TODAY’S S&P 500 SET-UP – May 31, 2013

As we look at today's setup for the S&P 500, the range is 33 points or 0.81% downside to 1641 and 1.18% upside to 1674.

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 1.79 from 1.82

- VIX closed at 14.53 1 day percent change of -2.02%

MACRO DATA POINTS (Bloomberg Estimates):

- 8:30am: Personal Income, April, est. 0.1% (prior 0.2%)

- 8:30am: Personal Spending, April, est. 0.0% (prior 0.2%)

- 8:45am: Fed’s Pianalto speaks in Washington

- 9am: NAPM-Milwaukee, May, est. 49 (prior 48.43)

- 9:45am: Chicago Purchasing Mgr, May, est. 50 (prior 49)

- 9:55am: U. of Mich Conf, May final, est. 83.7 (prior 83.7)

- 10am: Commerce Dept. issues benchmark revisions on retail sales data, wholesale inventories and sales data

- 11am: Fed’s Liang speaks in Washington

- 11am: Fed to buy $4.25b-$5.25b notes in 2017-2018 sector

- 1pm: Baker Hughes rig count

GOVERNMENT:

- House, Senate not in session

- 1pm: VP Biden addresses media after mtg w/ Brazilian President Dilma Rousseff, Vice President Michel Temer in Brazilia

WHAT TO WATCH

- U.S. consumer spending was probably little changed in April

- P&G said planning to promote 4 as contenders to succeed CEO

- Apple raises prices for some products in Japan after yen weakens

- Apple ruling to revolve around who can use standard technology

- Sony said to engage Morgan Stanley, Citigroup on Loeb plan

- Treasury 7-Yr auction demand rises with yield at 13-mo. high

- Boeing sells new 787 as Singapore splits $17b order

- Dell investors sue over founder’s buyout bid

- Japan’s April industrial production rose 1.7% m/m, exceeding the highest est. in a Bloomberg News survey

- Euro-area April jobless rate rises to record 12.2%, est. 12.2%

- Euro-area May consumer prices rise 1.4% in yr, est. 1.4%

- Italy jobless rate reaches 12%, 36-yr-high amid recession

- German retail sales unexpectedly fell for a 3rd mo. in April

- EMA’s CHMP monthly announcements may include Sanofi, Roche

EARNINGS:

- No earnings expected from S&P 500 cos.: Bloomberg data

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- China Gold Demand to Slow From April Surge, Association Says

- Gold Traders Divided as Physical Buying Surge Slows: Commodities

- Gold Falls on Speculation Demand May Slow After Price Rally

- WTI Heads for Weekly Drop as Stockpiles Gain Before OPEC Meets

- Copper Trims First Monthly Gain in Four Before Chinese Index

- Soybeans Head for Best Month Since July as U.S. Supply Dwindles

- White Sugar Gains on Africa, Middle East Demand; Cocoa Retreats

- Battle Over U.S. Natural Gas Exports Increases as Permits Flow

- ETF Investors Dumping Gold Add to Platinum Bet: Chart of the Day

- Tea Output in India Seen at Record as Normal Weather Aids Yields

- WTI Crude May Fall Next Week on Ample Stockpiles, Survey Shows

- SHFE Copper Stockpiles Rise for First Time in Nine Weeks

- Japan Pays Record Price for LNG Imports in April as Yen Weakens

- Gold Premiums in Singapore at Record Seen Declining Next Month

CURRENCIES

GLOBAL PERFORMANCE

EUROPEAN MARKETS

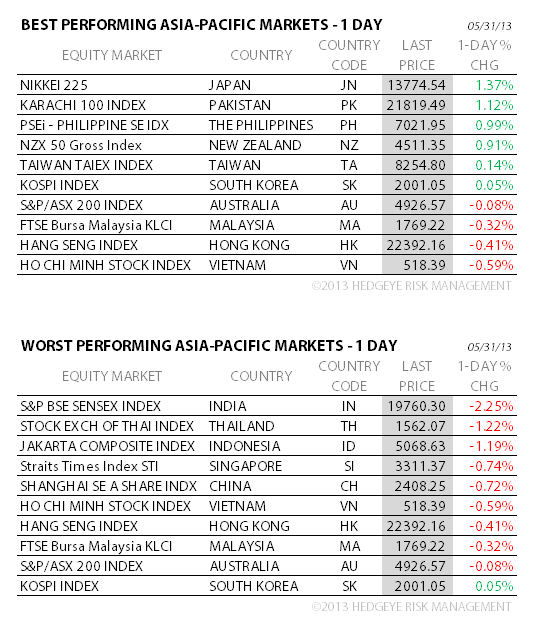

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team