Listening to each of these companies’ respective presentations today at the Sanford Bernstein conference, it was not difficult to understand why we like SBUX and are bearish on MCD.

Takeaways from the presentations:

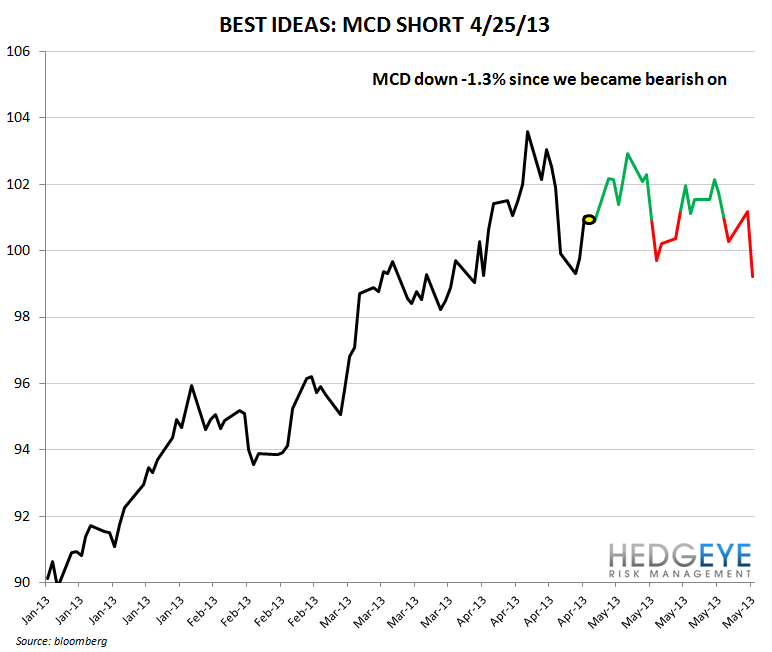

MCD

We remain bearish on MCD as the stock has underperformed the S&P 500 by 550 basis points since we added it to our Best Ideas list on 4/25. On an absolute basis, the stock has declined -1.09%. We believe the Street’s expectations are still too aggressive, from a sales and earnings growth perspective, and the company needs to make structural changes to its U.S. business as the store has become too complex. Please click here for the materials for our presentation on McDonald’s from 4/25.

- MCD CEO Don Thompson was cautious in his tone, citing soft economic environment and stagnant IEO industry

- Comps have outperformed QSR sandwich operators in 16 of 19 weeks this year (we are wary of this statistic as sandwich concepts compete against everyone in food service)

- Overall tone seemed to convey a message of near-term struggle with bright long-term ahead

- Mgmt stating, first, that guest counts are important for franchisees was interesting – franchisees want higher margin items on the menu, there is a conflict between corporate and franchisees here in terms of priority

- Unconvincing response as to what mgmt will do to revive U.S. business in ’13 – the menu is back and marketing is stronger and “more direct” – does not inspire confidence

- Europe remains a significant problem for McDonald’s

SBUX

Starbucks’ presentation represented a stark contrast to McDonald’s as the company offered a clear, positive and energized outlook for shareholders. The company’s data-anchored strategy is tailored for specific regions of the world, unlike the more general and now-outdated MCD strategy (three global growth priorities). We continue to view Starbucks as one of the best ways to play the strengthening U.S. economy and consumer.

- Goals of the company remain as lofty as ever – no constraints being placed on Schultz’ ambition

- SBUX foundation for growth is solid, primed for accelerated growth over the next 5, 10 years

- Challenges in Europe are persisting and will persist for “quite some time”

- Growth being supported by Via, K-Cups, home brewer systems, tea and other categories such as juice

- Expanding the loyalty card into the grocery aisle and following the rise of mobile internet closely

Conclusion

If you wanted to own a global company with strong growth prospects, sound fundamentals, high exposure to the U.S. recovery and low exposure to Europe’s travails, you would own SBUX and not MCD. We remain positive on SBUX and negative on MCD.

Howard Penney

Managing Director

Rory Green

Senior Analyst