capacity reductions, a younger fleet and, perhaps most importantly, the use of commercial lift for International Economy volume drove the highest quarterly segment margin since the tight market of FY4Q 2010. Importantly, the margin gain was from what some pejoratively refer to as “self-help”, not a strong Express environment. Management's tone when discussing International Economy (IE) vs. International Priority (IP) seemed clearer and more positive than it had previously.

Why Did Express Margins Expand Now? This is the first quarter we expected to see any benefit Express restructuring because this is the first quarter since the restructuring is in place (see “Clock Starts Now”). The early results are encouraging and there should be more to come.

$8.00 In FY14 EPS? Given the strong FY4Q 2013 Express margin and the further improvements expected in FY14, a 6% Express margin for next year is not unrealistic. FedEx Ground reported strong growth and margins, putting >$2 billion in operating income within reach. Assuming another decent year for Freight, it is not a big stretch to model FY2014 adjusted EPS at just under $8.00/share.

Why was guidance so weak? It seems pretty obvious that management sandbagged guidance, refusing even to elaborate on it in Q&A. Even though management claimed that they did not play the conservative guidance game, we do not precisely believe them. In a long-term restructuring, it is much more attractive to progressively raise guidance than to cut/raise/cut/raise the way a true 50/50 guidance expectation could force them to. Besides, the guided EPS growth barely accounts for the improved pension expense next year, let alone the profit improvement demonstrated in the quarter and expected in the restructuring.

Capacity & Capital Spending: Some may have been disappointed by the higher than expected capital spending number. Our opinion is that the faster FDX gets rid of old aircraft, the better. If they were adding capacity to grab market share, we would worry. Instead, the capital spending is being directed at replacing high cost, out of date aircraft. In the international express market, International Economy should increasingly be handled through the asset light FedEx Trade Networks (FTN).

“We are not buying any airplane capacity for growth. The airplanes that we are buying are for replacement. We're replacing the 727s and, as Alan mentioned, the last one flies Friday, with 757s, ditto the A310s. The 767s start coming in, in September and those are very high ROIC activities with the existing volumes. It's not growth at all, and the 777s are replacing the MD-11s over the next 10 years and I think we've got 18 more of them on order over the 10 years. So, there is no capital in airplanes. We're not putting capital in the business for growth. We're simply replacing the assets that we have.” – Fredrick W. Smith

Express Margin Gains May Slow From Here: FedEx Express finally moved to fix the capacity/international mix issue this quarter with a sizeable initial benefit. That pace of margin expansion may be difficult to duplicate and we expect more of a lumpy/seasonal grind higher from here. The moving of the Investors and Lenders meeting out a year may suggest that there is less incremental news coming and more focus on delivering what the company has already outlined.

“I'd say the one thing that we're a bit disappointed on, we probably should have moved a bit faster on some of our capacity because we thought that the mix would be a little bit different than it ended up, but it's like Ground and Express, we're happy to get either one and we just have to manage properly within those segment demands from the customers.” – Fredrick W. Smith

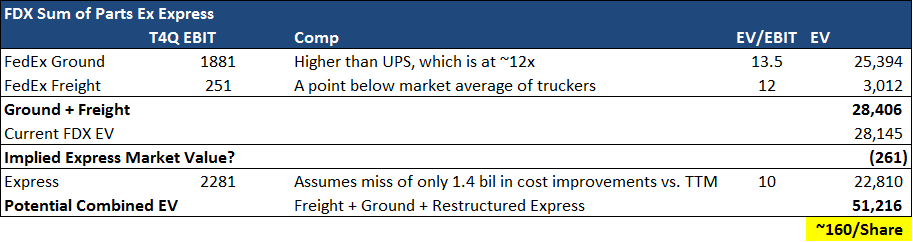

Significant Upside: Although we do not usually like sum of the parts valuations for a number of reasons, the one below helps illustrates the kind of much upside available if FDX is able to execute on its plan to expand margins. We continue to believe that FDX represents one of the best longer-term opportunities in the Industrials sector.