My first job on the buy side was as a US Retail analyst. That was 9 years ago, and I think my boss gave me that group because it's the easiest one to analyze - I'm one of them Canadian hockey players, eh!

I started trading my own US Consumer "carve-out" of the fund within a few years, and effectively had to learn the art of job stability via not losing money. Losing money in the hedge fund business generally equates to losing one's job - as it should.

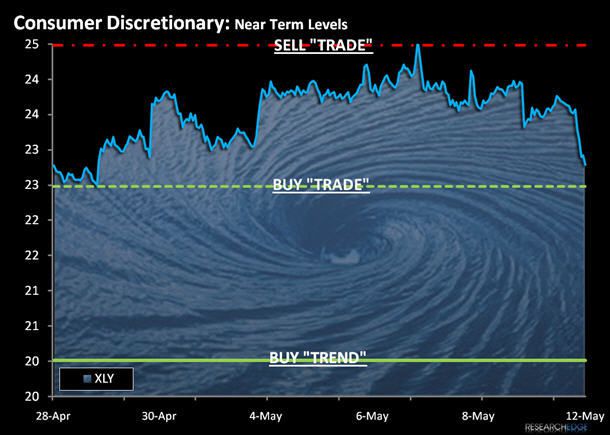

Making money on the long side isn't that hard to do. Not getting squeezed on the short side is. If the chart below had an audio clip, it would have a massive sucking sound - from now on I am going to refer to it as The Suckerpool Chart (this one will be really hard for Cramer to say is his - he hasn't used Squeezy yet either).

If you think being short the US Consumer Discretionary sector is a unique thought, think again. This sector, quantified, has the highest bottoms up short interest in the US market. It also now sports none other than Meredith Whitney as the latest doomsayer (yesterday she said short the group on CNBC). I thought she was a bank analyst? Maybe she's moving from the MEGA squeeze in her stocks on over to this one - who knows - but now she's in my sandbox this game probably won't end the way she thinks.

I sold my XLY (Consumer Discretionary ETF) on 4/29/09 at $23.18, so I haven't had to deal with the stresses associated with this sector's recent week of underperformance. Today, I am buying it back.

The Pain Trade that remains in this market is one that's really been a great story in 2009 - squeezing the US Consumer Depressionista shorts. Are they still out there? You tell me... how many people in your investment meetings are ragingly bullish and "long of" US Consumer Discretionary stocks?

I have painted the lines of support (green) and resistance (red) in The Suckerpool Chart below.

KM

Keith R. McCullough

Chief Executive Officer