TODAY’S S&P 500 SET-UP – June 7, 2013

As we look at today's setup for the S&P 500, the range is 62 points or 0.96% downside to 1607 and 2.86% upside to 1669.

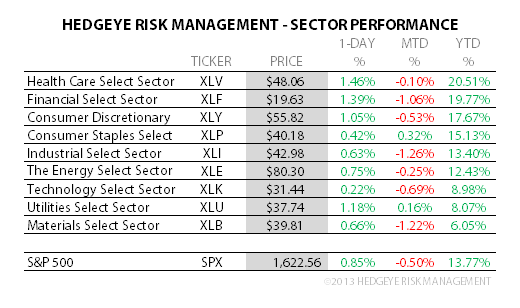

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 1.76 from 1.79

- VIX closed at 16.63 1 day percent change of -4.97%

MACRO DATA POINTS (Bloomberg Estimates):

- 8:30am: Change in Nonfarm Payrolls, May, est. 165k (prior 165k)

- 8:30am: Change in Private Payrolls, May, est. 175k (prior 176k)

- 8:30am: Chg in Manufacturing Payrolls, May, est. 4k (prior 0k)

- 8:30am: Unemployment Rate, May, est. 7.5% (prior 7.5%)

- 1pm: Baker Hughes rig count

- 3pm: Consumer Credit, April, est. $13.3b (prior $7.966b)

GOVERNMENT:

- House not in session; Senate schedule TBA

- 8:30am: Mental Health America holds conf. on wellness breakthroughs, whole health

- 10am: House Transportation and Infrastructure panel field hearing on improving the rail service in the northeast corridor

- 11am: ABA, Economic Advisory Committee news conf. to present monetary policy predictions, consensus economic forecast, including consequences of sequester, spending cuts, housing recovery, whether banks are prepared to finance stronger consumer and business spending

WHAT TO WATCH

- Job gains probably restrained in May amid U.S. fiscal cutbacks

- Aso says Japan won’t intervene in market after surge in yen

- Apple, other tech cos., deny giving U.S. access to servers

- Glaxo may get Avandia reprieve after FDA panel vote on risks

- Fed seen reducing asset buying by smaller amount: survey

- Microsoft unveils trade-in rights for games on Xbox One console

- AT&T 2Q customer growth improves as margins shrink

- German exports rose more than economists forecast in April

- Bundesbank cuts German growth forecasts while signaling recovery

- Pimco defends $8.5b BofA mortgage accord as “outstanding”

- U.S. Retail Sales, BOJ, Iran, U.S. Open: Week Ahead June 8-15

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Fewest Hedge Funds Invest in Gold Since ’10 as Assets Slump

- Gold Traders Most Bullish Since Bear Market Began: Commodities

- Urals Exports Plunge as Russia Refiners Keep Oil: Energy Markets

- Tin Miners in Indonesia Stop Output on Raid Concern, Arsani Says

- Gold Premiums in India Double as Imports Decline on Restrictions

- Soybeans Head for Best Weekly Run in Four Years on Export Sales

- EU Suspends Some Licenses to Import Sugar After Tender in May

- Rubber Books Fourth Weekly Loss on Strong Yen, Demand Concerns

- WTI Crude Heads for First Weekly Gain in Four Before Jobs Data

- Low Dry Bulk Rates Boost Scrapping, Control Fleet Growth

- Palm Oil Heads for Fifth Weekly Gain as Stockpiles Seen Dropping

- LME Chief Abbott Plans to Leave After $2.2 Billion Takeover

- Dalian Soymeal Gains Limited by Bollinger: Technical Analysis

- Commodities Daybook: Gold Traders Most Bullish Since Bear Market

- Gold Heads for Best Weekly Run Since March Before U.S. Jobs Data

CURRENCIES

GLOBAL PERFORMANCE

EUROPEAN MARKETS

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team