This note was originally published June 07, 2013 at 16:20 in Consumer Staples

Our Consumer Staples team has been touting Dean Foods (DF) for the past couple of months and although the stock has moved, we believe there remains significant value and upside in the name. Before getting into an updated valuation analysis, we wanted to tell you why we like this business (especially at 5x firm value / 2013E EBITDA).

We think DF is a compelling business for the following reasons:

- National scale – DF is the largest processor and distributor of fluid milk in the United States at more than 5x the size of its nearest competitor. As such, it is a natural and synergistic acquirer of smaller competitors, especially given its ample free cash flow and low debt load.

- Market share within the market – In 80% of its IRI defined geographies, DF has the #1 or #2 market share of branded milk. This dominant market share will make it difficult for a competitor to compete on price, since DF typically has a volume advantage. (DF national market share has been stable and ranged between 37.5% and 38.2% for the last nine quarters ending in Q1 2013.)

- Strong management – We could drill deeper into this topic, but this is a management team that has shown an ability to execute, as evidenced most recently by the successful spin-off of WhiteWave and monetization of Morningstar. As well, management has met or exceeded expectations for the last nine quarters. This was also in a period in which they reduced operating costs by $53MM, or ~9%, from Q1 2011 -> Q1 2013.

That all said, DF is still a commodity company, even if a branded one, so we do need to consider that fact when evaluating the business along with the highlights above. In our view, the current valuation provides substantial downside protection and fully accounts for the commodity nature of the business.

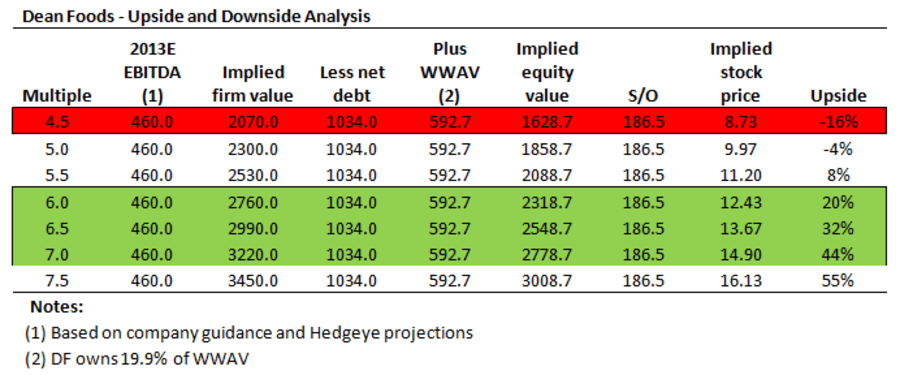

In the table below, we provide an upside / downside analysis based on 2013E EBITDA and multiples of enterprise value / EBITDA. Currently, we think the stock is at a price in which the risk / reward is compelling. On the downside, absent a dramatic change in the milk market or poor management execution (unlikely), we think the reasonable downside is 4.5x EBITDA, or ~16% from current levels.

In terms of the upside, as noted we do acknowledge that this is a commodity company with only modest top line growth rates, but we do believe given the compelling business characteristics and high free cash flow yield reasonably justify a multiple in the 6.5X – 7.0x EBITDA range, which implies 32% - 44% upside from current levels. From our perspective, a situation in which there is 2:1 upside / downside with fundamentals trending our way is a compelling investment.

The argument for the upper end of the multiple range of course is based on the generous free cash flow nature of this business. While 2013 is a bit of an odd year given the corporate activity (notably the spin-off of WWAV), we believe that on a normalized basis DF will generate in the range of $140 - 150 million of free cash flow to the equity annually. This implies a rough 8% free cash flow yield. In combination, a 8% free cash flow yield and a debt-to-EBITDA ratio of just over 2x makes this a compelling LBO candidate. (Moreover, the debt-to-EBITDA is closer to 1x if we net out the WWAV stake.)

In addition, DF’s publicly traded debt seems to validate our view of the stability of the cash flow, and potential to add more debt to the balance sheet in a LBO type scenario, as all three tranches are trading well above par and tight versus Treasuries. In fact, 5-year DF paper is trading at only 210 basis points above comparable Treasuries.

The key pushback from many is that DF is a “value trap”, or a business in decline, so it is a cheap stock that can get cheaper. Indeed, there have been a number of publicized articles recently that highlight that per capita milk consumption has been in decline since 1970. Even if this is accurate, total volumes have shown a steady increase in recent years, which is more relevant for a market share leader like DF. In fact, in the chart below we show that total volumes have increased by 20% over the last nine years. Not stellar, but definitely the kind of growth and cash flow that gets a private equity firm licking the milk off their moustache!

Daryl G. Jones

Director of Research